| News Home |

GreklandGrekland är inget särfall, bara ett extremfall

Rolf Englund blog 5 februari 2012 En av mina bästa artiklar, tycker jag själv Greklandskrisen på 30 sekunder

Grekland kan betala sin förfallande skulder om de får nya lån. Men det hjälper inte kostnadsläget. Rolf Englund blog 19 sept 2011   Det finns de som försöker skylla den aktuella krisen på euron.

Peter Wolodarski, DN 2010-05-02  What Happens If Greece Defaults? - CNBC

What happens when Greece defaults. Here are a few things:

Andrew Lilico, Daily Telegraph, May 20th, 2011 - Every bank in Greece will instantly go insolvent.

- The Greek government will nationalise every bank in Greece. - The Greek government will forbid withdrawals from Greek banks. - To prevent Greek depositors from rioting on the streets, Argentina-2002-style (when the Argentinian president had to flee by helicopter from the roof of the presidential palace to evade a mob of such depositors), the Greek government will declare a curfew, perhaps even general martial law. Grekland står på randen av statsbankrutt.

EU:s valutaunion har visat att den inte håller måttet. Att EU:s valutaunion spricker är inte realistiskt, men att det ”otänkbara” faktiskt diskuteras säger åtskilligt om allvaret. Signerat, Claes Arvidsson, SvD 7/5 2010 Where the IMF Gets its Money IMF

Clinging to my naive faith in the integrity of contracts, I assume that ISDA will soon trigger the credit default swaps on Greek debt. If the Greek contracts are not triggered, it will destroy the CDS market for sovereign debt. It will deter investors from buying any Club Med bonds if they cannot take out reliable and easily-traded insurance at any time.

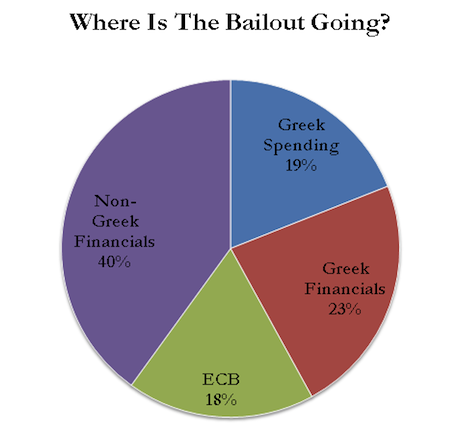

Greklands Default Kommentar Eurozone finance ministers reached a long-delayed €130bn second bail-out for Greece early on Tuesday a “voluntary” deal Voluntary However, there has been talk of asking creditors to take a steeper cut in the face value of bonds, or on the interest rate paid, to help Greece meet debt-reduction targets. Greek Default The writedown, or "haircut", of up to 70% on Greek bonds Voluntary "events have a habit of demolishing dreams" - Portugal, internal devaluation Greece must default if it wants democracy Why the Greek Bailout Doesn’t Change Much of Anything Ett sista tabu i eurokrisen är på väg att försvinna. En historisk reträtt ur valutaunionen eller inte, den har redan fått ett namn "Grexit" . Medverkande är professor Lars Jonung, chefsanalytiker Pär Magnusson och radions korrespondent i Berlin, Daniel Alling. Brandförsäkringsargumentet Allt talar för att grekerna kommer att proteströsta fram ett politiskt kaos. Man kan naturligtvis säga att med så kallade "frivilliga" nedskrivningar och en statsskuld på 160 procent av BNP så är Grekland i praktiken redan statsbankrutt. Men i maj, när det politiska kaoset är ett faktum och när det franska presidentvalet är avklarat, så lär euroländerna och ECB tvingas acceptera att Grekland valt att försätta sig i fullständig konkurs och lämna euron. Konsekvenserna är oöverblickbara, och EU måste ha beredskap för att pumpa in miljarder i bistånd. Det är djupt tragiskt att Grekland ska få lida så mycket The combined exposure of foreign banks to Greek entities - public and private - “EU is now saying to the Greek people: ‘Unless you vote for the right parties, we will not give you the rest of the money and you will go bankrupt,'” The big problem in Greece is that the worst economic effects of austerity haven’t even happened yet “On the current path – which is not sustainable in my view – we may very well see Greek GDP go down 25-30 percent, which would be historically unprecedented. It’s a disastrous crisis for them,” Dadush, a former senior World Bank official, said… “They’re suffering. It’s nasty,” said Weisbrot, who has studied the lessons to be learned from economic crises in Latvia and Argentina. “If you could say with a reasonable probability that the worst was over, then that would be different. But you can’t say that. They’re in for a long nightmare.” The point here is that both Europe and Greece need a light at the end of the tunnel. Without that, social unrest in Greece will only get worse, the credibility of its promises will continue to deteriorate, and the Europeans will be understandably reluctant to throw good money after bad The World from Berlin The center-left daily Süddeutsche Zeitung writes: The left-leaning daily Die Tageszeitung writes: The Financial Times Deutschland writes: The fact that this small, economically weak and chronically mismanaged country has been able to cause such difficulty also indicates the fragility of the structure. Quantifying Eurozone Imbalances and Many Greeks are in despair. Han är bildad, Ambrose; Grekland, Tyskland och the London Debt Agreement of 1953 What Greece has in essence committed itself to is an internal devaluation lasting years, if not decades into the future. No business can survive in such an environment. Not until Greece devalues, and Greek assets start to look reasonable value once more, will the money return. Yet instead, Greece has chosen the internal devaluation route, or the forced reduction in wage and asset prices necessary to restore competitiveness. Does anyone other than the technocrats and the hair-shirted Germans really think such a road possible? In less extreme form, much the same hard labour awaits the rest of the eurozone periphery, which must similarly achieve big reductions in real exchange rates via the socially destructive path of decreases in nominal wage and asset prices. Interndevalvering - Ådalsmetoden Interndevalvering Grekland står inför sin ödesdag och det är nödvändigt att hela landet inser stundens allvar. Det grekiska budgetunderskottet på runt tio procent av BNP behöver omgående minskas. On Friday, German commentators argue that it is time for EU politicians to face the truth about the situation Why Greece Will Default, Leave the Euro Zone The debt burden is unsustainable and the austerity measures demanded by the "troika" will only make it more so. With unemployment [cnbc explains] already at 21 percent, further government spending cuts are likely only to drag the economy down even more. More importantly, perhaps, it is simply intolerable for a free nation to allow itself to be pushed around by its creditors. The creditor nations may feel like they have the moral authority to shove around Greece, but they are wrong. They have neither the moral authority nor the actual, operational authority. Greece can hurt them as much as they can hurt Greece. What Happens If Greece Defaults? Riktigt intressant blir det om och när Grekland lämnar euron. Portugiserna kommer i så fall börja fråga sig varför de ska genomlida femton år av misär, när det enda man behöver göra är att lämna euron. Därefter kommer spanjorerna och italienarna. European finance ministers held back a rescue package for Greece in a rebuff that “In short: no disbursement without implementation,” Luxembourg Prime Minister Jean-Claude Juncker said in Brussels late yesterday after chairing emergency talks of euro-area policy makers. Europe is now deliberately trying to push Greece out Merkel: I Won't Take Part In Pushing Greece Out Of Euro Angela Merkel is often depicted by the Western media as a boring, mousey and indecisive physicist obsessed by rules and the Euro ideal. Finance minister Evangelos Venizelos was quoted by Kathimerini: „Merkel fordert bedingungslose Kapitulation“ Its called the Greek "bailout" or the "Greek rescue package" Greek leaders thought they had fulfilled their side of the bargain, same politicians have now been told they have three days to come up with a bit more budget pain And they have to all promise (in blood?) that they will stick with the programme, no matter what the voters might say in April Sure, Greece would have a terrible time after a messy default. But then, the life they are signing up to under the terms of the deal is going to be pretty terrible too. And if eurozone ministers get their way, it's a life that Greek voters are not going to be allowed to reject. Where the Greek bailout money goes

Daniel Hannan, February 8th, 2012 It's Time To End the Greek Rescue Farce For the past two years, Greece has wrangled with the euro-zone states and the International Monetary Fund (IMF) over its so-called "rescue." Austerity measures have been agreed to, aid has been paid and private creditors have been forced to accept "voluntary" debt haircuts. Despite all this, Greece is in even worse shape today than it was then. Its economy is shrinking, the debt ratio is rising and the country and its banks have been cut off from capital markets. There isn't even the slightest sign that the situation might improve. Det finns de som försöker skylla den aktuella krisen på euron. Man måste ställa sig frågan om inte Grekland och i synnerhet grekerna har mest att vinna på att ställa in betalningarna och skriva ner sitt skuldberg How much is the troika demanding from Greece? How tight is the squeeze?

