IMF-pengar till Euron

Related: Greece - Europakten 2011

Finanskrisen - Eurokrisen

Germany digs in heels as world anger mounts over its toxic trade surplus, the world’s largest in absolute terms

Maury Obstfeld, the IMF’s chief economist, said Germany’s current account surplus – 8.5pc of GDP, and the world’s largest in absolute terms at almost $350bn (£252bn) – is 4.5 percentage points of GDP beyond what can be justified by demographic arguments.

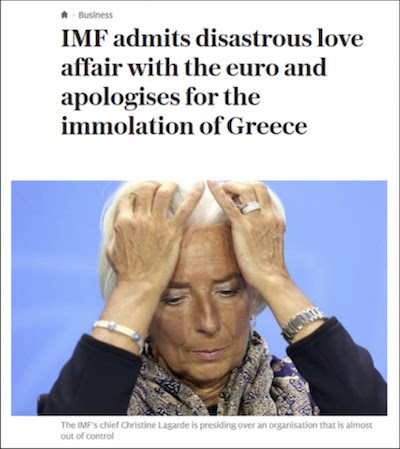

Ambrose 18 January 2018

For those of us who have been following the Greek economic tragedy for many years,

much of the European view continues to defy economic logic – and for a simple reason:

European politicians worry about the domestic political consequences of granting Greece debt relief, especially ahead of Germany’s federal election in September.

Mohamed A. El-Erian, Project Syndicate 21 June 2017

The grudging short-term compromise between the IMF and Europe comes after months of sometimes acrimonious discussions. For the sake of Greece, and for the credibility of their own future interactions, they should view it as a stepping-stone to the (long-delayed) definitive resolution of Greece’s economic and financial malaise.

Greek citizens have waited, and suffered, long enough.

“extend and pretend”

Europe's Unserious Plan for Greece

The latest deal on debt won’t work, and everybody knows it.

By The Editors, Bloomberg 21 June 2017

Euro-zone finance ministers have unlocked a payment of 8.5 billion euros.

This will let Athens make debt repayments of 7 billion euros that fall due next month.

But there’s still no agreement on how to get Greece’s debt burden under control.

The IMF had previously insisted that this question should be settled now.

This protracted game of “extend and pretend” serves nobody’s long-term interests: not those of the Greek government, the International Monetary Fund or, most of all, the people of Greece.

The blow to the credibility of the IMF could prove to be lasting damage. The fund points to its refusal to disburse money at this point as proof it’s serious about debt relief. Yet it remains a partner in a project that, by its own analysis, is bound to fail.

Under the compromise deal, the IMF is set to formally join the rescue programme,

but delay providing any money to Athens until the eurozone provides more clarity on what debt relief it is prepared to offer.

FT 15 June 2017

Ms Lagarde said that while ministers at Thursday’s meeting had further fleshed out debt relief options for Greece,

what was on the table still did not allow the fund to assess whether Athens’ debts were sustainable.

The debt relief “needs to be better clarified”, she said. “This is something that will need to happen.”

The European Financial Stability Facility and

the European Stability Mechanism will raise a combined €61.5bn (600 miljarder kr)

in financing this year

FT 1 June 2017

ECB’s Coeure calls for clarity on Greece debt relief before QE inclusion

Mehreen Khan, FT 31 May 2017

Greece and its European creditors failed on Monday to agree on the next batch of bailout loans

but officials said the deal should be reached at their next meeting in three weeks.

Deutsche Welle, 23 May 2017

After more than eight hours of talks in Brussels, finance ministers from the single currency bloc and the International Monetary Fund (IMF) were unable to secure an agreement on the sort of debt relief measures the Athens government can expect when its current bailout program ends next year.

Greece could default on its debts in July if it can't repay some 7.3 billion euros

The Eurogroup is asking Greece to do something unprecedented

Historical experience—not just Greece’s experience, but that of a typical advanced country—

is inconsistent with the primary surplus paths that would make Greece’s current debt sustainable.

Matthew C Klein, FT 13 april 2017

Christine Lagarde said that eurozone creditors must provide considerably more detail on debt relief for Greece

before the fund will take a decision to join the country’s bailout programme.

“There cannot be a specific case for any particular country.”

FT 12 April 2017

Ms Lagarde insisted there could be no special treatment of Greece when it comes to any fund decision on joining the bailout.

“If and when I put a programme to the board of the IMF it will have to comply with the rules of any…programme,” she said.

“There cannot be a specific case for any particular country.”

IMF under pressure in Washington over Greek bailout

Conservatives in US Congress say Europeans should solve the crisis on their own

FT 17 March 2017

“The IMF isn’t a fund to rescue political parties in creditor nations, nor should it be a junior partner to outside organisations that lack the commitment to do their work,” he said.

“For seven years now, the IMF has been used to shield eurozone officials from their voters, which has tarnished the Fund’s reputation,

prolonged Greece’s misery, and put off hard choices about Europe's future that must be made regardless.”

A failure to tell the truth imperils Greece and Europe

If the IMF pulls out, Europe will be free to mismanage the crisis on its own

Wolfgang Münchau, associate editor of the Financial Times, 12 February 2017

Greece

European nations are over-represented on the board relative to their size in the global economy.

Wielding that power to dissuade the fund from demanding debt relief from eurozone governments

is a clear conflict of interest and poses a threat to the fund’s credibility and independence.

Eurozone governments have behaved poorly on this issue. They deserve to be defeated.

FT Editorial 9 February 2017

IMF board split over bailout terms for Greece

Rare public division amid stand-off with EU over country’s ‘explosive’ debt path

FT 7 February 2017

IMF and EU policymakers take Greece bailout spat online

War of words breaks out between officials over austerity measures

FT 15 December 2016

The Eurogroup is the real villain in Greece today, not the IMF

Ambrose Evans-Pritchard 14 December 2016

Greece cannot be condemned to austerity for ever

Myths about the country’s rescue package must be confronted

Pierre Moscovici, European commissioner for economic and financial affairs, taxation and customs,

FT 15 December 2016

Eurozone and IMF splits remain over Greece rescue

Short-term debt relief deal falls shy of fund joining €86bn bailout

FT 5 December 2016

A fiscal surplus too far for the Greek economy

The EU’s softening attitude to public deficits should include Greece

FT editorial 23 November 2016

By the end of this year, if those lenders cannot agree a deal,

the IMF may decide finally to detach itself from the rescue programme and leave Europe to sort out its own mess.

EU har funnit sig i att Grekland aldrig kommer att kunna (eller vilja) betala tillbaka sina skulder.

Alla miljarderna har gått upp i rök. Fast av principiella och framför allt inrikespolitiska skäl kan man inte säga det öppet,

eftersom det vore detsamma som att peka ut den som kommer att bli tvungen att ta hand om notan: de europeiska skattebetalarna.

Richard Swartz, kolumn DN 22 oktober 2016

IMF has argued stridently that /Greece/ needs relief on the fiscal and debt front in order to generate growth.

The IMF is right. Greece has made some notable changes to its economy, albeit from an extremely dysfunctional base.

But structural reform is generally contractionary in the short to medium term.

It needs to be accompanied by supportive fiscal policy.

FT Editorial 11 October 2016

The IMF paper said the slow recovery had been made worse by the fact that

what growth there had been “bypassed many low-income earners” and

“raised anxiety about globalisation and worsened the political climate for reform”.

FT 1 Sepember 2016

To escape sluggish growth and boost countries’ economies,

the fund has been urging policymakers to more aggressively employ the three prongs of

monetary policy, structural reform and fiscal measures.

