Mario Draghi

Related: Europakten - Banks - Funding - Otmar Issing - Tyskland - Frankrike - Stabilitetspakten - Finanskrisen - Euron

The ECB "will continue to monitor the situation while euro-area financial markets in general are going back to normal functioning,''

Mr Trichet said in a statement on Tuesday. 14/8 2007

Targeted long-term refinancing operation - TLTRO

TLTRO is a super-cheap funding vehicle for banks that choose to participate,

getting liquidity into the more challenged parts of the EU’s regional banking system.

Think Greece and Italy.

Bloomberg 21 January 2019

The main instrument of coercion in the eurozone is not its fiscal rules, but the power of the European Central Bank to withdraw funding from national banks.

Italy

The short history of the eurozone has taught us that resistance is futile.

Wolfgang Münchau FT 28 October 2018

The ECB has bought €2.5tn of eurozone debt securities under a QE programme that is set to stop at the end of this year.

The central bank’s monthly purchases halve to €15bn of bonds in October.

FT 4 October 2018

The ECB defines price stability as inflation “below, but close to, 2% over the medium term.”

That is a lower inflation rate than even the Bundesbank achieved during its celebrated pre-euro history,

and it is a tighter target than virtually all other central banks pursue.

For some, too much of a good thing is apparently wonderful.

Stefan Gerlach Project Syndicate 12 July 2018

Stefan Gerlach is Chief Economist at EFG Bank in Zurich and Former Deputy Governor of the Central Bank of Ireland. He has also served as Executive Director and Chief Economist of the Hong Kong Monetary Authority and as Secretary to the Committee on the Global Financial System at the BIS.

Italy illustrates the way to liberal democracy’s demise

Wolfgang Münchau FT 20 May 2018

If liberal democracy fails to deliver economic prosperity for a sufficiently large portion of the population over long periods, it ends — along with the financial and economic institutions it has created.

The euro is run in the interest of whichever country faces the biggest problems and

poses the biggest threat to the survival of monetary union at any particular time.

Right now that is Italy,”

Bernard Connolly, a hedge fund advisor and former currency chief for the European Commission, Ambrose Telegraph 22 February 2018

Germany is the largest guarantor of the European Central Bank’s credit default insurance, known as the OMT,

and provides by far the largest stock of “target” overdraft credit to other European countries, currently €956bn.

Hans-Werner Sinn FT 27 June 2018

Until Greece can successfully sell a multi-billion euro bond to international investors,

it can’t truly be said to be on a sustainable path.

For now, the European Union, the International Monetary Fund and European Central Bank have chosen to extend and pretend.

Greece - Extend and Pretend, again

An agreement was close that would leave Greece with minimal repayments

until after 2030 on the €228bn it owes to the rest of the eurozone.

FT 21 June 2018

For three years, the ECB has allowed investors to overlook the fragilities in the public finances of several member states and the flaws in the monetary union.

Governments must now learn to do without the central bank’s support.

Bloomberg Editorial 15 June 2018

What fixes does the euro really need?

As Isabel Schnabel and Nicolas Véron have recently explained, this requires, at a minimum,

that banks’ creditworthiness is no longer at the mercy of the public finances in the country they happen to emerge from —

that the “doom loop” between banks and sovereigns be broken.

Martin Sandbu 11 June 2018

Mario Draghi, the euro’s central banker, inimitably set out what this means in his speech in Florence last month;

the single best guide to the eurozone’s challenges.

The head of Germany’s central bank Jens Weidmann, who is seen as a leading candidate to become the next president of the ECB,

has taken aim at plans for creating new eurozone funds to help crisis-hit countries, urging governments to instead make greater efforts to put their finances in order.

FT 5 June 2018

How to Unite 340 Million People: The ECB Turns 20

Highlights from the first two decades of a monetary union.

Bloomberg News 1 juni 2018

Italy no longer has a lender of last resort standing behind its sovereign debt,

and therefore has no backstop defence for its commercial banking system.