JP Morgan Advises Its Clients To Read Zero Hedge Three Weeks Ago Three weeks ago, Zero Hedge was the first to bring the world's attention to the legal (and explicit trading/risk) ramifications of European sovereign bonds. We noted the ECB/IMF's subordinating impact on unsuspecting sovereign bond holders but much more explicitly showed the huge gap in market perception between domestic- and foreign-law bonds (and the fact that they have very different ramifications given the rising tendency for retroactive CACs or simply local-law changes to accommodate restructurings). If Athens cannot sign up the required 90 percent of bondholders needed to push through the debt haircut and bailout, it may have to use new legislation for Collective Action Clauses, or CACs. What Happens If Greek Debt Swap Deal Fails? Thus far the ISDA has not judged the deal a “credit event” forcing the triggering of anti-default insurance policies known as credit default swaps. “I don’t anticipate that would be a destabilising event,” he said. Involuntary Investors and traders fear the decision not to trigger a credit event Involuntary There is a ruling from the International Swaps and Derivatives Association which says that credit default swaps, an instrument designed to insure against just such an event, will not be paying out. Or rather it makes a statement in insurance company legalese that goes The EMEA DC determined that it had not received any evidence of an agreement which meets the requirements of Section 4.7(a) of the 2003 Definitions and therefore based on the facts available to it, the EMEA DC unanimously determined that a Restructuring Credit Event has not occurred under Section 4.7(a) of the 2003 Definitions .Voluntary Earlier in the day, the International Swaps and Derivatives Association said Greece had not triggered a payout on credit default swaps by its recent moves to prepare for a debt restructuring, The ruling means holders of these insurance contracts, worth a net $3.25 billion, will not receive payment at this stage, though further rulings based on any new questions are still possible. Involuntary Voluntary Många fonder har en sorts försäkringar – CDS:er – vilket gör att de får tillbaka pengarna även om allt går åt skogen. Går Grekland i konkurs faller däremot försäkringarna ut. Involuntary If it become seen as a precedent, Mr. Blitzer says, "prices of the debt of other peripheral euro-zone countries could be negatively affected." Grekland CDS Sedan millennieskiftet har handeln med försäkringar mot statsbankrutter ökat, så kallade Credit Default Swaps. Går Grekland i konkurs ska innehavaren ha betalt, men frågan är om försäljarna har råd med kostnaderna. Voluntary Default will trigger credit-default swap contracts, derivatives known as CDS that protect the owner from events such as default. This will implode the shadow-banking system and the visible banking system, as those who sold the CDS (financial institutions) do not have enough cash or assets to pay the owners of the CDS. Grekland ett permanent bekymmer, som slutligen kan leda till att grekerna tvingas gå bankrutt och kanske även lämna euron. ”Chicken Race” Voluntary Ledaren för eurozonens finansministrar, Luxemburgs Jean-Claude Junker, beskriver förhandlingarna som "extremt svåra". Regeringskälla: Den grekiska regeringens förhandlingar med internationella borgenärer går bra Ah, but what do we have here, at 3:36 AM (via my London partner, Niels Jensen), Voluntary The Greek default will have only the most minor effect on the United States - except that it will give the White House and its Federal Reserve appointees someone other than themselves to blame for the economy not recovering in 2012. Voluntary While Laos (People’s party) has only 16 seats in the Greek parliament, its anti-European line is echoed by lawmakers in Pasok, the socialist party that lost power in November but is now part of the three-party coalition headed by Lucas Papademos, Greece’s technocrat prime minister. Antonis Samaras, the conservative leader, has also warned that Greece cannot take more austerity Grekland är ett sorgligt särfall. Portugal - The next special case? Irland - Italien - Spanien - Portugal Voluntary German commentators on Friday say it's time for a bit of honesty from Europe's leaders. The center-right Frankfurter Allgemeine Zeitung writes: "Europe's citizens are growing accustomed to only being told a small part of the truth. In the end, Olli Rehn's vague comments could mean that the European Central Bank will have to waive a portion of its Greek bond claims. That could, in turn, make itself felt in the budgets of euro-zone member states. European taxpayers, though, will never be told the full extent of the damage.... Even should there be debt relief for Greece, it will not put a stop to the country's thirst for borrowing. Debt relief would change nothing when it comes to the shocking inability of the Greek economy to compete internationally. Yet, without economic growth, there is no foundation for healthy state finances." Grekisk tvångsförvaltning Anna Diamantopoulou 1999-2004 EU-kommissionär med ansvar för sysselsättning och socialpolitik i Prodi-kommissionen. Wikipedia Forderung nach Sparkommissar Griechen-Presse pöbelt gegen Berlin

„Merkel fordert bedingungslose Kapitulation“ Unconditional surrender

The use of the term was revived during World War II at the Casablanca conference when American President Franklin D. Roosevelt sprang it on the other Allies and the press as the objective of the war against the Axis Powers of Germany, Italy, and Japan.

The term was also used at the end of World War II when Japan surrendered to the Allies.

Both Winston Churchill and Joseph Stalin disapproved of the demand for unconditional surrender, as did most senior U.S. officials (except General Dwight D. Eisenhower). "EMU är i alla fall bra för freden" Tyskland vill att en ny budgetkommissionär, utsedd av eurozonen, I dokumentet, som lämnades till medlemmarna i eurozonen på fredagen, skriver Tyskland: "Med tanke på det misslyckade uppfyllandet hittills måste Grekland acceptera att lämna över bestämmanderätten över budgeten till Europanivå under en viss tid". Horst Reichenbach Logiken i det hela rör sig i federativ riktning... Sch! säger Kohl åt mig när jag tar upp det. Over the next two months Greece has promised to adopt legislation

Acropolis now

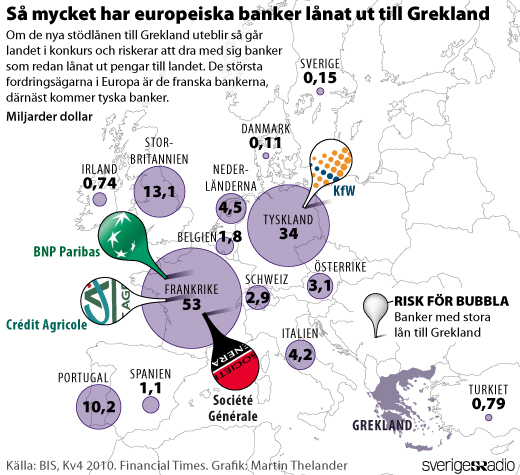

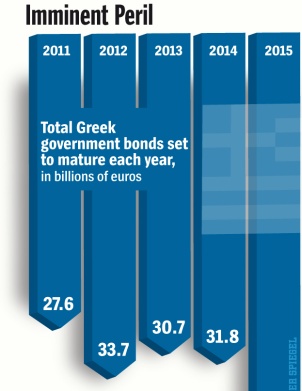

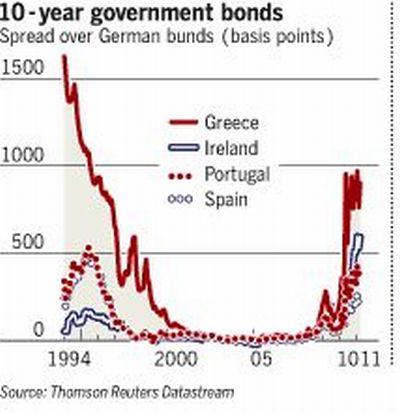

The Greek debt crisis is spreading. Europe needs a bolder, broader solution—and quickly Speaking on the fringes of the forum, George Soros, the financier, blamed Germany for many of the eurozone’s woes. Involuntary "Hedge funds don't need to worry about their public image," one banker says. Their reputation has already been destroyed. Therefore, they can be relatively cavalier in gambling with the possibility of a Greek bankruptcy. Greece Involuntary Discard the veneer of voluntarism and Greece can be tougher on its creditors. It should pass a law that retroactively introduces collective-action clauses into all domestic-debt contracts (making it easier to impose debt deals on recalcitrant bondholders). If it does this now there is still, just, enough time to organise a big, coercive, but orderly, restructuring of Greek bonds by March 20th. Credit default swap, Wikipedia Sardelis och The Ticking Euro Bomb, The creditors, represented in the negotiations by the Institute of International Finance, have said that they won't agree to interest rates of less than 4% on the new bonds. And then there's the European Central Bank, which owns around €45 billion of Greece's debt, purchased on the secondary market. European finance ministers balked at putting up more public money for Greece, Greek bondholders draw line in the sand Now, the bankers and leaders of Europe are getting ready to walk to the edge of the Abyss. if relatively big economies like Italy and Spain got into trouble

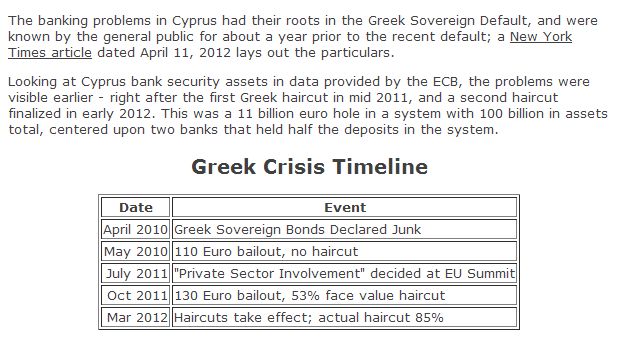

One of the unresolved problems hanging over the eurozone was what would happen if relatively big economies like Italy and Spain got into trouble. There was neither a fund big enough to rescue them nor a firewall large enough to prevent contagion. A permanent rescue fund, the European Stability Mechanism (ESM), has been brought forward and should be in place by the summer. It will have a lending capacity of 500bn euros. There are still 250bn euros in the existing rescue fund, the European Financial Stability Facility (EFSF). One plan is to run these two funds in parallel. The Germans are currently under enormous pressure to boost the fund to over a trillion. The sticking point is the interest paid on the new bonds, bearing in mind they will not mature for 30 years. Greece, Voluntary... Vem avstår frivilligt 70 procent av sin fordran? Greece was closing in on an initial deal with private bond holders on Friday The agreement, to be followed up by technical talks over the weekend, could come later in the day, sources close to the negotiations said. Private bondholders would most likely incur a real loss of 65 to 70 percent, with the new bonds having a 30-year maturity and offering a progressive coupon, or interest rate, averaging out at 4 percent, a banking official close to the talks told Reuters. Hemligt PM. Marshall-hjälpen, Grekland och Carl Bildt Standard & Poor´s motiveringar till sina nedgraderade kreditbetyg för en lång rad euroländer drar ner byxorna på euroetablissemanget, Angela Merkel om "frivillig" nedskrivning med 50 procent av Greklands skulder As one senior figure who has long played a role in the euro negotiations says, politicians hate being pushed around by markets Ms Merkel’s scepticism also stems from bitter experience. The European Central Bank and Mr Sarkozy had warned that such contagion would happen. Varför ska man sitta på portugisiska papper när Angela Merkel gjort klart att det är de privata långivarna som ska förlora. Merkel signed up to a commitment that private sector bondholders The “haircut” on Greek debt sparked investor fears that the debts of other heavily indebted countries such as Italy and Spain might also not be honoured, contributing to a sharp increase in their bond yields. Ms Merkel said it was imperative to show that Europe was a “safe place to invest”. zcc "Signs of stabilisation are emerging in the banking sector," At Cyprus's banks, non-performing loans - ones where payments have been missed - "For a small, open economy like Cyprus, Getting creditors not taxpayers to rescue banks seemed like a good idea, Amid tough competition, Cyprus’s banking crisis was a contender for Europe’s worst.