IMF Paper

We Need Forceful Policies to Avoid the Low-Growth Trap

Christine Lagarde

The IMF and the Crises in Greece, Ireland, and Portugal

IMF/IEO, July 2016

474.000 hits about this at Google

Ambrose knows how to turn a phrase.

“Calamitous misjudgments” is a good way to describe the way the IMF, along with the EU and ECB, has handled the continent’s sovereign debt crisis,

which remains unresolved even now, six years later.

An Inheritance of Incompetence, John Mauldin, 13 August 2016

Bretton Woods

With currencies now effectively free-floating, the IMF found itself with little reason to exist. Did it go off quietly into the night? Of course not.

When has any bureaucracy ever volunteered to shut itself down? IMF officials simply redefined their mission.

The IMF would now provide financing to nations with balance of payments issues, makes loans to nations in distress, and publish lots of economic research.

My real purpose here is not to point the finger at the IMF but to point out where its problems are part and parcel of a greater problem in global institutions.

During the next global recession we are going to see a continuation of the same approaches to crisis solving that we’ve seen in the past,

based on the theories of defunct economists mixed with personal and institutional biases.

The bias developed because, as Ambrose says, the European elites in the IMF have waged a massive love affair with the euro. And like many in love, they simply could not see the flaws in the object of their affection, the common currency of the eurozone. It was at the very foundation of the whole European project in their eyes.

The IMF-EMU love affair led the agency to accept reports and reassurances from eurozone officials at face value, without the same kind of verification they routinely demand from less-developed countries.

Long before the deluge, people within the agency had argued that the euro system was fundamentally flawed and would eventually fall apart. Those who said so found themselves overruled and even punished.

Calamitous: causing great harm or suffering, Webster

In 2013 economists at the IMF rendered their verdict on these austerity programmes:

they had done far more economic damage than had been initially predicted, including by the fund itself.

What had the IMF got wrong when it made its earlier, more sanguine forecasts?

It had dramatically underestimated the fiscal multiplier.

The Economist print 13 August 2016

Highly Recommended

IMF’s top staff misled their own board, made a series of calamitous misjudgments in Greece

Ambrose Evans-Pritchard, Telegraph 29 July

The Myth of Austerity and Growth

Noah Smith, Bloomberg 22 June 2016

The principles of Keynesian fiscal policy -- which have slowly been coming back into vogue -- say that tightening spending is the worst thing you can do in the middle of a recession. More generally, it isn’t clear just how austerity is supposed to work its positive magic. The main claim seems to be the rather vague idea that lower budget deficits increase business confidence.

Blanchard has shifted his stance. In a 2013 paper with Daniel Leigh, he showed that the IMF had been consistently wrong in its forecasts of the effects of austerity. The more beneficial the IMF predicted that austerity would be, the more incorrect its predictions were!

In 2010, the IMF admitted that its demands exacerbated the pain of South Korea’s financial crisis in the 1990s.

And in 2016, the Fund released a report questioning whether its entire economic philosophy had major weaknesses.

The /IMF-EU/deal requires finance ministers to come clean before the end of this year

on what debt relief measures they intend to propose.

Wolfgang Münchau, FT 29 May 2016

Europe's Pointless 'Breakthrough' on Greece

Bloomberg Editorial Board 26 May 2016

The leader of Europe’s finance ministers called Wednesday’s agreement on Greek debt a “major breakthrough.”

In a way, it was. The latest twist in this perpetual negotiation has raised the art of dithering to impressive new heights.

The next financing crunch, which would otherwise have come this summer, has been staved off:

Greece will get money to last it at least until October.

To make this possible and maintain a show of comity, its official creditors have ventured various semi-commitments and vague understandings. But they left basic disagreements -- mainly between Germany and the International Monetary Fund -- unresolved.

This epic of mismanagement is set to drag on.

It has been three years since Greece debt stopped growing

— since then, Athens has borrowed only to service debt payments falling due.

Martin Sandbu, FT Free Lunch 25 May 2016

Domestically, it has been making ends meet for years.

In contrast, the debt burden — the amount of debt in proportion to the economy’s size and hence ability to pay —

has continued to grow. That’s exclusively because of the continuing recession,

itself perpetuated by the debt issue in a vicious cycle.

As the chart below shows, the bulk of the increase in Greece’s debt-to-GDP ratio since the crisis is caused by falling GDP and not mounting debt.

“We on the part of the IMF have made a major concession - we had argued that these debt-relief measures should be approved up front

and we have agreed that they will be approved at the end of the program,” said IMF Director of European Department Poul Thomsen,

Bloomberg 25 May 2016

Some euro-area nations including Germany and the Netherlands, which have elections next year,

had resisted the restructuring measures

as they are restrained by domestic electorates that have grown weary of helping the Greeks.

IMF insists on debt relief, but Germany resists.

Germany trapped in the lie that Greece is solvent,

which is what their own backbenchers were told.

Without that lie, Greece would no longer be a eurozone member.

The IMF and calling Berlin’s bluff over Greece

Wolfgang Münchau, FT 22 May 2016

The International Monetary Fund’s latest recommendations on Greek debt relief have leaked.

FT Alphaville, 20 May 2016

Without any debt relief measures at all, the IMF’s analysis calculates Greece’s debt pile will soar to 294 per cent of GDP in 2060.

Christine Lagarde letter to Eurozone finance ministers demands:

drop all the talk about new austerity measures and quickly agree a plan for debt relief

so that a deal can be met before a possible Greek default in July.

Peter Spiegel, FT Alphaville 6 May 2016

Interndevalvering (Ådals-metoden)

Vice President Biden underscored the need for Europe to follow through on its commitment

to put Greece's debt on a sustainable path through debt relief.

Office of the Vice President, April 04, 2016

The good news is that the recovery continues; we have growth; we are not in a crisis.

The not-so-good news is that the recovery remains too slow, too fragile, and risks to its durability are increasing.

Lecture by Christine Lagarde, Managing Director, IMF

Hosted by the Bundesbank and Goethe University

Frankfurt, Germany, April 5, 2016

Certainly, we have made much progress since the great financial crisis. But because growth has been too low for too long, too many people are simply not feeling it.

This persistent low growth can be self-reinforcing through negative effects on potential output that can be hard to reverse.

The risk of becoming trapped in what I have called a “new mediocre” has increased.

This has consequences for the social and political fabric in many countries, even in Germany where the economy has been strong.

By adopting structural reforms at the same time as slashing spending,

European politicians may be creating an association in voters’ minds between reform and economic hardship

— a reflex that would not bode well for the health of Europe’s economy or for the survival of the euro.

The Economist April 2016

“It’s not a demand of the federal government to have no debt haircut

but rather in our opinion this is legally not possible in the eurozone,”

Merkel said.

Greece faces more than 10 billion euros of debt repayments in June and July

which may strain its finances

Bloomberg 4 April 2016

IMF officials raised questions in a private discussion

published by WikiLeaks about what it would take to get Greece's creditors to agree to debt relief.

CNBC/NYT 3 April 2016

The IMF declined to comment on the WikiLeaks transcript,

but said in a statement that Greece needed to be put ''on a path of sustainable growth''

supported by reforms and further debt relief.

Germany wants IMF-style conditionality imposed on Greece more or less indefinitely.

But both the Greek government and the staff of the IMF dislike this possibility.

The former hates it because it wants a free hand.

The latter hate it because they fear the conditions for successful programmes do not exist.

This being so, they cannot, in good conscience, recommend one to the board.

Martin Wolf, FT 22 December 2015

IMF could now see its involvement when its Greek programme ends in March 2016.

In debt sustainability analysis carried out by body, it has suggested Greece may need a full moratorium on payments for 30 years to finally end its reliance on international rescues.