Ambrose Evans-Pritchard 30 May 2018

The European Central Bank is progressively removing its shield as quantitative easing is wound down and purchases of Italian bonds fall to zero. There will be no protection by the end of the year. The Draghi pledge to do “whatever it takes” no longer holds.

No future rescue by the ECB is possible unless the Italian government of the day – endorsed by parliament – formally invokes the bail-out mechanisms (OMT-ESM) and accepts austerity imposed by Brussels.

Mario Draghi, head of the Bank of Italy before his ECB appointment

QE, since the programme began in March 2015, the ECB has bought €341bn in Italian bonds

FT 31 May 2018

OMT, Italy and ELA

Bloomberg 29 May 2018

Mario Draghi’s defining moment as ECB president came in July 2012 when he unexpectedly pledged to do “whatever it takes” to preserve the euro.

Outright Monetary Transactions

Under OMT, the ECB would make large-scale purchases of Italian debt, bringing yields down and ensuring the government can fund itself.

There is a catch: The country must apply for it, and must also go to the European Stability Mechanism, the euro area’s bailout fund.

And an ESM rescue comes with conditions requiring economic reforms

Bank of Italy can fund solvent lenders directly through Emergency Liquidity Assistance, at a penalty interest rate.

zc

Otmar Issing vänder sig mot hur ECB-chefen Mario Draghi har drivit igenom obligationsköp

som ska stötta euroländer med stora interna problem som Italien och Grekland

Johan Schück DN 26 maj 2018

IMF calls for an agreement on Greece’s debt by next week

CNBC 15 May 2018

The ECB has soaked up €300bn of Italian debt

buying time for the country to claw its way out of a debt-deflation trap.

Italy has pulled off an “internal devaluation” within the eurozone, albeit at the cost of a deeper depression than the 1930s.

Ambrose Evans-Pritchard Telegraph 13 May 2018

ECB should not have regarded low inflation as a permanent or even long-term condition that demanded an aggressive monetary-policy response.

Jürgen Stark, former Member of the Executive Board of the ECB and former Deputy Governor of the Deutsche Bundesbank, Project Syndicate 19 February 2018

The ECB, in particular, defends its low-interest-rate policy by citing perceived deflationary risks or below-target inflation. But the truth is that the risk of a “bad” deflation – that is, a self-reinforcing downward spiral in prices, wages, and economic performance – has never existed for the eurozone as a whole.

It has been obvious since 2014 that the sharp reduction in inflation was linked to the decline in the prices of energy and raw materials.

The vast bond-buying operations nominally undertaken by the ECB in recent years

have been handled largely by national central banks, which purchase their own governments’ bonds.

Daniel Gros, Procect Syndicate 11 October 2017

“The blunt truth is there is a single monetary policy, but there is not a monetary union,” Mr Tucker said.

Claire Jones, FT 13 November 2017

As Paul Tucker, former deputy governor of the Bank of England, remarked this month at an ECB conference in Frankfurt, the region may have a common currency — but it has many different forms of money.

“The blunt truth is there is a single monetary policy, but there is not a monetary union,” Mr Tucker said. “There are 20 moneys within the European monetary union. There is the money that Mario [Draghi, ECB president] issues, the notes. But these are inconvenient to carry about. Most of the money we use are deposits held in 19 national banking systems.”

The job of a normal central bank faced with this situation is to be the lender of last resort.

But the ECB was deliberately constructed to be different from normal central banks.

Matthew C Klein, FT Alphaville 9 November 2017

One of the most striking moments in the euro crisis saga was when European elites forced Silvio Berlusconi to leave office in favour of unelected Mario Monti. This was possible because Italy is a member of the euro area, and is therefore uniquely vulnerable to capital flight and bank runs.

Spaniards have good reason to hold euros in bank deposits and euro-denominated bonds as their safe asset, but have literally no reason to hold Spanish bank deposits or Spanish government bonds.

At any moment, euro-area creditors could decide they no longer wish to finance a country’s banks and its government.

This arrangement is inherently unstable.