But getting creditors both to absorb losses and to recapitalise the country’s biggest bank (which also had to absorb the second-biggest and even more comprehensively bust bank) is not proving to be a great success. Three lessons can be learnt from the Cypriot saga. "For a small, open economy like Cyprus, Euro adoption provides protection from international financial turmoil." ECB-Trichet 2008 The EU's bailout of Cyprus has elicited unusually frank and vehement criticism from the finance experts grouped in the IMF's Executive Board.

Det är bara en tidsfråga innan ett av de stora krisländerna väljer en politisk ledning som inte längre godtar åtstramningsdiktaten.

Den pågående förtroendekrisen är långt farligare än en förnyad oro på marknaderna, eftersom den inte kan övervinnas med ännu en likviditetsinjektion från ECB. Det beror på att Tyskland, utan jämförelse EU:s starkaste ekonomi, har genomdrivit en strategi för att övervinna eurokrisen

Alla i Europa vet att krisen antingen kommer att tillintetgöra EU eller leda till en politisk union,

"For a small, open economy like Cyprus,

Cyprus, Spain, Greece, Italy Since this eurozone crisis began, a view has emerged, not least among the single currency’s most stringent advocates,

Are all these countries, their electorates supplicant, really going to subscribe to and live under, for decades to come, a system based on Germany telling them how much they can borrow and spend?

Depositors are not bondholders – who knew their money was at risk and reaped a commercial yield on their investment.

Monetary union, also, requires “banking union” we are told. Is that really going to happen? Do current events in Cyprus make it more, or less likely? The answer is obvious, for anyone prepared to see. And are capital controls even legal? Articles 63 and 65 of the European Union treaties say such controls are justified “only on grounds of policy or public security” and should “not constitute a means of arbitrary discrimination or a disguised restriction on the free movement of capital and payments”.

Europe’s Cyprus Blunder and Its Consequences

I fallet Cypern går Tyskland och dess allierade, däribland Finland och Slovakien, mycket hårdare fram än vid de fyra tidigare tillfällen då EU har tvingats ingripa med nödlån.

Bankpanik är en oerhört destruktiv företeelse... Det kusligaste exemplet är Creditanstalt, en bank i Österrike. Den havererade 1931. Paniken fortplantade sig i Europa och över Atlanten. I USA fördjupades depressionen. Och i Tyskland följde katastrofernas katastrof. Vad skall euroministrarna göra med stöldgodset?

Demanding that Cyprus raise €6bn – almost a quarter of its annual GDP – over a weekend is “a big ask”

The eurozone after Cyprus

The principle of divorcing the debt of governments from that of banks (and thus breaking the “diabolical loop” which threatened to bring down Spain last year), was very rapidly thrown out of the window in Cyprus. There was apparently no willingness to use ESM money directly to recapitalise the banks, even though that is being done successfully with the Bankia resolution in Spain this very week. --- Bankia SA shareholders will be nearly wiped out and its junior bondholders will lose about 30% of their original investment in the restructuring plan for Spain’s largest ailing bank, the country’s bailout fund said Friday. Under the strict terms of a European-Union financed cleanup of Spain’s banking industry, the Fund for Orderly Bank Restructuring is forcing investors to bear heavy losses before injecting public funds into the banks. In Bankia, the nominal value of its shares will be reduced to €0.01 from €2 and the nominal value of its preferred shares and subordinated debt will be reduced to €4.84 billion ($6.29 billion) from €6.91 billion, the bank-restructuring fund said. --- It is a well established principle of bank work-outs that losses should be taken in the following order:

Direct controls over the exit of capital from a eurozone member will have occurred for the first time in Cyprus. It seems to breach one of the basic principles of a single currency. (See Jeremy Warner.) Cyprus 'business model' was no mystery to EU

Be it the German finance minister, European Central Bank (ECB) officials or the head of the Eurogroup - they all agree on one thing: Cyprus must scrap its "unsustainable business model" based on low taxes and attracting large amounts of bank deposits from abroad, mainly Russia. In a so-called convergence report dated 2007, one year before Cyprus joined the eurozone, the ECB mentioned the large influx of capital. "Much of the financing of the deficits in the combined current and capital account over the past two years has also come from capital inflows in the form of 'other investment,' comprising non-resident deposits and loans," the report says. "Other investment inflows amounted to a sizeable 11.3 percent of GDP in 2006. Since capital inflows exceeded the current and capital account deficit between 2004 and 2006, Cyprus experienced an accumulation of official reserve assets in this period," it adds. It was the morning after the night before and I was riding an elevator to the 13th floor in the European Commission. Two men smiled at each other and one said "I hear Greece has been saved". "Couldn't be better," beamed the other, before disappearing into the vastness of bureaucracy. It felt like news shared from a distant front: "Bastogne has been relieved" or "Malta is holding out". Gavin Hewitt, the BBC's Europe editor blog 26 March 2010 Cyprus is a low-tax jurisdiction, not a tax haven. Cyprus an arrangement with all of its OECD bilateral (double-taxation treaty) partners – 46 fully, 6 being ratified. Within these 52 countries, Cyprus has double-taxation treaties with about every country in the EU, and includes China, the US, Russia and, practically, every Middle East country. All the double-taxation treaties concluded by Cyprus were drafted on the basis of the Organization of Economic Co-operation and Development (OECD) model treaty. The Germans want large investors - many of them Russians - to share in the cost of bailing out Cyprus.

But senior European finance-ministry officials in a call Friday evening expressed

Let the failing banks fail. Only The Wall Street Journal's editorial board seems to understand this The unlearned lesson of Lehman remains badly unlearned. The problem wasn't that Lehman failed—it was that the government was never able to send a consistent message about its approach to troubled financial firms. Bear was rescued, Fannie and Freddie brought into something called a conservatorship, Lehman bankrupt, and AIG bailed out. No wonder chaos broke out. This is what's at risk in Cyprus. There seem to be no agreed-upon rules, no official process, nothing that can be counted upon. John Carney, Senior Editor, CNBC.com, 22 Mar 2013 --- Here's how it could work: Shareholders, along with senior and subordinated debt holders, would be wiped out. Deposits up to €100,000 that are insured would be protected. Larger depositors would take a haircut in the range of 40%—somewhat more for Laiki depositors, somewhat less for account holders at Bank of Cyprus, reflecting the extent of the losses and the capital needs at the two banks. In exchange for their losses, these depositors would get all the new equity; they would become the proud owners of two newly well-capitalized banks. No public funds would be needed to save the banks, and both creditor seniority

Kommer Vargen?

Cyprus was just hours away from a deal on Friday to raise billions of euros and With hundreds of demonstrators facing off with riot police outside parliament, lawmakers were preparing to debate bills to nationalize pension funds, pool state assets and split the island's second-largest lender, Cyprus Popular Bank, into good and bad assets in a desperate effort to placate exasperated European allies. The official sick man list of Europe has long been the PIIGS, or if you prefer, the GIPSI: The latest Flash PMI data spell further bad news for the French economy, with the downturn in output accelerating to the sharpest in four years Reuters argues Slovenia will be next to ask for a rescue:

Cyprus exposes folly of eurozone banking union Over the past three years the EU has shown a remarkable facility for turning problems into crises and crises into catastrophes. The writer is a former chairman of the UK Financial Services Authority, former deputy governor of the Bank of England and former director of London School of Economics. He is now a professor of practice at Sciences Po in Paris This crisis has revealed yet again the faultline at the heart of the euro.

The worst outcome would be to allow the Cypriots to slide towards the exit.

Even if only uninsured deposits are hit, a line has been crossed. A formal European bail-in regime is needed as soon as possible, one that requires banks to hold a layer of loss-absorbing senior debt designed to spare depositors, both insured and uninsured, in all but the last resort.

There is no provision in any European Treaty for a country to leave the eurozone. Stocks shot higher Friday, erasing their losses from the previous session,

De slutna rummens beslutsfattande är ansiktslöst

“It’s déjà vu all over again.” The European game goes like this: Undantagstillstånd

The EU's smaller members aren’t getting a fair shake in the eurozone, Eurogroup Working Group

Euro zone finance officials acknowledged being "in a mess" over Cyprus during a conference call on Wednesday and discussed imposing capital controls to insulate the region from a possible collapse of the Cypriot economy. The call was among members of the Eurogroup Working Group, which consists of deputy finance ministers or senior treasury officials from the 17 euro zone countries as well as representatives from the European Central Bank and the European Commission. Cypriot Financial Sector Faces Collapse ECB to Push Cyprus Over the Brink Cyprus: The Sum of All FUBAR 1. Runaway banking. Cyprus has a huge banking system — assets around 8 times GDP — based on a business model of attracting offshore money with high rates and good opportunities for tax avoidance/evasion.