Telegraph 1 October 2015

The reports came after a former IMF watchdog urged the world's "lender of last resort" to be more critical of its involvement in many bail-out countries for the sake of the institution's credibility.

"Few reports probe more fundamental questions - either about alternative policy strategies or the broader rationale for IMF engagement," said a report from David Goldsbrough, a former deputy director of IMF's Independent Evaluation Office (IEO).

The International Monetary Fund has come under fire for failing in its duty of care towards Greece by pushing self-defeating austerity measures on the battered economy.

Speaking after a six-hour meeting of eurozone finance ministers in Brussels, Christine Lagarde, the IMF managing director, said:

“I remain firmly of the view that Greece’s debt has become unsustainable and that

Greece cannot restore debt sustainability solely through actions on its own.”

FT 14 August 2015

Wolfgang Schäuble, the German finance minister, put a brave face on the lack of a guarantee from the IMF. He said the eurogroup ministers were “assuming” that the fund would decide in October to make “a financial contribution” — something the fund has previously said it would consider.

In an effort to win over the IMF, the finance ministers agreed to consider debt relief at a later date “if necessary”. Such relief would potentially include a longer grace period and longer maturities, although would not involve a nominal reduction in the level of Greek debt. “We stand ready if necessary to consider more debt-related measures,” said Jeroen Dijsselbloem, the president of the eurogroup. “We will have that debate, whether more needs to be done now or later, in October.”

Greece Extend and Pretend

Rolf Englund blog 2015-08-16

IMF: Lagarde Greece

The fund’s managing director hopes its stance on debt relief will be implemented

FT August 13, 2015

Highly Recommended

Eager not to repeat what many see as one of myriad mistakes it and others made in Greece,

IMF staff have for months insisted that the rescue has to include not just a series of difficult reforms by Athens,

but also what in countries such as Germany would be a politically awkward agreement to help reduce the burden of Greece’s more than €300bn sovereign debt pile,

most of which is now owed to other eurozone governments and taxpayers.

Greece could struggle to win German support for its third bailout programme after

IMF confirmed last night that it was not yet prepared to put any cash into the deal.

The Times, August 12 2015

Varoufakis:

"The International Monetary Fund... is throwing up its hands collectively despairing at a programme that is simply founded on unsustainable debt...

and yet this is a programme that everybody is working towards implementing."

He added: "Ask anyone who knows anything about Greece's finances and they will tell you this deal is not going to work,"

BBC 12 August 2015

Debt relief from its European creditors

Talks over an €86bn bail-out for Greece have been thrown into turmoil after just four days as the International Monetary Fund said

it would have no involvement in the country until it receives explicit assurances over debt sustainability.

Telegraph 30 July 2015

An IMF official said the fund would withhold financial support unless it has guarantees Greece can carry out a "comprehensive" set of reforms and will be the beneficiary of debt relief from its European creditors.

"One should not be under the illusion that one side of it can fix the problem."

The delay could last well into next year, forcing the other two-thirds of the Troika - the European Central Bank and European Commission - to bear the full costs of keeping Greece afloat.

Lagarde Push for Greece Debt Relief Challenges Merkel

IMF, which requires borrowers to have sustainable debt, has made clear it won’t ask its 187 other member nations to approve a deal

until euro-area states significantly ease terms on existing loans.

Bloomberg 23 July 2015

Now that Greece is eligible again for loans from the IMF, getting any more money from the fund may hinge on a test of wills between Christine Lagarde and Angela Merkel.

The bailout of as much as 86 billion euros ($95 billion) proposed by European leaders this month assumes financing from the International Monetary Fund and is conditional on Greece seeking a new loan program from the IMF once the current one expires in March. The Washington-based IMF, which requires borrowers to have sustainable debt, has made clear it won’t ask its 187 other member nations to approve a deal until euro-area states significantly ease terms on existing loans.

The most recent example of the IMF’s interventionism with regard to nations and their debts came with last week’s provocatively-timed conclusion that Greece’s sovereign debts were unsustainable.

European creditors such as Germany, the IMF warned, had to accept that, despite their discomfort at the idea,

those debts would have to be restructured for Greece to survive as a member of the eurozone.

FT GLOBAL INSIGHT July 7, 2015

Yet nowhere in that paper was there more than a glancing mention of what at least in the short term remains one significant bit of Greece’s debt burden:

the €22.5bn Athens owes the IMF itself.

IMF admits: we failed to realise the damage austerity would do to Greece

Guardian, 5 June 2015

Greece needs €60bn in new aid, says IMF

Financaial Times 2 Juky 2015

Greece needs more than €60bn in new financial help over the next three years and faces decades under a daunting mountain of debt that will make it vulnerable to future crises, the International Monetary Fund has warned.

In a new analysis that lays out Greece’s economic dilemma in stark terms, the IMF on Thursday called for Europe to grant the country “comprehensive” debt relief, arguing for the doubling of the maturities on its debts from 20 to 40 years.

Greece

The International Monetary Fund’s chief economist, Olivier Blanchard, recently asked a simple and important question:

“How much of an adjustment has to be made by Greece, how much has to be made by its official creditors?”

But that raises two more questions: How much of an adjustment has Greece already made? And have its creditors given anything at all?

James K. Galbraith, the author of The End of Normal, Project Syndicate 16 June 2015

The IMF and Greece’s other creditors have assumed that massive fiscal contraction has only a temporary effect on economic activity, employment, and taxes, and that slashing wages, pensions, and public jobs has a magical effect on growth.

This has proved false. Indeed, Greece’s post-2010 adjustment led to economic disaster – and the IMF’s worst predictive failure ever.

It is Europe, as much as Greece, which is opposing a settlement

IMF in an awkward position, because its doubts on the sustainability of Greece's debts cut two ways.

Either Greece, burdened with massive unemployment, would have to raise taxes and cut public spending further;

or some of its debt would have to be written down.

Bloomberg editorial, 12 June 2015

The compromise capable of resolving this crisis hasn't changed:

a moderation of the fiscal austerity imposed on Greece, a credible commitment from the government in Athens to undertake further long-term reform, and new debt relief.

An outcome lacking any of these components will fail.

It is Europe, as much as Greece, which is opposing a settlement of this kind.

IMF is also frustrated that the European side has been unwilling to address the issue of Greece’s debt pile seriously.

According to the IMF’s calculations, putting the Greek economy on a sustainable path now requires

— at the very least — an extension of the maturities on Greece’s outstanding debts.

But European officials, wary of public opinion, have been reluctant to discuss even that.

FT June 11, 2015

IMF åker hem därför att de är missnöjda med EU?

Rolf Englund blog 11 June 2015

IMF has betrayed its mission in Greece, captive to EMU creditors

The IMF’s Original Sin in Greece was to let Dominique Strauss-Kahn hijack the institution

to save Europe's banks and the euro when the crisis erupted, dooming Greece to disaster.

Ambrose Evans-Pritchard, 5 June 2015

The International Monetary Fund is in very serious trouble.

Events have reached a point in Greece where the Fund's own credibility and long-term survival are at stake.

Syriza’s leaders are letting it be known that they are so angry, and so driven by a sense of injustice, that they may indeed default to the IMF on June 30 and in doing so place the institution in the invidious position of explaining to its 188 member countries why it has lost their money so carelessly, and why it has made such a colossal hash of its affairs.

The Greeks accuse the IMF of colluding in an EMU-imposed austerity regime that breaches the Fund’s own rules and is in open contradiction with five years of analysis by its own excellent research department and chief economist, Olivier Blanchard.