Mr Draghi gave a brutally honest account of central bank failings before the Lehman crisis,

admitting that the orthodoxies of the day bore little relation to reality on the ground.

There was too much trust in the dogma of “rational expectations” and a chronic neglect of how capital markets really work.

Mario Draghi speaking at a forum of Nobel Prize economists at Lake Constance, Ambrose Evans-Pritchard, Telegraph 23 August 2017

Mario Draghi’s ‘whatever it takes’ outcome in 3 charts

Where do we stand 5 years after the ECB head’s famous pledge?

FT 25 July 2017

Policymakers pushed the deposit rate to minus 0.4 per cent, eurozone banks received more than €1tn of liquidity via Long Term Refinancing Operations, and the ECB has purchased over €2tn of government and corporate bonds in a programme which accumulates another €60bn every month.

The European Central Bank has for the first time published its

rule book for giving emergency loans to ailing lenders,

breaking with the secrecy that fuelled controversy over the programme during the financial crisis.

FT 19 June 2017

ECB-sanctioned “emergency liquidity assistance” was a lifeline for a clutch of banks that were cut off from normal financing channels during the crisis.

Greek banks are still using €44bn of ELA help.

ECB’s Coeure calls for clarity on Greece debt relief before QE inclusion

Mehreen Khan, FT 31 May 2017

Mr Coeure added the ECB would have to make its own assessment of Greece’s debt dynamics should the IMF and EU agree on the restructuring to kick in after 2018.

Christine Lagarde said that eurozone creditors must provide considerably more detail on debt relief for Greece

before the fund will take a decision to join the country’s bailout programme.

“There cannot be a specific case for any particular country.”

FT 12 April 2017

ECB faces impossible choice between German overheating or Italian debt storm

When ECB runs out of plausible justifications for why it is still covering Italy's entire budget deficit

and rolling over its existing €2.2 trillion of public debt.

Ambrose, 25 May 2017

“There are risks that euro area bond yields could increase abruptly without a simultaneous improvement in growth prospects,”

said the ECB in its Financial Stability Review released today.

Clemens Fuest, head of the IFO Institute, says ultra-loose policies are distorting the capital markets,

hurting banks and insurance companies, and bleeding savers to help debtors.

QE is near its technical limits anyway. The ECB balance sheet has reached €4.17 trillion, or 39pc of eurozone GDP.

Germany trade surplus of nearly $300bn outpacing China by more than $50bn

Schäuble blames ECB for euro that is ‘too low’ for Germany

FT 5 February 2017

ECB needs to be more clear about its calculation that ailing bank Monte dei Paschi di Siena

needs more than €8 billion pumped into it, Italy's economy minister Pier Carlo Padoan says.

EUobserver, 30 december 2016

cnbc.com/2016/02/07/ecb-may-be-running-out-of-stimulus-options-but

The European Central Bank has come under renewed pressure in Germany,

after a group of academics and business people filed a complaint at the country’s highest court

over the monetary policymakers’ mass bond-buying programme.

FT 16 May 2016

Mario Draghi

Apparently, the chorus of German voices pointing to the obvious - that his policies are killing savers, insurance companies, pension funds and banks — got his dander up:

“We have a mandate to preserve price stability for the whole of the euro zone, not only for Germany,” he said.

“We obey the law, not the politicians, because we are independent.”

Mario Bothers: Germany Takes Aim at the European Central Bank

- In hardly any other euro-zone country is the financial investment sector so dominated by savings accounts and insurance policies.

It is mostly life/retirement insurance policies that are suffering. Insurance providers have primarily invested their customers' money in sovereign bonds. But returns are extremely low, in part because of the massive ECB purchases of such bonds.

German money being thrown out of a helicopter: It would be difficult to find a more fitting image to show people that the money they have set aside for retirement may soon be worth very little.

A few weeks ago, Finance Minister Wolfgang Schäuble warned the ECB head that his ultra-loose monetary policies could "ultimately end in disaster."