The initial screwup was a joint error of the Europeans and the Cypriots.

FUBAR (fucked up beyond all recognition/any repair/all reason)

ECB PRESS RELEASE 21 March 2013

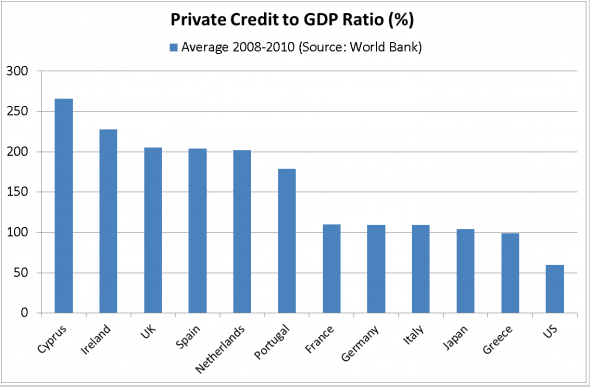

Cyperns ekonomi är liten och i sig en minimal smittorisk för eurozonen.

Även när privata investerare i grekiska statsobligationer i fjol ”frivilligt” tvingades acceptera förluster (för övrigt den stora knäcken för de cypriotiska bankerna) påstods det vara en unik åtgärd. Utan tvivel är den cypriotiska banksektorn för stor, åtta gånger landets BNP. Det är lite mer än på Irland vid tiden för kraschen, även om det stabila Luxemburg också har en gigantisk finansbransch. Precis som Cypern hittills vägrat genomföra privatiseringar och maskat med andra reformer, finns det EU-krav om bankerna som inte följts. Har Cypern inte råd att underhålla sin affärsmodell är det knappast europeiska skattebetalares sak. Men strukturförändringar tar tid. Samtidigt står banksystemet på Cypern inför en härdsmälta. Att Cypern tvingas lämna euron kan inte uteslutas, och de direkta efterräkningarna för valutaunionen torde i så fall bli begränsade. Men åter ligger faran i exemplets makt: kan Cypern gå ur samarbetet, så kan väl Grekland och… Russian prime minister Dmitry Medvedev:

Cyprus - The disaster scenario

On Tuesday, not a single member of the Cypriot parliament voted in favor of the legislation.

De som i dag har pengar i banker på Cypern kommer, om euroministrarna får som dom vill, att få upp till 9,9 procent av pengarna konfiskerade.

To say that the tensions within the European "Union" are getting unbearable would be an understatement. Riktigt hur det gick till när euroländerna krävde konfiskering av bankspararnas pengar för att gå med på nödlån till Cypern får vi kanske aldrig veta. Europe's Reckless Raid on Cyprus's Savings Bernard Connolly

Cyprus rescue breaks all the rules Genom att även konfiskera småsparares pengar upphävs en princip som gällt sedan den amerikanska depressionen på 30-talet: Europe is risking a bank run

IMF and the German government want to reduce the size of any loan to Cyprus by forcing it to “bail in” the creditors of Cypriot banks,

Kommentar av Rolf Englund:

Even those people who come from larger EU countries should be conscious of the fact that

Rehn: The French government has begun structural reforms, but the economic outlook has also simultaneously and unexpectedly worsened. France must now persuade the European Commission and its European partners that it will get its public finances in order in medium-term. SPIEGEL: What use is it, then, if Europe obliges itself to ever greater budgetary discipline, but in reality is constantly making concessions? Rehn: I don't make any trade-offs when it comes to the Stability Pact rules. The reformed pact places an emphasis on making public finances sustainable in the medium-term. In the short term, certain divergence can be accepted under the condition that a country is implementing reforms.

Europakten - Frankrike - Stabilitetspakten Europe faces an impossible challenge - why can't Olli Rehn see it?

Cyprus is having a hard time shaking its reputation,

"The Eurogroup called on the international institutions and Cyprus to accelerate their work on the building blocks of a program,

That is likely to appease Germany, which has raised concerns about money-laundering on the island. The ministers examined a variety of options to finance the bailout and ensure that it is "sustainable" - that Cyprus can repay what it borrows. 17 miljarder euro? Javisst, men inte i dag

The bailout could be worth up to 17bn euros. Eurogroup head Jeroen Dijsselbloem said ministers were ready to help Cyprus, "but the details still needed to be worked out". Simon Nixon says Cyprus, not Italy, decides the fate of the eurozone Writing in the Wall Street Journal, Simon Nixon argues that Italian politics is important but only in the long run.

He said Germany’s insists on a depositor bail-in might trigger panic across the eurozone’s weaker banking sectors. He concludes that it will be hard to square the requirements of Cyprus with those of German politics. ---How this situation is resolved could have profound consequences for the euro zone.

Berlin's preference appears to be a traditional euro-zone can-kicking exercise, with a solution cobbled together via mixture of fudged numbers, nondepositor haircuts, privatization promises and euro-zone bailout cash—the aim being to at least defer the problem until after Germany's own elections in September. In the current political climate, it may be difficult to get any bailout for Cyprus through the German parliament.

The German government is now resigned to accepting an aid package for Cyprus without a default,

PSI

Att skriva ned skulderna båtar föga. Men framför allt hade Europa lovat att just den metoden var unik för Grekland. Om det inte längre stämmer kommer marknaderna att undra i vilka andra sårbara länder den då är tänkbar. The extraordinary thing is that there hasn't yet been a bank run across the Mediterranean Until now, the EU has sought to reassure depositors by guaranteeing – absolutely guaranteeing – that savings up to €100,000 are secure,

What would you do now if you had savings in a Greek, Spanish or Portuguese bank?

Undantagstillstånd

Undantagstillstånd

Are you a Russian company with deposits in Cypriot banks?

She started her career in the investment banking division at Lehman Brothers in the summer of 2007, timing it perfectly with the beginning of the credit crunch. When the bank collapsed she was pictured walking out of the the building with a box of her belongings. The picture somehow made it to the front of various newspapers, and has seemingly since become a stock image used by picture desks to illustrate anything from greedy bankers to the victims of capitalism. Her friends briefly nicknamed her “the face of the credit crunch” but fortunately it didn’t catch on.

Radical rescue proposed for Cyprus

Cyprussia

A new parking scheme appeared late last year in some congested Moscow neighbourhoods. Street signs advised Muscovites either to buy a ticket at a nearby machine or text their licence plate details to a number: 7757. Evgeny Schultz, a Moscow blogger, took a closer look. It turned out that the number 7757 had been bought by a company registered just six months previously, which itself had been founded by two Cyprus-registered companies whose ownership was unclear. German Finance Minister Wolfgang Schäuble, as he has made clear several times, Cyprus is in urgent need of up to €17.5 billion ($23.6 billion) in emergency financing, primarily to prop up its ailing and outsized banking sector. But a bailout of that size would be roughly equivalent to the country's annual gross domestic product and would increase the island nation's sovereign debt load to a potentially unsustainable level. The German government is now yielding to the pressure from the European Commission, the ECB, and other member states over a Cypriot rescue programme.

But a package in this magnitude is not going to solve Cyprus’problems. The country will be left stranded with a massive increase in its debt ratio. This can only work if the country changes its business model, and closes down some of its banks. Reichenbach --- Cyprus threatens to open a Pandora’s box

In June, Cyprus became the fifth country in the eurozone to request an international bailout after lenders, including Bank of Cyprus and Popular Bank (Marfin), got caught up in the debt restructuring of Greece’s banks. Richard McGuire, senior fixed-income strategist at Rabobank, says any attempt to force burden sharing on bank bondholders could risk renewing fears over the solvency of banks in the wider eurozone.

Fotnot:

If Greece were allowed to default, then what would that imply about other peripheral-country debt? Nästan alla etablerade partipolitiker kommer framstå som åsnor om EMU havererar.

Draghi calls Schäuble a lawyer The question of systemic relevance, he said, was not one that lawyers could answer. That was a matter for economists. (Schauble is, of course, a lawyer.)

Shakespeare's King Henry VI; "The first thing we must do is kill all the lawyers" Asmussen warns that Cyprus could harm the whole of the eurozone

Failure to deal with Cyprus could directly impact Greece through "banking channels" and send the "wrong signal" to other Eurozone countries, just as Ireland and Portugal are looking to re-enter capital markets, he said. Cypern

In a country like Cyprus (or Iceland, or Switzerland), where the banking sector is many multiples of national GDP, there’s very little distinction between rescuing the banks and rescuing the country. And if the asset side of the banks’ balance sheet is full of Greek sovereign debt, the liability side is equally dodgy: Cyprus is a notorious center of dodgy offshore banking, especially for Russians. If Cyprus is going to restructure its liabilities, it’s going to have to face one huge question: will those restructured liabilities include Russian and other foreign deposits? There is growing resistance in Europe to the planned aid program for Cyprus,

The euro rescuers face a dilemma. On the one hand, they want to prevent the country from going bankrupt. On the other hand, they lack the support of a majority of member states for an aid program that would mostly benefit rich Russian tax fugitives. Cyprus Bailout Could Fail in German Parliament

Even if euro-zone finance ministers do approve an aid package for Cyprus in February, the German parliament must sign off on it. Yet with elections in Germany looming this autumn, the Social Democrats have become less willing to follow Merkel's euro strategy.