Greece’s public debt is 180pc of GDP. The loans are in a currency that the country does not control. It is therefore foreign currency debt.

The Fund’s mission is to save countries, not currencies or banks, and it certainly should not be doing dirty work for a rich currency union that is fully capable of sorting out its own affairs, but refuses to do so for political reasons.

Är IMFs Lagarde för EU-lydig?

Rolf Englund blog tidigare på dagen 5 juni 2015

The IMF remains sceptical about Greece’s ability to meet the ambitious budget surplus targets

and continues to seek assurances that eurozone governments would agree to restructure Greek debt

— mostly now held by EU creditors — if a credible reform programme is not implemented.

FT 2 June 2015

However, the IMF relented after Christine Lagarde, the fund’s chief, and leaders of Greece’s two other bailout monitors

— the commission and the European Central Bank — were summoned to Berlin on Monday night by Angela Merkel, the German chancellor, to find common ground.

“[There was] at least a meeting of the texts; minds are probably further apart,” said one senior eurozone official.

Rather than call upon the combined authority of Euro governance to manage a deep Euro Area-wide sovereign debt workout,

the IMF, through its repeated public assertion of need for primary surplus numbers in that ballpark,

backs the application of Euro Area political authority to condemn a single member—Greece—to further depression,

thereby also prolonging and aggravating the vulnerabilities for the Euro Area as a whole.

Former IMF staffer Peter Doyle, FT Alphaville 17 April 2015

Voters in Europe are rising up against all this. They do not leave much time for an alternative course to be charted.

The euro is engaged in two dances of death.

The fact that both /ECB and Greece/ threaten euro destruction is testament to the astonishing mis-construction of the euro itself.

Peter Doyle, an economist and former IMF staffer, FT 10 February 2015

A senior International Monetary Fund economist is resigning from the Fund, writing a scathing letter to the board blaming management

for suppressing staff warnings about the financial crisis and a pro-European bias that he says has exacerbated the euro-zone debt crisis.

“The failure of the fund to issue [warnings] is a failing of the first order, even if such warnings may not have been heeded,”

Peter Doyle said in a letter dated June 18 and copied to senior management.

WSJ 20 July 2012

An amazing mea culpa from the IMF’s chief economist

the fund blew its forecasts for Greece and other European economies because it did not fully understand

how government austerity efforts would undermine economic growth.

Washington Post January 3, 2013

The nickname for the IMF in the markets is “It’s mostly fiscal”

Why do the IMF and the other lenders persevere with this destructive path?

The answer is IMP: “It’s mostly political.” That is to say, it is driven by the overriding will to keep the euro on the road.

Roger Bootle, 1 March 2015

But there was a difference. In most cases, the traditional IMF medicine counter-balances fiscal tightening with a devaluation of the exchange rate.

The idea is that as the fiscal tightening squeezes domestic demand and threatens to cause higher unemployment, then a more competitive currency encourages net exports.

Essentially, exports fill the hole left by the retreating government

But this was not possible in the Greek case because the country does not have its own currency – because it joined the euro.

The only way of compensating for this absence was to allow domestic deflation of prices to produce an “internal devaluation”.

What a laugh! We learned in the 1930s that this does not work.

Deflation is extremely slow and painful and, even if it succeeded in improving competitiveness, it would worsen the debt ratio

because it reduces the money value of GDP (the denominator of the ratio).

The result is that Greece is on the road to misery, with no obvious escape.

Why don’t the Germans understand the logic of this argument?

Rolf Englund: The Germans should remember that Brüning was the finance minister who tried fiscal tightening in the 30s and paved the way for Hitler.

Encyclopedia Britannica Online: Brüning's austerity measures prevented any renewal of

inflation, but they also paralyzed the German economy and resulted in

skyrocketing unemployment and a drastic fall in German workers'

standard of living.

He helped President Paul von Hindenburg

win reelection in the spring of 1932, but on May 30 of that year

Brüning resigned, a victim of intrigues by General Kurt von

Schleicher and others around Hindenburg.

The immediate cause of his dismissal was his project to partition

several bankrupt East Elbian estates.

Hindenburg, himself an eastern

landowner, considered this plan Bolshevism, and his withdrawal of

confidence left Brüning with no choice but to resign.

Read more here

Members of a European Parliament committee investigating the role of the troika

call to replace this “interim” institution by a “more democratically accountable and transparent” inspection process

“We need more transparency, more democratic legitimacy,” Othmar Karas, the conservative Austrian MEP leading the inquiry.

“All instruments of the EU must be based on community law,” he added.

His colleague, the French Socialist MEP Liem Hoang Ngoc, was more categorical, declaring that there was “no legal basis for the actions of the troika.”

Eurointelligence 31 January 2014

IMF boss Christine Lagarde calls for speedy EU bank union

How banking union will be achieved is unclear, with some countries maintaining it would require a change to EU treaties.

BBC, 10 September 2013

The banking union project is designed to prevent a repeat of the global banking crisis. It could include a single banking supervisor, and pool national resources to rescue banks.

While the language of the IMF report is polite,

it masks a bitter dispute between the Fund and Germany over the nature of the EMU malaise,

and whether austerity and reform really have cleared the way for a viable recovery.

Ambrose, 6 Aug 2013

The IMF admitted in its famous mea culpa earlier this year that the Troika bail-outs had been scandalously botched, that the growth forecasts had been delusional, that loans been disbursed (the biggest in IMF history as the share of any country’s quota), in violation of three of the IMF’s four key guidelines on rescue packages, and that the whole policy was designed to save the euro, not to save Greece.

In other words, they admitted that the Fund had allowed itself to be hijacked by European politicians, for the benefit of the European Project.

Yet having bravely come clean, they are still playing along with this game.

Ambrose Evans-Pritchard, August 1st, 2013

Brazil supports Greece aid programme after all

Brazil’s finance minister Guido Mantega phoned Christine Lagarde expressing his support for the Greek aid programme,

saying that its representative at the IMF Nogueira Batista had not consulted his government before the vote

and was not authorised to withhold support for the latest aid to Athens, according to the FT.

Eurointelligence, August 2, 2013

In Brazil Mantega’s rush to support the IMF’s decision is met with some disbelief, as Mantega used to be one of the starkest critics of the IMF. One analyst says it is a sign of his own political weakness. Batista had released a second, shorter statement on Wednesday, in what some saw as an attempt to mollify the public reaction to his first, in which he said although he represented other countries in the region, his decision to abstain from the latest vote on Greek aid should not be attributed to them.

Lagarde confident that Europeans stand behind their commitment to Greece

Christine Lagarde said she is confident about Europe's commitment to provide additional measures to help Greece reach the agreed debt thresholds

if Greece delivers on its commitments.

"I have no reasons to believe the Europeans would not themselves deliver on their undertaking vis-à-vis Greece," she told reporters on Thursday.

"What form those further measures and assistance will take will certainly be discussed at a later stage."

Eurointelligence, August 2, 2013

Elva latinamerikanska länder, med Brasilien i täten, sågar IMF:s fortsatta stöd till det konkursmässiga eurolandet Grekland.

Lånevillkoren uppfylls inte, anser ländernas regeringar, som avstod från att rösta när den senaste utbetalningen av grekiska nödlån godkändes.

Dagens Industri, 31 juli 2013

"Implementeringen av Greklands reformprogram har varit otillräckligt på nästan alla områden", säger Paulo Nogueira Batista, Brasiliens represenant i IMF:s styrelse.

Han beskriver utsikterna för både tillväxt och skulder som ohållbara för Grekland.