SPD is considering blocking a Cyprus deal on the grounds that it won’t support tax dumping and money laundering

SPD chief Sigmar Gabriel is quoted as saying that the SPD could not approve a package for the Cypriot banks on the basis of current information available. If Angela Merkel were seeking SPD support (which she will need to get the package through the Bundestag), she will have to come up with good reasons, he said, a scenario he considers implausible. As the Greens have the same reservations about Cypriot banks, a Bundestag majority is not guaranteed – especially given the trend towards rising opposition within Merkel’s coalition. Ty Cypern Rysk bastion i Medelhavet

En mörkare sida av det ryska inflytandet på Cypern är miljardbeloppen som väller in över landet och i många fall sedan slussas tillbaka till hemlandet igen. Tyska veckotidningen Der Spiegel citerade häromdagen ur en hemligstämplad rapport från tyska säkerhetstjänsten BND i vilken det talas om 26 miljarder dollar som ryska oligarker ska ha placerat i cypriotiska banker, till stor del svarta pengar. spiegel.de/international/europe/money-laundering-accusations-could-stall-aid-to-cyprus Russia has no plans to grant a 5 billion-euro loan requested by Cyprus “We have no specific plans or instructions to do so,” Storchak said in a Dec. 24 interview in Moscow. “It’s obvious that no single creditor can work with Cyprus alone,” he said. “Anyone who steps up on an individual basis to finance that country’s government or to help recapitalize its banks would be taking an enormous risk.” Cyprus, whose public debt is forecast to reach 89.7 percent of gross domestic product this year, in late June became the fourth euro-area nation to request a financial rescue since a 2010 bailout of Greece. In addition to seeking aid from its euro-zone partners and the International Monetary Fund, Cyprus asked Russia for a fresh loan after borrowing 2.5 billion euros last year. A bailout deal with the euro area and IMF will be signed by Feb. 12, Kathimerini reported on Dec. 22, citing Thomas Wieser, who heads the group of officials that prepare meetings of euro- area finance ministers.

Moscow has signalled its willingness to take part in rescue of Cyprus,

Vladimir Putin told reporters after a summit meeting in Brussels on Friday: “We believe there might be a situation when we can engage in the resolution of issues related to the stabilisation of the situation in Cyprus.” IMF Demands Partial Default for Cyprus

To ward off insolvency, Nicosia has raided the pension funds of state-owned companies. The troika are looking at an aid package of €17 billion for the country.

Fully €10 billion of that would go towards propping up the country's wobbly banking sector. The fiscal situation in Cyprus, the fifth euro-area nation to seek international aid, is “more serious than Greece,”

Cypriot banks need about 9.3 billion euros ($12.2 billion) in fresh capital, according to a preliminary report by Pacific Investment Management Co., Cypriot broadcaster RIK reported Dec. 9. Another 6 billion euros may be needed to refinance state debt and 1.5 billion euros to cover fiscal deficits, Finance Minister Vassos Shiarly said Nov. 22. That would bring the total to 16.8 billion euros, almost the size of Cyprus’s 17.9 billion-euro economy. The country’s general government gross debt will rise to 89.7 percent of gross domestic product this year, according to the European Commission. That figure does not take into account any aid Cyprus may receive. De Facto Loss of Sovereignty In return for billions of euros for the debt-ridden country from the European bailout fund, the "troika," made up of the European Commission, the European Central Bank (ECB) and the International Monetary Fund (IMF), will essentialy take control of the Mediterranean island. The Cypriot government and representatives of the troika negotiated for almost five months over the terms of a bailout package, worth at least €17.5 billion ($22.8 billion). The negotiations produced the draft version of a 30-page Memorandum of Understanding (MoU), in which the troika dictates to Cyprus what steps it will have to take in the coming years, down to the smallest detail. President Christofias left no doubt as to who he blames for the disaster, saying: "It's true that the decisions of bank executives and the miserable control by the Cypriot central bank have cost Cyprus billions of euros." The amount of the aid package corresponds almost to the country's entire economic output in a year. According to the troika's plan, by 2016 Cyprus's national budget will be cleaned up enough that the country can hopefully make do without new debt. Creditors to Take Losses First Cypriot banks are also expected to make a contribution. Crisis-ridden institutions will no longer be supported solely by injections of cash from the European bailout fund. Cyprus has agreed a bailout deal with international creditors,

Lenders have suffered huge losses due to their heavy exposure to Greece. The deal, expected to include some 16bn euros ($20bn) of loans, will be officially confirmed later on Friday. But any deal would have to be ratified by parliaments in the eurozone countries. The Bailout Of Russian “Black Money” In Cyprus Jeff Randall, 22 Oct 2012 The intriguing element of Cyprus, however, is that what's at stake extends way beyond vulgar economic considerations. The politics of this place are complex, as befits its Byzantine past. Cyprus is in the eurozone but barely in Europe. Israel and Syria are about 300 miles from Nicosia; Brussels and Paris are 1,800 miles away. Turkey is an ever menacing presence, with its unrecognized regime in the north of the island. Hostility looms large. Then there is Russia, with which Cyprus shares an orthodox church. While Paphos's feline vagrants were being rounded up for extermination, big bears moved in to fill their places on the sunbeds. The newcomers are easy to spot, thanks largely to a sartorial style originated by Englebert Humperdinck's costumier and watches the size of grapefruits. The number of Russians visiting Cyprus has tripled in three years to more than 400,000 and many do not intend to go back. The official estimate of Russian residents here is about 50,000 but double that seems nearer the mark. Aside from the appeal of an agreeable climate and a low tax rate, the Russians' penchant for cash transactions prompts widespread suspicion that the island is becoming a giant laundromat for red-hot rubles. Cypriot authorities deny this. Cypern tog i veckan över ordförandeskapet i EU RE: Återföreningen mellan Öst- och Västeuropa? Öst- och Västeuropa har väl aldrig varit förenade, utom under Napoleon och några få år och med vissa undantag, i början av 1940-talet? Laiki Bank isn't alone. Other Cypriot lenders are also potentially in trouble. They lent about €25 billion to Greek borrowers. President Christofias is also looking for fresh funds in Moscow and Beijing. The Cypriot leader obtained his doctorate at the Moscow School of Social and Economic Sciences, and he still has many friends in the Russian capital today. The island itself is a popular base for wealthy Russians and Ukrainians, who use it to do business at home, thanks to favorable double taxation treaties. Other foreigners are also attracted to the island, thanks to a corporate tax rate of only 10 percent. In 2011, Cyprus borrowed €2.5 billion from Moscow, at an interest rate of only 4.5 percent. Riksbankschefen heter Panicos, Panicos Demetriades På söndag tar Cypern över ordförandeklubban i EU. Det enda roliga med det är att riksbankschefen heter Panicos, Panicos Demetriades Cypern borde aldrig ha fått komma in i EU så länge ön är delad. På andra sidan FN:s buffertzon, som går 18 mil tvärs över ön, ligger turkcyprioternas republik - endast erkänd av Turkiet. Zonen bevakas av drygt tusen FN-anställda; det kostar drygt 400 miljoner kronor om året. På norra Cypern finns 30 000 turkiska soldater och knappt 300 000 invånare. The findings of the Council of Europe Committee of Experts on the Evaluation of Anti-Money Laundering Measures and the Financing of Terrorism (MONEYVAL) ECB-ledamoten Athanasios Orphanides, centralbankschef i Cypern Ett "fruktansvärt misstag" och "jag vet inte hur det kan lösas", sade Athanasios Orphanides. I en första uppgörelse i juli föreslogs en skuldlättnad på motsvarande 21 procent. Denna uppgörelse har dock rivits upp och ersatts av ett förslag på att halvera skulderna, vilket motsvarar en nedskrivning på cirka 100 miljarder euro. Centralbankschef på Cypern? Ha, ha, ha, kanske Du tänker. Men skratta inte för tidigt. Bankerna på Cypern har en inlåning på 93 miljarder dollar. Undrar vad det är för pengar? Nov. 28 (Bloomberg) - Deposits in Cyprus’s banks fell 0.2 percent to 69.7 billion euros ($93 billion) in October compared to the prior, the Central Bank of Cyprus said. Interndevalvering Statens budgetunderskott kan inledningsvis komma att stiga i stället för att minska, eftersom skatteunderlaget krymper samtidigt som utgifterna för arbetslöshetsunderstöd o dyl. stiger. Tanken är emellertid att detta stålbad skall pågå i tillräckligt många år, så att priser och löner kan falla rejält jämfört med dessa länders handelspartner. Då kan sysselsättning och produktion börja stiga genom att förbättrad konkurrenskraft får exporten att öka samtidigt som import kan ersättas av inhemsk produktion. Unga och välutbildade kommer att utvandra, vilket är en nödvändig säkerhetsventil i en valutaunion. Det är så den USA:s valutaunion överlever. Och slutligen, när deflationen är igång, stiger realvärdet av alla skulder och kan tvinga fram ökat sparande, som sänker efterfrågan ytterligare. Deflation är inte att leka med. I Sverige och Finland klarade vi liknande grundproblem 1991-1993 med ganska små påfrestningar. Det berodde på att åtstramningarna kunde kombineras med nominell devalvering, eftersom vi hade egna valutor. Valutaunioner är inte heller att leka med. * Även om man, på något sätt, skulle kunna ta hand om medlemsländernas skulder (Reuters) - Greeks protesting at austerity measures demanded by foreign lenders blocked a major national parade on Friday Greek protesters call president "traitor" 28.10.2011 Rolf Englund: Grekland ska folkomrösta om det nya EU-stödpaketet, "Om det grekiska folket inte vill ha det så kommer det inte att godkännas", säger Papandreou till nyhetsbyrån AFP. EU-ledarna: Räcker inte 50 % nedskrivning för Grekland, det hade vi ingen aaning om? Jag har lyssnat i nästan tre timmar idag 12/10 på Studio 1:s genomlysning av den europeiska skuldkrisen utan att ha blivit så mycket klokare. Den fråga jag väntade att skulle besvaras var Hur kan det vara klart att Grekland ska få sina 8 miljarder euro om man samtidigt tror att Grekland ska gå i konkurs Borde Grekland behålla euron? Det som Örn visar i ett diagram om den grekiska valutans övervärdering är något som Persson och Flam borde ta till sig. Efter eurons införande har emellertid den nominella växelkursen låsts (vid 175 drachm/DM). Samtidigt har den reala växelkursen försämrats med nästan 20 procent genom snabbare löneökningar i Grekland än i Tyskland. Det betyder att den grekiska valutan borde devalveras med nästan 25 procent för att komma i paritet med Tyskland. Om inte annat brukar det finnas mycket tyska turister i Grekland, som nu tycker att det blivit dyrt att turista där. Att långsamt sänka de grekiska lönerna i den ordinarie lönebildningen? Varför skulle det vara enklare? Jag tror att folk i allmänhet lider av penningillusion och inte är konstruerade som rationella nationalekonomer. Försöken att motivera att Grekland ska finnas kvar i EMU och behålla euron för att det är bäst för grekerna själva verkar inte speciellt välgrundade och trovärdiga. Der frühere Chefvolkswirt der Europäischen Zentralbank, Otmar Issing, fordert einen Schuldenschnitt für Griechenland und hält in der Folge einen Ausstieg des Landes aus der Eurozone für unvermeidlich. In einem Interview mit dem stern sagte der langjährige Notenbanker, er halte es für "ausgeschlossen" dass Griechenland mithilfe radikaler Sparmaßnahmen wieder auf die Beine komme. Das Land würde im kommenden Jahr eine Schuldenquote von 160 Prozent des Bruttoinlandsprodukts erreichen Mats Persson, Grekland och de rationella förväntningarna Greklands oväntat stora underskottet för 2011 på 8,5 procent av BNP Greklands "unexpectedly harsh recession" Grekland borde aldrig ha gått med i euron, det vet vi nu. Det är obegripligt hur EU kunde blunda för att hela Europa inte är som Tyskland. Greklands konkurs - en studie i panik?

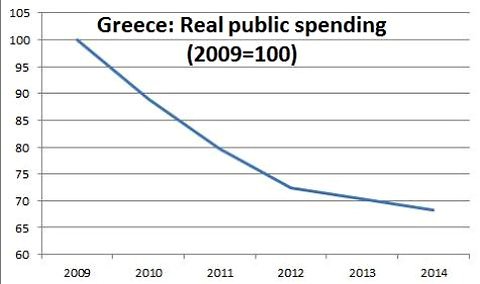

Om sparpaketet inte går igenom blir det inte några 8 mdr € i övertagande av förfallande lån. Då har vi kris på onsdag. Arga greker som skriker antikapitalistiska slagord utanför parlamentet fördjupar krisen, Arga greker gör andra européer arga. En våg av bitterhet drabbar invånarna i EU:s nettobetalande länder; här har EU pumpat in otaliga miljarder sedan Grekland kom med 1981! Hårt arbetande tyskar frågar sig varför de ska subventionera den grekiska livsstilen. Någonstans i Berlin hukar så Angela Merkel och tänker på hur väljarna straffat henne i tidigare delstatsval. Medan desperata liberaler i FDP försöker svida om till euroskeptiker. Grekland måste rimligen gå i konkurs, ingen kan förstås säkert överblicka konsekvenserna. Men det finns kalkyler som pekar på att det blir betydligt billigare för Tyskland och Frankrike att rädda sina egna banker i stället för att köra fler repriser av programmet Skuldkris. Låt också Grekland stanna i EMU, för det är också vad grekerna vill. Grekland En grekisk statsbankrutt skulle inte i sig välta hela euroområdet. Kruxet är att åtskilliga länders banker sitter med stora innehav av statsobligationer i både Grekland, Italien och resten av Sydeuropa. Ingen vet exakt hur riskbilden ser ut och allt färre litar på varandra. Kommentar av Rolf Englund: Rubriken för ledaren är: "Eurokrisen: Fler behöver visa skuldmedvetenhet" Rubriken fick mig att tro att det skulle handla om att de som arbetat för införandet av euron, DN, Svenska Dagbladet och nästan hela det övriga etablisemanget, som inbillar sig vara en elit, skulle visa skuldmedvetenhet och ånger. Men icke. Fler behöver visa skuldmedvetenhet, skriver DN Förut ledde väl inte budgetbekymmer i Grekland till risk för sammanbrott i världsekonomin ? Charles Gave beskriver situationen i Grekland som ett ”lågintensivt inbördeskrig”. Även om Grekland misskött sin ekonomi går det inte att komma ifrån att Ett av de centrala argumenten på nej-sidan mot euron var att Europa inte är ett ”optimalt valutaområde” – vilket betyder att euroländernas ekonomier helt enkelt är så olika och aldrig helt kan vara i fas med varandra att en gemensam valuta och ränta inte kan passa alla samtidigt. Som nejsägare till euron kan jag uttala de fruktansvärda men underbara orden: Vad var det vi sa? Nils Lundgren: EMU och teorin för optimala valutaområden Och då skrev jag i Financial Times om eurobonds och Hayek (och Grekland) Greklandskrisen på 30 sekunder Ledaren för Greklands största konservativa oppositionsparti säger att det enda sättet – Enda lösningen är val, så att folket vilja kommer till uttryck, sade Ny demokratis ledare Antonis Samaras i ett tal i Thessaloniki på lördagen.

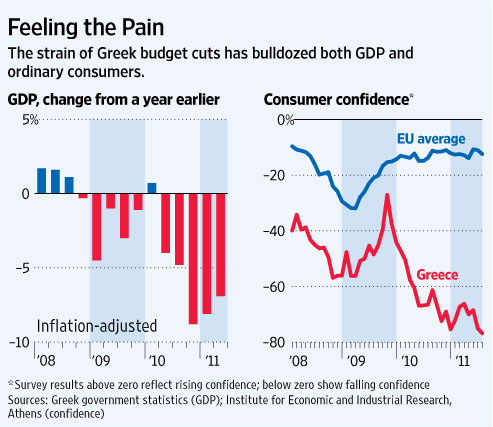

Rolf Gustavsson, demokratin och sockerbagare Grekland, demokratin och det nu aktuella pladdret Sveriges erfarenheter från 1990-talskrisen kan tas som exempel. Vad som kan locka med att överge euron är att Grekland får möjlighet till devalvering. Problemet för till exempel Grekland är att kostnaderna under ett antal år stigit i förhållande till andra euroländer. Calmfors pekar på Eurokrisens huvudproblem, kostnadsläget * Grekland ska införa en ny fastighetsskatt I lördags sade Venizelos att Greklands ekonomi i år väntas krympa med 5,3 procent i år, vilket är mer än man trodde tidigare. Full text

Greklands BNP krympte med 2 procent i fjol. I år (2010) och nästa år (2011) väntas BNP minska med 4 respektive 2,6 procent, Sedan kommer vändningen, i Sardelius diagram. - Men vad är det som får BNP att vända upp, trots åtstramningarna, vid fast växelkurs, frågade jag från golvet. Sardelius svarade att det var genom utbudspolitiken, borttagande av onödig byråkrati mm. Jag skrattade. - Skrattar Du, sade Sardelius. Ja, sade jag. Det är kanske fel att skratta i en så allvarlig situation. Det är ju, som Sardelius själv visade i ett annat diagram, nödvändigt med en stark tillväxt för att kunna beta av statsskulden.

Jag är väl inte så mycket skickligare ekonom än dom andra i salen, från Riksbank och Finansdepartement med mera. Dom förstod nog också. Men dom teg. Det är allvarligare att folk tiger än att någon skrattar. Hellre skratta än att vara kollaboratör. Top of pageDebatterade igår euron med Olle Schmidt i Studio ett. Låt Grekland lämna euron The Holy Roman Empire, (Habsburg and all that)