IMF godkände trots invändningarna en ny omgång nödlån på 1,7 miljarder euro i måndags, vilket innebär att Grekland sedan 2010 fått 28,4 miljarder euro i nödlån från fonden.

Is Germany Repeating American Errors at Bretton Woods?

U.S. set out to revive a fixed exchange-rate system by offering a war-torn, debt-ridden world

a new deal to be supported by concessionary dollar loans from a new IMF.

Today, Germany is trying to resuscitate /återuppväcka/ the periphery of the crisis-stricken euro area

in much the same way, and it is worth looking back at the formation of Bretton Woods for clues as to how this will play out.

Bloomberg, July 16, 2013

The architect of the conference, Harry Dexter White of the U.S. Treasury Department, gave the American delegates a warning: the other countries would want the IMF to prod the U.S. “to adopt a policy which will put less pressure on their exchange and enable them to sell more goods here.”

The U.S. wouldn’t tolerate such interference. “We have been perfectly adamant on that point,” White said. “We have taken the position of absolutely no on that.”

The reason, White explained, was that the IMF was “designed for a special purpose, and that purpose is to prevent competitive depreciation of currencies.”

Fixed exchange rates should therefore be at the center of the postwar monetary architecture, to stop countries devaluing their way out of trade deficits. The IMF should only lend money for short periods to countries that had difficulty financing deficits.

Why was the U.S. in a position to impose such a system? Because it controlled almost 80 percent of the world’s monetary gold stock at the time.

Gold in Fort Knox, White explained, was “why we dominate practically the financial world, because we have the where-with-all to buy any currency we want.”

Today, Germany is persisting with the same creditor-centric plan for reviving the euro area -- new loans to finance old loans while the debtors cut spending and wages to accommodate fixed exchange rates.

Lippmann, if he were alive, would no doubt warn that the seemingly endless austerity being imposed on southern Europe will ultimately lead to a political backlash that will make it unsustainable.

Germany will soon have to choose: a Marshall Plan for the south, or an economic and political breakdown of the euro zone.

(Benn Steil is director of international economics at the Council on Foreign Relations and

author of “The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order.”)

The most honest and clear-headed analysis by an official body on the eurozone crisis yet.

In just 50 pages, the IMF produced a concise and sober analysis of what went wrong in the Greek rescue programme.

The fundamental error was excessive optimism about economic growth.

Moreover, it was not an error of bad luck.

The severe economic consequences of the agreed Greek adjustment were not merely visible;

they were actually foreseen by many critics, as the IMF openly admits.

Wolfgang Münchau, FT, June 9, 2013

My own expectation is that Greece will remain stuck in a vicious circle of recession and debt deflation

until it either leaves the eurozone and defaults unilaterally or there is a fundamental shift in policy.

The latter would require two adjustments to the existing programme.

The first would be a redefinition of debt sustainability.

The target of 124 per cent of GDP is both arbitrary and illusionary.

It is arbitrary because there is no economic reason for this number.

It is illusionary because investors no longer regard Greek debt as sovereign, but as sub-sovereign.

Sub-sovereign entities, such as US states or German Länder, cannot sustain the same debt-to-GDP ratios as sovereign countries

because they lack the ability to print their own money.

A figure in the range of 60-80 per cent would be more realistic.

If you thought that the IMF’s Mea Culpa on Greece has any practical significance, you could not be more wrong.

The strategy for Greece – if you want to call it that – will continue. As for the historic assessment,

IMF mission chief for Greece Poul Thomsen had this to say:

"If we were in the same situation, with the same information at that time, we would probably do the same again."

Not only is he not sorry, he would do it all over.

Eurointelligence 7 juni 2013

Streit über Griechenland-Hilfe: Das falsche Spiel des IWF

Der Spiegel, 6th of June 2013

ABBA: I should do the same again

There was something in the air that night The stars were bright, fernando They were shining there for you and me For liberty, fernando

Though I never thought that we could lose There's no regret If I had to do the same again I would, my friend, fernando

The International Monetary Fund has published a scathing report about how it and the European Union handled Greece’s first €110bn bailout,

saying growth assumptions were too optimistic and that debt restructuring should have occurred earlier.

Financial Times June 6 2013

The study says that the rescue went ahead even though Greece did not meet one of the IMF’s four criteria for such a huge programme – a good chance of debt sustainability in the medium term – and may have failed two of the others as well.

IMF admits mistakes on Greece bailout

BBC

The bailout of Greece was bungled because it was an attempt to save the single currency

rather than the debt-stricken country, according to a highly critical IMF report.

Telegraph 6 June 2013

The IMF has released a fairly remarkable piece of self-criticism over policy in Greece.

On a first read, the report seems to suggest two main failings on the IMF’s part:

it failed to acknowledge early on that Greece simply could not repay its debt in full,

and it vastly underestimated the economic damage austerity would inflict.

Paul Krugman, June 5, 2013

For Hard-Hit Greeks, IMF Mea Culpa Comes Too Late

Greeks reacted with an air of vindication and outrage at the IMF's admission it erred in its handling of the country's bailout,

berating an apology that comes too late to salvage an economy and countless lives in ruins.

CNBC 6 Jun 2013

Anger was palpable on the streets of Athens, where the European Union-IMF austerity recipe that the Washington-based fund says it sharply misjudged has left rows of shuttered stores and many scrounging for scraps of food in trash cans.

"Really? Thanks for letting us know but we can't forgive you," said Apostolos Trikalinos, a 59-year old garbage collector and a father of two.

Nobody has taken responsibility for the disastrous errors made by the EU-IMF Troika in Greece, where youth unemployment has just reached 58.3pc.

Nobody has resigned, or missed a day’s pay, or faced any kind of censure from an elected body,

despite the withering indictment just issued by the IMF.

Worse yet, the basic conceptual policy errors that led to this tragic episode have not been fully corrected.

With a little trimming here and there, the eurozone is sticking to the same mix of self-defeating contractionary policies

Ambrose Evans-Pritchard Economics Last updated: June 6th, 2013

European Commission denies IMF Greece 'mistakes' claim

BBC

The EU's bailout of Cyprus has elicited unusually frank and vehement criticism from the finance experts grouped in the IMF's Executive Board.

Although no names were mentioned, the criticism was directed at all European politicians involved in the bailout,

from Merkel and Schäuble to Hollande, Barroso and Olli Rehn.

The criticism applies in particular to the Eurogroup president, Dutch politician Jeroen Dijsselbloem, who has even recommended the Cyprus bailout as a model for future bailout programs.

Der Spiegel, 3 June 2013

Prior to the financial and euro crisis, it was usually the West that faulted the developing nations and emerging economies for incurring excessive debt and constantly begging for money from the IMF.

The situation is reversed today. The former petitioners now find themselves having to fend off constant requests for assistance from Europe. And they note with growing indignation how promises are being broken in Paris, Brussels and Berlin, figures are being massaged and many of the principles that the West once established for the IMF's activities are being violated.

French and German banks reduced their exposures to these markets by some 30-40 percent

ECB has taken extraordinary action to protect monetary union with the LTRO and conditional OMT.

Unfortunately, fragmentation continues and remains debilitating.

A common safety net is another essential element.

This would involve common deposit insurance and common backstop.

The other union Europe needs to contemplate is fiscal union.

David Lipton, First Deputy Managing Director IMF, April 25, 2013

I have been asked to speak today to the topic of “Saving the Euro.”

On reflection, that topic might have been more suitable a year ago,

before the euro area governments and institutions took important steps that gave us

some distance from that worst-case scenario.

The reality is that Europe still faces severe vulnerabilities that — if unaddressed — could degenerate into a stagnation scenario.

There is a deep ongoing recession in some periphery countries and weakness in the core.