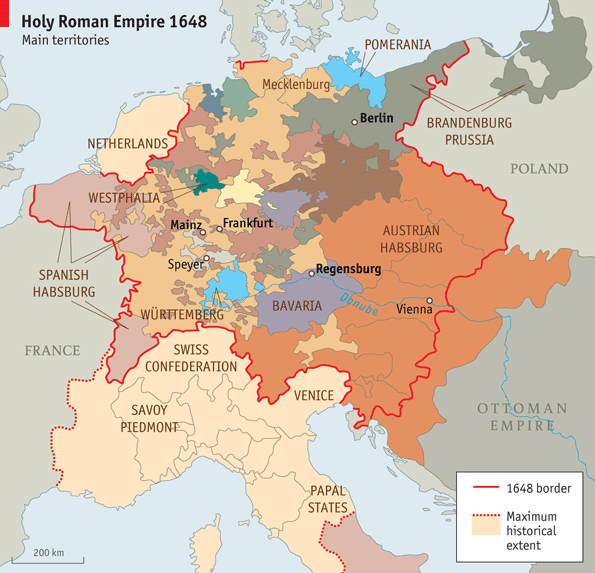

Summits were more fun in those days. When Ferdinand III, the Habsburg monarch of the Holy Roman Empire, arrived in Regensburg, the Brussels of its time, in late 1652, he brought 60 musicians and three dwarves. There were sleigh rides, fireworks and the first Italian opera ever performed in Germanic lands. On the hot-button issue of religion, in particular, each prince should independently determine whether his territory was to be Catholic, Lutheran or Calvinist. But then one more Habsburg, Ferdinand II, was tempted to have a good last go at absolutism. Already king of his hereditary lands and soon to be elected emperor, he was also a strict Catholic and rather offended when, in 1618, cranky Protestants threw three Catholic bigwigs out of a window in Prague (though all three survived the plunge). He sent soldiers, and thus ensued a series of increasingly messy wars. One could see the origins of today’s crisis, and the danger in the much longer term, in Germany’s rapid growth after reunification with East Germany (which was largely the old Brandenburg-Prussia, as it happens). Historians are a cautious bunch, but Mr Hartmann dares make that comparison. The EU, prompted by Germany, in 1997 signed a “stability and growth pact” to impose fiscal discipline on member countries and to avoid crises. But that pact lost its bite a decade ago once Germany itself broke it. The EU should have taken Germany to task, but Gerhard Schröder, the chancellor, got off scot-free. The EU can discipline Ireland or Greece, but probably not Germany or France. "When the Holy Roman Emperor, Henry VI (1190-1197), demanded money and men for his projected crusade, Holy Roman Empire, Wikipedia A History of Greece,Amazon The Holy Roman Empire and the Habsburgs, 1400–1600 Rome, Habsburg and the European Union Portugisiska och grekiska bönder vill helt enkelt inte att nogräknade tyskar och svenskar i demokratisk ordning reformerar, det vill säga lägger ned, deras jordbruk. Möte på torsdag mellan Frankrikes nye finansminister Francois Baroin och hans tyske kollega Wolfgang Schäuble Grekland, Persson och Jens Henriksson ”Mordet på EU-expressen” Irlands underskott exploderade efter att landet tvingades rädda sina banker och i Spanien är problemen lika mycket situationen i banksystemet som misskötta statsfinanser. Underskotten var en konsekvens av krisen: mer än en orsak. Tyska banker har lånat ut 500 miljarder euro till Portugal, Irland, Grekland och Spanien. Skulle de skriva ner sina skulder kommer förlusterna i det statligt ägda tyska Landesbanken att bli enorma. Neil Ferguson i Newsweek Varför ingen har skrivit en avslöjande insiderskildring från Ja till euro-kampanjen 2003,

måste vara ett av de största mysterierna i svensk politik. Skulle Grekland brännmärkas med "default" av S & P eller Fitch kan den grekiska skuldkrisen förvärras snabbt. Grekisk stötesen En stötesten har varit om och i så fall hur privata långivare ska bidra. Förhoppningen är att banker och andra investerare frivilligt ska gå med på en förlängning av skulderna, att de ska köpa nya grekiska statsobligationer när de gamla löper ut. Mer om hur nästa grekiska stödpaket kommer att utformas lär beslutas den 11 juli då euroländernas finansministrar träffas på nytt. Grekland Det första alternativet innebär att hunden viftar på svansen, det andra att svansen ska vifta på hunden. Problemet är att Grekland som medlem i eurozonen inte har en egen valuta, och därmed inte kan devalvera. Alltså rekommenderar IMF, ECB och euroländerna det senare alternativet. Men Greklands ekonomi är inte i sådant skick att landet kan hålla jämna steg, i konkurrenskraft och tillväxt, med de dominerande euroländerna. Grekland hör inte hemma i eurozonen. Den amerikanske ekonomen Herbert Stein har skrivit: ”If anything cannot go on forever, it will stop.” Hans slutsats kan kritiseras för att vara ytterst deprimerande. Härav följer inte att den är felaktig. De har inte läst Herbert Stein. Jeffrey Sachs, Grekland och Persson Jeffrey Sachs och chockterapin i den fd monetära unionen Jugoslavien Man bör inte avfärda alternativet att landet lämnar valutasamarbetet. Stefan Fölster menar att en nedskrivning av Greklands skulder är oundviklig. Han pekar på att Grekland faktiskt genomfört många åtgärder vilket kanske inte är det intryck man får när media rapporterar från landet. Det finns egentligen inte någon Eurokris. Det är en i Sverige vanlig uppfattning att det var Göran Perssons motsvarande nedskärningar som satte fart på den svenska ekonomin. Nedskärningarna räddade landet, tror många. USA:s president och alla vi andra borde inte bekymra oss om Liran och Drachman Innan månadsslutet ska man dessutom kunna visa upp konkreta, klubbade besparingsplaner för statskassan på 28,4 miljarder euro, exempelvis genom att sälja ut några statsägda bolag till privata intressenter, helst så många som ett stort bolag var tionde dag om kalkylen ska hålla. /Grekland skall/ sälja ut några statsägda bolag till privata intressenter, helst så många som ett stort bolag var tionde dag om kalkylen ska hålla. En klentrogen journalist frågade hur i all sin dar man kunde tro att den grekiska regeringen skulle kunna sälja av ett statligt företag var tionde dag från och med nu. –De bara måste göra det, svarade eurogruppens ledare Jean-Claude Juncker kort. Dagens Nyheter och Svenska Dagbladet är pinsamma om EMU och Grekland Baksidan av de massiva nedskärningarna är att ekonomin krymper, Tyskland och Frankrike har enats om att snällt be privata investerare i grekiska statsobligationer att ta en liten del av notan. Men Grekland skulle behöva hjälp av några antika gudar för att ta sig upp ur dödsriket. Alternativt en ordnad nedskrivning av skulderna. Andes Borg å ena och å den andra sidan om eurokrisen Tyskland vill att privata investerare som banker och försäkringsbolag, Men andra varnar för att det skulle ses som att Grekland ställer in sina betalningar och därmed är statsbankrutt. Robert Bergqvist: Samhällskollaps runt hörnet Greklands kris är så djup att landet kan tvingas att lämna eurosamarbetet. Svenska Dagbladet åter i EMU-debatten! Slutsatsen i ledaren om Grekland är att "Ännu kan det faktiskt sluta lyckligt", en ovanlig men därför kanske intressant uppfattning. Strukturreformerna är bra anser SvD "oavsett om de på sikt klarar av att blåsa tillräckligt liv i landet för att vända den ständigt stigande statsskuldskurvan". Men avsikten med reformerna/nedskärningarna är väl just att "att blåsa tillräckligt liv i landet för att vända den ständigt stigande statsskuldskurvan" och därmed återupprätta Greklands kreditvärdighet? The bail-out strategy that rescued Europe’s peripheral economies is proving insufficient. Resultatet kommer att bli en helt och hållet frivillig skuldomläggning Det centrala problemet är ett dödläge mellan bailout-rädda politiker och instabilitetsfruktande centralbanker. Översättning av RE, för engelsk originaltext klicka här Pengarna "till Grekland" går till bankerna New York Times dömer ut försöken att "vinna tid" genom nya pålagor på det grekiska folket Fast i skuldfällan - Grekland stramar åt men inget hjälper Att skriva ned skulderna, och låta privata investerare ta sin del av förlusten, är den ekonomiskt realistiska lösningen. Utan tvekan finns det risker. Banker i Grekland, och i andra EU-länder, kan gå omkull och det måste finnas beredskap att stötta finanssystemet där det behövs. Diskussioner har förts om så kallad mjuk nedskrivning av Greklands skulder, genom att man förlänger löptiden på statspapper. Men kreditvärderingsinstituten hotar att likställa det med statsbankrutt. Och ECB säger tvärt nej till alla sorters nedskrivningar, bland annat för att banken själv äger massor av grekiska obligationer som skulle förlora i värde. Snaran dras åt kring Grekland Förhoppningarna är att hälften av de 60-70 miljarder euro som Grekland behöver till 2013 ska kunna klaras av utan ytterligare lån. Can Greece learn the economic lessons Argentina missed? In Argentina's case, the government struggled to keep the economy on the rails, even though it had help from the International Monetary Fund, for most of 2000 and 2001, before President Fernando de la Rua was forced to resign.

For a vision of how the Greek debt meltdown is going to end, look no further than the International Monetary Fund's post mortem into a similar crisis that came to a head almost exactly a decade ago - Lessons From The Crisis In Argentina. The parallels with Argentina are so strikingly exact as to bear repeating at length. Substitute the word Greece for Argentina in the IMF's analysis, and euro for currency board, and you'd have a near perfect account of the present crisis, all written nearly eight years ago. Here's what happened in Argentina. Lessons from the Crisis in Argentina Default, Devaluation, Or What? Officials warned, however, that almost every element of the new package faced significant opposition from at least one of the governments and institutions involved in the current negotiations and a deal could still unravel. One senior European official involved in the talks, however, said ECB objections could be overcome if the rescheduling was structured properly. Officials think Greece will be unable to return to the financial markets to raise money on its own in March Skrattar bäst som skrattar först om Grekland Grekland står nu på randen till statsbankrutt. Tusentals greker i fredlig protest mot sparplaner För första gången under den pågående grekiska ekonomiska krisen anordnades inte en demonstration av några fackföreningar, organisationer eller politiska partier, utan spontant via internet, via Facebook Bundesbank President och Grekland – “the central bank equivalent of nuclear deterrence: Kaos väntar om Grekland faller Greklands regering antog ett nytt paket med utgiftsnedskärningar och försäljningar av statlig egendom Greklands regering kommer inom de närmaste dagarna att annonsera åtgärder för att Rolf Englund: Grekland har cirka elva miljoner invånare. Den nya besparingen/nedskärningen motsvarar cirka 5.000 kr per capita, Euroländernas del av det lån på 110 miljarder euro som förhandlades fram förra våren ligger på 80 miljarder euro. Dels den ränta som exempelvis Tyskland eller Frankrike själva betalar för att låna, men även en extra riskpremie som förra året bestämdes skulle ligga på 3 procent. Det gör att Grekland hittills har betalat över 6 miljarder kronor i riskpremie – en summa som flutit direkt in på eurostaternas konton runt om i Europa. Om Grekland ställer in betalningarna, alternativt skriver ned värdet på sina utestående lån, Greklands affärsbanker har använt grekiska statsobligationer som säkerhet för att få låna pengar av centralbanken i Frankfurt. Vid årsskiftet var bankernas skulder till ECB uppe i 94 miljarder euro. Grekland har ingen chans att klara sig undan en omstrukturering av sina skulder. Läget i Grekland blir allt allvarligare. Ekonomin skenar och missnöjet bland människor växer. Skrattar bäst som skrattar först om Grekland Hans Werner Sinn, chef för det ansedda IFO-institutet.