Investment is declining, and unemployment continues to rise. Financial markets remain fragmented, undermining the transmission of monetary policy.

This contributes to divergence in private interest rates, and reduces access to credit, particularly for smaller enterprises.

Reform fatigue is setting in.

In our preoccupation with sovereign debt, we tend to overlook the huge overhang of private debt in some countries that could be a deadweight on demand and bank balance sheets for a long time.

French and German banks reduced their exposures to these markets by some 30-40 percent between mid-2011 and the third quarter of last year.

ECB has taken extraordinary action to protect monetary union with the LTRO and conditional OMT. Unfortunately, fragmentation continues and remains debilitating.

A common safety net is another essential element. It is needed to weaken bank-sovereign links by reassuring depositors.

This would involve common deposit insurance and common backstop.

The other union Europe needs to contemplate is fiscal union. That will surely take time, and further discussion by members to choose the precise end point.

Treaty change

The last big rewrite took the best part of a decade: the constitutional treaty was rejected by French and Dutch voters in 2005,

and its successor, the Lisbon treaty, had to be put to the Irish twice before passing.

Today, even assuming that Europe’s debtors and creditors can agree, any revision could invite disaster.

Much of the euro zone is in a deep and prolonged recession,

and Eurosceptic parties of many stripes are on the rise in both north and south.

Charlemagne, The Economist print Apr 27th 2013

In its twice-yearly World Economic Outlook, IMF said the euro zone remains the weakest part of the global economy,

and warned that a long period of low growth in the currency area would weaken the potential for expansion in the neighboring economies

"The damage and the spillovers could be much worse if pessimism builds on pessimism and leads to a major cutoff of credit to periphery sovereigns

or if stagnation raises doubts about the viability of the EMU," the Fund said.

Wall Street Journal 16 April 2013

IMF said that in the near-term, the euro zone still poses the greatest threat to a recovery in the global economy, citing "the fallout from events in Cyprus" and political stalemate in Italy, as well as "vulnerabilities" among the weaker members of the currency area.

The Fund warned that the prospect of a long period without significant economic growth could spook investors, leading to a renewed threat to bond market access for governments in southern Europe.

World Economic Outlook, Hopes, Realities, and Risks, April 2013

Top of pageProtecting the eurozone at all costs is undermining IMF’s validity

In the period from its inception in 1946 up until the financial crisis, the IMF broadly succeeded in its task of promoting financial stability and monetary co-operation.

So much so, in fact, that by 2007 many had begun seriously to question the organisation’s continued purpose.

Was there really any need to keep all those highly paid economists in Washington DC,

when the capital markets were doing such an apparently splendid job in guaranteeing financial and economic stability?

Jeremy Warner, Telegraph 15 April 2013

With the advent of the credit crunch, the IMF briefly rediscovered its raison d’etre.

Momentarily distracted from carnal pursuits, the IMF’s erstwhile managing director, Dominique Strauss-Kahn, set about galvanising an international response which was not without its early successes.

Here was a global implosion for which the organisation seemed to have been tailor made.

In becoming part of the hated “troika” which imposes apparently counter-productive austerity on weaker members of the euro, the IMF has badly discredited itself and by doing so is steadily undermining its validity on the wider international stage.

The IMF’s starting point is that the euro is too systemically important to be allowed to break up. Like the larger banks, it has become too big to fail, and must therefore be propped up for fear of the wider economic damage if it went down in flames.

So along with the European Commission and the European Central Bank, it has become part of the hated “troika”, imposing fiscal austerity and structural reform on weaker eurozone nations in return for handouts

Full textLagarde:

Väljarna största hotet mot EMU

Den största risken kring försöken att lösa krisen i eurozonen är en ökad politisk utmattning och

väljare som blir trötta på krävande ekonomiska omstruktureringar.

Dagens Industri 10 april 2013

The IMF was formed in 1944 to avert another Great Depression by lending money to troubled countries,

but after decades of dealing mainly with the third world, the

IMF now devotes 83% of the money in its general-resources account - extended loans, in plain speak - to three limping European nations: Portugal, Greece and Ireland.

Time Magazine, April 8, 2013

Some economists even seem nostalgic for the days of Lagarde's predecessor, Dominique Strauss-Kahn, who resigned in disgrace after he was hauled into a New York City jail in May 2011 on charges of sexually assaulting a hotel maid. (The charges were eventually dropped.)

It was Strauss-Kahn who negotiated the IMF loans to Greece, Ireland and Portugal, using his credibility as an economist and his skill as a dealmaker to keep dissension in check.

At a conference of German bankers in Frankfurt on March 19, she /Lagarde/ zeroed in on one message: Europe needs a strict, E.U.-wide banking union, and quickly.

“substantially below” 110 per cent in 2022

Several of the elements remain unfinished, including a Greek debt buyback programme

Christine Lagarde, the International Monetary Fund chief, said her institution would not release its portion of the Greek bailout until the transaction was successfully completed.

Financial Times, 27 November 2012

The IMF had been holding out for a deal to get Greece’s debt levels to 120 per cent of gross domestic product by 2020, a target that would have likely forced eurozone governments to make substantial writedowns on their bailout loans – something deemed politically explosive in creditor countries like Germany and the Netherlands.

In exchange for allowing a loosening in the target to 124 per cent, Ms Lagarde secured a commitment to get debt levels to “substantially below” 110 per cent in 2022

Euro-zone finance ministers meeting in Brussels this week have been unable to reach an agreement with IMF

on how to ensure that Greece's debt load comes down to manageable levels.

Germany and other European countries continue to reject a new debt haircut.

The standoff could become dangerous.

Der Spiegel, 21 November 2012

On Greece, Europe should listen to the IMF

Mohamed El-Erian, Financial Times, November 21, 2012

"You know, it's not over until the fat lady sings, as the saying goes," Ms Lagarde told reporters

when asked if she expected a deal to be forged at the meeting next week in Brussels.

Telegraph 16 November 2012

EuroCliff

Det budgetstup som alla; Tyskland, EU, Internationella Valutafonden IMF och andra ekonomiska pekpinneviftare är överens om att USA måste undvika till varje pris,

är precis det som flera av Europas länder redan knuffats ut över.

Den kur som sägs ta kål på USA påstås alltså kunna rädda Europa.

Andreas Cervenka, SvD Näringsliv 14 November 2012

Några exempel. Spaniens budgetunderskott skulle enligt order från övriga EU-länder minskas från 6,3 procent av BNP i år till 2,8 procent 2014.

I Portugal ska budgeten kapas med motsvarande över 3 procent av BNP bara under 2013 och i Grekland är besparingarna 7 procent av BNP under 2013 och 2014 varav det mesta ska tas nästa år.

Detta trots att budgetunderskotten alltså är större i USA.

Bland de som varit med och ställt upp dessa krav finns bland andra IMF.

Läs mer här

Jean-Claude Juncker, president of the Eurogroup of finance ministers, announced Greece would be given an extra two years to meet its debt reduction target of 120pc of GDP by 2022 instead of 2020.

“The target, as far as the time-frame is concerned, has been postponed to 2022,” he said.

A visibly angered Mrs Lagarde, the managing director of the IMF, shook her head and rolled her eyes at the announcement that breaches the Washington-based fund’s condition that Greek debt must become sustainable by 2020.

“We clearly have different views,” she said. “In our view the appropriate target is 120pc by 2020. It is critical that the Greek debt be sustainable."

Financial Times via CNBC och Rolf Englund blog 12 November 2012

IMF wants Greece's creditors to forgive a portion of the country's debt,

a move which could cost Germany up to 17.5 billion euros.

It is partly for that reason that euro-zone finance ministers are in favor of extending by two years

the deadline for Greece to reduce its debt load to 120 percent of GDP from 2020 to 2022.

Der Spiegel, 14 November 2012

IMF's mea culpa is the "biggest financial story of the year"

Ambrose Evans-Pritchard, 14 Oct 2012

IMF

It is no secret why growth is slowing in high-income countries:

this is due to fiscal tightening, weak financial systems and powerful uncertainty.

This toxic combination is particularly threatening inside the eurozone, where, again no surprise,

countries reliant on exports are affected by the shrinking economies of big trading partners

Martin Wolf, Financial Times, 16 October 2012

In its relations with its most powerful clients, the International Monetary Fund possesses “the right to be consulted, the right to encourage and the right to warn”. Walter Bagehot, the great Victorian economic journalist, gave this description of the role of the British monarch in the 19th century.

I applied this phrase to the role of the fund in a paper I submitted to its 2011 triennial surveillance review.

At the annual meetings in Tokyo, the fund fulfilled precisely this role. What matters, however, is that its members, above all, the US and Germany, act upon the warnings and encouragement they have received.

Armageddon i Grekland den 18-19 Oktober:

How much more pain can the people take?

BBC via Rolf Englund blog

We face a conjunction of three large events - the implosion of the debt-based finance-capitalism that developed over the past twenty years or so, a fracturing of the euro resulting from fatal faults in its design, and the ongoing shift of economic power from the west to the fast-developing countries of the east and south.

Keynes condemned Britain's return in 1925 to the gold standard, which famously he described as a barbarous relic.

Would he not also condemn the determination of European governments to save the euro?

Might he not think they would be better advised to begin a planned dismantlement of this primitive relic of 20th Century utopian thinking?

John Gray, BBC, 21 July 2012

Ingen eurokris i Almedalen?

Regeringen, med stöd av socialdemokraterna, förefaller ha som princip att i Bryssel uppträda som om Sverige vore medlem av eurozonen. Sverige har således utlovat uppemot miljarder kr till IMF avsedda för stöd till euroländer i kris.

Vi borde i stället följa den linje som England driver.

Lars Wohlin och Rolf Englund, 10 juli 2012

Mr Cameron said: "I can understand why eurozone countries may want to look at elements of banking union.

"Because we are not in the single currency, we won't take part in the profound elements of that banking union.

"I wouldn't ask British taxpayers to stand behind the Greek or Spanish deposits.

"It is not our currency, so that would be inappropriate to do.

The Independent 7 June 2012

Sverige är inledningsvis berett att ställa upp med 10 miljarder dollar, nära 70 miljarder kronor, till IMF,

säger finansminister Anders Borg enligt Reuters.

Maximalt kommer Sverige att bidra med 100 miljarder kronor.

DN/TT 17 april 2012

IMF still won't admit truth about the euro

Discussion will once again focus on the creation of a firewall big enough to provide for bigger eurozone bailouts, including Spain and possibly Italy, too. This misses the point, for it presupposes that the crisis is at heart just a confidence issue that can be solved simply by creating a backstop large enough to convince markets they cannot break the euro.

Jeremy Warner, Telegraph 16 April 2012

In fact, the underlying cause of the Europe's travails is much more fundamental – it is the euro itself, which is ripping the Continent apart in an uncorrected balance of payments and consequent debt crisis. European leaders have yet properly to face up to this inconvenient truth. Their project won't and cannot work in its present guise.

The US, knowing it could never get enhanced IMF support through Congress, has already said it won't contribute any additional funding, while even the UK is beginning to get cold feet. A previously compliant George Osborne does not believe the conditions he listed a little while back, not least a much bigger European rescue fund, have been met.

Despite the punishing mix of austerity and structural reform being imposed on the South, the idea that Europe's periphery can in time be made as competitive as Germany is just fantasy.

Europe can’t accept that the economics of the single currency condemn it to failure

Det skriver Jeremy Warner i Daily Telegraph 12 April 2012

Felet är att eurozonens ledare inte vill inse att allt var fel från början.

Rolf Englund blog

The survival of the eurozone now depends on Italy and Spain.

They are the countries that are too big to fail – or to rescue.

Structural steps are painful for any government. They are devilishly difficult without growth.

Robert Zoellick, president of the World Bank, Financial Times 16 April 2012

Is the IMF already assuming Greek failure?

FT, Peter Spiegel, 19 March 2012

On Friday, after much of Europe shut down for the week, the International Monetary Fund issued its 231-page report on Greece’s new €174bn bailout

The fund notes that more austerity measures totalling 5.5 per cent of economic output – or about €12bn – must be found in the next three months to close gaps in Greece’s budget for next year and 2014. Without those cuts, the IMF warns, it’s ready to withhold its very first quarterly aid payment in three months’ time

The report also makes clear that if Greece falls off the wagon in any way, the IMF is not going to pick up the tab any more. Instead, it will either be up to Athens to restructure its debt yet again or for eurozone lenders to put up even more money.

The report seems to give a very strong hint that the fund wants European Union leaders to prepare for that eventuality very quickly.

U.S. Treasury Secretary Timothy Geithner:

Europe's actions so far have averted potential financial catastrophe

but said it still must put up a sturdier firewall against contagion.

CNBC 26/2 2012

"A durable solution requires both a sustained period of economic reform and a substantial financial firewall to support those reforms," he told a press conference at the conclusion of a Group of 20 finance ministers' and central bankers' meeting.

Injecting Cash - Europe's Banks Are Addicted to ECB's Cheap Money

ECB will give European banks another massive round of loans at bargain-basement rates on Tuesday,

with financial institutions expected to borrow up to one trillion euros at 1.0 percent.

Der Spiegel 27/2 2012

G20-länderna kommer inte att skjuta till mer pengar förrän eurozonen själv gjort mer

Euroländerna håller på att bygga upp en ny räddningsfond som ska innehålla 500 miljarder euro.

Det är alldeles för lite, hävdar länderna utanför Europa, brandväggen måste byggas högre

Ekot 27 februari 2012

Det är framför allt Tyskland som hittills vägrat att sätta in mer pengar i eurozonens räddningsfond. Även i går framhärdade den tyske finansministern med att det inte behövs. Han tycktes dock lämna en liten öppning för att Tyskland skulle kunna ändra sig innan nästa G20-möte i april.

Schäuble’s duplicity on ESM enlargement: He says Yes in private, No in public

Eurointelligence Daily Briefing 27/2 2012

This is how Wolfgang Schäuble has been running the eurozone crisis all along. He proceeds with conflicting messages.

The German public seems under the impression that Angela Merkel’s rejection of an increase in the ESM would hold, but there are already signs that the German resistance to an enlarged ESM is weakening. T

The dangerous subversion of Germany's democracy

Markets appear to be acting on the firm belief that Germany’s finance minister Wolfgang Schäuble is lying to lawmakers

Ambrose Evans-Pritchard, September 28th, 2011

Very Important Article

Germany Isolated over Resistance to Expanding Euro Bailout

Der Spiegel, 23 februari 2012

The European Commission, the European Union's executive in Brussels, is also arguing for an expansion of the ESM. "There is a clear need to further strengthen the euro area financial firewalls in order to equip Europe to contain the contagion and counter speculative pressures," Currency and Monetary Affairs Commissioner Olli Rehn said on Thursday.

Both the International Monetary Fund (IMF) and the Netherlands have increased pressure for the EFSF money to be carried over into the new fund -- a particular blow for Germany given that the Dutch have been among the most conservative of the euro-zone member states when it comes to providing bailout funds for Greece. Finland, another critic of Greek aid, has also signalled its support according to media reports.