I helgen aktualiserade den ansedda ekonomen alternativet att Grekland lämnar eurozonen. zc Financial Secretary to the Treasury Mark Hoban, MP and Jack Straw, a former foreign minister, about Greece and the euro Eventually, governments pursuing ever more austerity Jan Kees de Jager, the Dutch finance minister Germany and Greece flirt with mutual assured destruction Bild Zeitung populism has prevailed. Germany is pushing Greece towards a hard default, risking the uncontrollable chain reaction so long feared by markets. Greece can, if provoked, pull the pin on the European banking system and inflict huge damage on Germany itself, and Greece has certainly been provoked. Germany’s EU commissioner Günther Oettinger said Europe should send blue helmets to take control of Greek tax collection and liquidate state assets. This has sent the economy into a self-feeding downward spiral, crushing tax revenues. The policy is obscurantist, a replay of the Gold Standard in 1931. It has self-evidently failed.För både Moderater och Folkpartister verkar eurokrisen bara handla om att justera några tekniska detaljer, The German chancellor remains a believer. "voluntarily" The current conflict centers on the planned second bailout package for Greece, worth €130 billion and agreed to in principle at an EU summit last October. Greece needs the first payment of this fund in March to avoid insolvency. Part of this package is the 50 percent debt haircut for Greece that is now under negotiation. It envisions Greece's private creditors - primarily banks, insurance companies, investment funds and hedge funds - voluntarily agreeing to the write downs. Together, they hold some €205 billion in Greek bonds. Since May 2010, the ECB has purchased sovereign bonds from crisis-stricken euro-zone member states worth €213 billion. An estimated €55 billion of that are Greek bonds. when Greek banks borrow from the ECB, they post Greek sovereign bonds as collateral. The committee representing Greece's lenders said that some parties It said discussions were "paused for reflection on the benefits of a voluntary approach" without stating when they would resume. The alternative to a voluntary debt write-off is likely to be an outright default by Greece - a failure to continue repaying its debts. Some lenders have also privately expressed their objection to the agreement, because it is being devised in a way to avoid causing payouts on credit default swaps - financial contracts taken out to provide insurance on a Greek debt default. The European Central Bank - which has bought up a significant share of Greece's debts as part of efforts to rescue the country - is not participating in the talks and will not accept any write-off of the debts it holds. The biggest danger is Greece

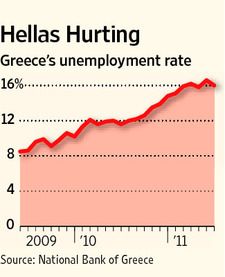

An IMF report on Greece just before Christmas was sobering. It says GDP probably shrank by 5.5-6% last year and may fall by a further 3% in 2012. Deepening recession makes it harder for Greece to meet its budgetary targets. The pace of reform and of privatisation has been slower than hoped. The delay in reaching an agreement with private-sector creditors on the losses that they should bear on Greek government bonds has not helped. The IMF reckons that, if all private bondholders agreed to take a 50% “haircut” (ie, lose half the value of their bonds) and if Greece were to meet its fiscal targets, public debt might eventually fall to 120% of GDP. Skrattar bäst som skrattar först om Grekland Horst Reichenbach One answer is playing out now as a Greek tragedy: It would be Europe’s worst nightmare: after weeks of rumors, We’re not occupiers, says Greek task force The one form of adjustment that is made a condition of financial support is ever more severe fiscal austerity. Vad journalisterna och EU-eliten missade George Papandreou also personally promoted the man behind the drafting of this Referendum Law. He is Interior Minister Haris Kastanidis, and in the past he has called into question whether the austerity measures being applied to Greece are too painful. A passionate believer in democracy and human rights, Kastanidis’ attitudes have been framed by a youth spent under the Colonels: his father was persecuted by the Colonels, to the point where his health failed and he died young. Greece’s prime minister unexpectedly announced a referendum to approve a second EU bail-out deal for his austerity-hit country, Europe’s crisis is all about the north-south split Greece prepares to default within the euro – the worst of all possible worlds Such a package would be tremendously expensive: in the trillions. Daniel Hannan about illelgal eurobonds Calmfors pekar på Eurokrisens huvudproblem, kostnadsläget The Greek people are increasingly asking what the point is of this pain. They see years and years of austerity ahead. In their view, they are being forced to accept deep cuts to protect the French and German banks. Again and again people ask where all this is heading. What is the end game? During the last two years the economy has shrunk by 10%. It is one of the reasons why Greece failed to meet its targets. And yet - in the eyes of many - the same medicine is being repeated. Unemployment is now at 16.3%. So Greece continues on its painful path. Time is bought for Europe's banks to make their balance sheets better able to withstand losses. Democracy: The European crisis Sixteen months after a landmark bailout In a vertiginous trading session Friday that also saw the surprise resignation of a top European Central Bank official, Greek woes once again unnerved investors. The euro slumped sharply against the dollar, falling under $1.37. Bourses in Paris and Frankfurt suffered big losses, led by banks, who would bear the brunt of a meltdown in Europe's periphery. Will the eurozone break up? Lagarde warns major economies of recession * In an eloquent speech in Washington today, the head of the IMF, Christine Lagarde, repeated her call for policymakers to act together to confront today's troubling times.

"They must reclaim the spirit of 2008, or the spirit of 1944. The Wilsonian spirits". Investors are right to be relieved that central banks have today reclaimed 'the spirit of 2008'. But we should not forget to be disappointed that it is still required. As I said on the 10 o'clock news last night,

For Europe's elite, the idea of a country leaving the euro is anathema. And that will push them towards shouldering Greece's debt. International lenders put Greece on notice that it is in danger of losing its next €8bn tranche of bail-out loans

Officials from the “troika” – made up of the European Union, International Monetary Fund and European Central Bank – abruptly suspended talks and left Greece on Friday in a warning to Athens before negotiations resume in 10 days. Evangelos Venizelos, the finance minister, said the government had no plans to adopt extra austerity measures, blaming a deeper than expected recession for spending overruns and missed revenue targets. * Låt Grekland lämna euron * "Det gäller bara Grekland", Mycket fiffigt, Too clever by half, Cconcern at the approach taken by BNP Paribas and CNP Assurances Banks and insurers that used market prices suffered a bigger hit. Royal Bank of Scotland wiped £733m from the value of a £1.45bn Greek government bond portfolio – a 51 per cent cut. Griechenland könnte laut dem weltweit führenden Versicherungsmakler Aon ein Bürgerkrieg drohen. East Germany Was and Is Greece Greece, Ireland and Portugal Wolfgang Schäuble, German finance minister, said a rethink was needed Greece, Portugal and Ireland Moment of truth for the eurozone Within just five years, the Greeks want to cut spending by the equivalent of 17 percent of their total GDP in 2010.

The Greek rollover pact is like a toxic CDO If you take some time to work through the arrows and boxes, you see relatively quickly that this complex structure is not a private sector participation at all. Rather it is a private sector bail-out. It is also inevitable that Greece will default on its coupon payment at some point. Full text via Rolf Englund blog This isn't just a mortgage or housing crisis. Greece’s austerity plan looks doomed to fail. Greece’s politicians reckon that so long as they pretend to fix their country, the EU will hand over the money whether the plan succeeds or not. After all, who wants to pull the plug on Greece if that risks contagion across the euro zone? The plan seems to do too little to help Greece, and too much to help the banks. It reduces the potential loss they might suffer were Greece to default and lets them take some money out now. It also rewards them with interest payments that may rise to 8% if the Greek economy rebounds. For Greece, the bargain is far less compelling. The 30-year plan does nothing to reduce Greece’s debt burden and could complicate any eventual restructuring. The difficulties facing the real economy, the contraction of bank credit in combination with ongoing capital flight and record unemployment, in particularly among young people, make Papandreou’s endeavors this week a herculean task. What we are currently witnessing on the streets and squares across Greece is the next stage of the country’s two-year long crisis. It now involves the collapse in trust between citizens and Greek-style parliamentary democracy. Jens Bastian is a senior economic research fellow at the Athens-based think tank ELIAMEP (Hellenic Foundation for European & Foreign Policy). He is currently a Visiting Fellow for the Political Economy of Southeast Europe at St Antony’s College in Oxford, U.K. Throughout the eurozone crisis the EU has insisted that Greece carry out the impossible When an outcome is inevitable, it is necessary to plan for it. The economy looks extraordinarily uncompetitive. The most telling indicator is the combination of the still huge current account deficit with a deep recession Without a surge in exports, it will be impossible to return to sustainable growth. Such a surge will require a big reduction in nominal costs. If this is feasible at all, which I doubt, this will raise the ratio of debt to GDP still more. What is the case for persisting with lending ever more and, in the process, taking a larger proportion of the liabilities of the Greek government on to public sector balance sheets? Other countries have achieved the kind of permanent budgetary adjustment that the IMF is looking for in Greece, You're talking about going from a primary deficit - that's the deficit, before interest payments on the debt are considered - of 4-5% of GDP in 2010 to a primary surplus of around 10% of GDP. If that's not going to happen, Dumas says Greece will suffer more from prolonging the agony. The country owes about 325 billion euros and has an annual gross domestic product of about €225 billion. Why spend seven hours behind closed doors, only to decide to wait and see? Threats are only worth making if those making the threats could actually carry them out How can you revitalise Greece? Every intervention so far has pretended that the crisis is one of liquidity, which can be solved by making loans to the troubled banks and governments in question.