*

Germany's ruling parties are to introduce a resolution in parliament blocking any further boost to the EU’s bail-out machinery,

vastly complicating Greece’s rescue package and risking a major clash with the International Monetary Fund.

Ambrose Evans-Pritchard, and Louise Armitstead 23 Feb 2012

G20 must protect the IMF from Europe

At this weekend’s G20 meeting European countries are likely to

press for an increase in the IMF’s resources as a means to bolster the firewalls

Mohamed El-Erian, Financial Times February 24, 2012

At this weekend’s G20 meeting, European countries are likely to press for an increase in the International Monetary Fund’s resources as a means to bolster the firewalls against the eurozone debt crisis. The other G20 members must resist such pressure until Europe starts showing more signs that it’s getting its act together.

It should come as no surprise that over the last couple of years Europe has pressed the IMF very hard to make exception after exception - and it has succeeded. This has resulted in a number of firsts by an organisation that prided itself on the “uniformity of treatment” for member countries.

Preserve and Protect

Each president recites the following oath, in accordance with Article II, Section I of the U.S. Constitution:

"I do solemnly swear (or affirm) that I will faithfully execute the office of President of the United States,

and will to the best of my ability, preserve, protect and defend the Constitution of the United States."

Germany has said that it sees no need to increase the size of Europe's

permanent bailout fund, the European Stability Mechanism (ESM):

Daily Telegraph 22 February, 11:32

Spokesman Steffen Seibert told reporters:

The German government's position has not changed -- that means no, it is not necessary... more

Lagarde repeated her calls for an increase in the size of the permanent euro backstop fund,

the European Stability Mechanism (ESM), which is due to come into operation in mid-2012,

as a precondition for a significant contribution by the fund

Der Spiegel, 21 February 2012

The IMF had provided 30 percent of the first €110 billion bailout for Greece, agreed upon in May 2010, but reportedly wants to reduce the size of its contribution this time around.

IMF is considering contributing just 13 billion euro to the latest Greek bailout package

10 percent of the 130 billion euro second bailout package under consideration for Greece.

The IMF funded 30 billion euro of the first Greek bailout, about 27 percent of its 110 billion euro

Globalpost 17 Febr 2012

IMF

ska få en resursförstärkning. Euroländerna liksom Sverige är beredda att bidra. Men på andra håll har intresset att ställa upp hittills varit svalt.

Johan Schück, DN Ekonomi 3 februari 2012

The IMF is no longer serving its purpose

To save the eurozone, the International Monetary Fund needs to dispense tough love, not endless bail-outs.

Jeremy Warner, Daily Telegraph, 19 Jan 2012

The IMF’s purpose is to instill the “right” economic policies in countries so that they can become competitive, and when things go awry, to provide the stop-gap finance and policies that get them back on their feet.

In addressing the European debt crisis, it has veered dangerously from this mission. Support seems directed more at sustaining the single currency than helping individual nations out of their difficulties. This is leading to the now routine prescription of inappropriate policy – repeated rounds of fiscal austerity with none of the compensating support of monetary stimulus and devaluation that countries such as Britain, with their own sovereign currencies, have been able to apply. The IMF has thereby become complicit in making a bad situation much worse.

In a recent analysis of developments in Greece, the IMF virtually admitted as much, describing with eloquence how fiscal austerity had become self-defeating by undermining all hope of economic growth.

Yet in defiance of its own evidence, the organisation concluded that the programme remained on track.

Euroländernas genidrag att deponera 200 miljarder euro i IMFs kassaskåp för att kunna begära nödlån ur det,

istället för att skramla ihop internt och då riskera långa parlamentsdebatter och medborgarilska,

ser ut att vara lättare sagt än gjort.

Teresa Küchler, SvD Näringsliv, 23 december 2011

Med IMF-lösningen tänkte man också ta sig runt politiska och lagtekniska hinder i länder som Tyskland, vars författningsdomstol gjort klart att det nu öppet betalningströtta parlamentet i Berlin måste ge klartecken till varje nytt lån.

Den brittiske premiärministern David Cameron sade i parlamentet i London att IMF var till för att rädda länder, och inte valutor.

Den tyska regeringen, som enligt måndagsmötets slutprotokoll gick med på att bidra med hela 41,5 miljarder till IMF, måste få Bundesdagens godkännande, vilket kan bli svårt.

Why should the members of the IMF finance Italy when German savers pull out and the German government

does not want the ECB to come to the rescue of a fellow member of the common currency area?

The US administration has already ruled out any American contribution because it would not pass Congress.

Daniel Gros, director of the Centre for European Policy Studies, 22.12 2011

This leaves the emerging markets as the only remaining source of funds. They, meaning China

I senaste numret av Nyliberalen skriver jag om ekonomerna som förutspådde eurokrisen.

Och då menar jag inte alla de ekonomer som rent allmänt trodde att det skulle gå åt h-e, utan de som faktiskt förutspådde hur det skulle gå åt h-e.

Italien har lovat att låna ut 22,5 miljarder euro till IMF så att IMF ska kunna rädda ... Italien.

Och Spanien bidrar med 15 miljarder euro för att rädda ... Spanien.

Mattias Lundbäck, 19 December 2011

"at least €1 trillion is necessary to stabilize the euro"

European leaders last week agreed to outfit the International Monetary Fund with 200 billion euros

But Germany's central bank has its doubts:

Some heavyweight countries are balking, and it also increases risks for German taxpayers.

Der Spiegel, 16 december 2011

The agreement on the €200 billion IMF fund is essentially an admission that the current euro bailout fund, the European Financial Security Facility (EFSF), is likely not large enough to handle Italy's -- or even Spain's -- refinancing needs should they run into trouble.

Plans are afoot to leverage the EFSF, but the fund's spending power is likely to max out at €750 billion.

The current consensus, voiced most recently by European Central Bank governing council member Klaas Knot, holds however that

at least €1 trillion is necessary to stabilize the euro.

Kommentar av Rolf Englund:

Jag tror att en trillion euros är 1000 miljarder euro.

Om en euro är 9 kr är en trillion euros lika med 9.000 miljarder kronor.

Mycket pengar för ett, misslyckat, experiment.

Ms Lagarde was always the wrong choice as managing director of the IMF, if only because she is neither impartial nor particularly well qualified for the job.

She's a European cuckoo in the nest, and therefore as incapable of seeing what needs to be done as the rest of the eurozone policy elite. Indeed, I've yet to see any evidence that she properly comprehends the economics of the eurozone sovereign debt crisis.

To Ms Lagarde, saving the euro and saving the world economy are one and the same thing. They are not.

Jeremy Warner, December 16th, 2011

Sverige är berett att bidra med upp till 100 miljarder kronor till krishanteringen i EU via IMF.

Ekot 15 december 2011

EU-länderna ska skjuta till 200 miljarder euro till IMF.

Det är nästan 2.000 miljarder kronor.

Det är väl generöst av stater i kris?

Detta är bakgrunden.

Rolf Englund blog 10 december 2011

The long shadow of the 1930s

Could things go bad again?

I mean really bad – Great Depression bad, world war bad?

The kind of cataclysmic event my generation has learned to think belongs only in the history books.

Gideon Rachman, Financial Times, November 28, 2011

If I had to give a snap judgment on the embryonic plan to “save the euro”,

I would say it is deflationary in the short term and inflationary in the long term

If the Republicans do well in the 2012 US elections, the stage will be set for a repetition of

many of the economic errors of the 1930s, when countries tried to fight depression with cuts of all kinds.

Samuel Brittan, 15 December 2011

![]()