David Stockman:

We are now ruled by about 200 unelected central bankers.

He can afford one cappuccino.

Draghi, Dennis, Wolodarski och Tomas Fischer

700 Days In No Man’s Land -- Why They Can’t Keep It Up

David Stockman, January 23, 2016

Germany's Constitutional Court to hear case against ECB bond buying

Todd Buell, MarketWatch, Jan 15, 2016

Most people also understand that the Greek debate is not just about Greece but also about whether or not several other countries

— Spain, Portugal and Italy among them, and perhaps even France — will also have to restructure their debts with partial debt forgiveness.

What few people realize, however, is these countries have effectively already done so once.

Michael Pettis February 25, 2015

I vastly overestimated the risk of /Euro/ breakup, because I got the political economy wrong

— I did not realize just how willing euro elites would be to impose vast suffering in the name of staying in.

Relatedly, I didn’t realize how easy it would be to spin a modest upturn after years of horror as success.

Paul Krugman, NYT 10 June 2015

I’m sorry to say that I completely missed the important of liquidity and cash shortages in driving bond prices in the euro area.

It wasn’t until Paul DeGrauwe weighed in that I realized just how much difference it would make if the ECB did its job as lender of last resort;

if the euro survives, DeGrauwe — and this guy named Draghi, who put his ideas into practice — should get a lot of the credit.

As Greece approaches the mathematical limit of its entitlements under the ELA program,

the ECB may find itself in the untenable position of acting as judge, jury and executioner.

Mark Gilbert, Bloomberg 19 May 2015

Greek banks have been increasingly reliant on emergency liquidity assistance from the European Central Bank since February.

And because Greece's banks only have sufficient collateral to cover 95 billion euros ($106 billion) of ELA funding,

extrapolating the growth in that reliance on a chart delivers a deadline -- May 29:

The success of eurozone QE relies on a confidence trick

Programme’s impact unknown without evidence of how the policy transmits to the real economy

Wolfgang Munchau, FT 22 March 2015

The euro is engaged in two dances of death.

The fact that both /ECB and Greece/ threaten euro destruction is testament to the astonishing mis-construction of the euro itself.

Peter Doyle, an economist and former IMF staffer, FT 10 February 2015

Greece is expected to run out of cash as soon as April 9

- ECB höjer Emergency Liquidity Assistance till grekiska banker till €71.3bn, cirka 664 miljarder kr.

Rolf Englund 26 Mars 2015

“Ending ELA would be a very last-resort type of intervention, paramount to a nuclear option

The European Central Bank is sending a message to the euro-area’s leaders: don’t make us pull the trigger on Greece’s banks.

After ECB blessed the expansion of so-called Emergency Liquidity Assistance by about 5 billion euros on Thursday,

officials are insisting that continued support is contingent on political talks over Greece’s bailout.

The ECB does not want to be pushed into a position where it is making decisions on the future of the Greek banking system

-- and the country’s membership of the euro -- without political cover from European capitals.

Bloomberg, Friday 13th 2015

ELA is funding provided by national central banks at their own risk, and is extended against lower-quality collateral than the ECB itself will accept.

Greece’s lenders now have access to about 65 billion euros in such funds, according to a euro-area central bank official. The expansion from 60 billion euros was reported Thursday by German newspaper FAZ.

An ECB official declined to comment, as is the policy on all ELA operations.

Greek Finance Minister met ECB president.

Analysts said the ECB statement was a sign the meeting had not been a success.

ECB has effectively just given a green light for Greek bank runs

Rolf Englund 5 februari 2015

The ECB may or may not have good reasons to cut off Greece – depending on your point of view – but let us all be clear that such a move would be political.

A central bank that is supposed to be the lender of last resort and guardian of financial stability would be taking a deliberate and calculated decision to destroy the Greek banking system.

Ambrose Evans-Pritchard 2 Feb 2015

In reality, the ECB cannot easily act on this threat.

They do not have the political authority or unanimous support to do so, and historians would tar and feather them if they did.

The ground is shifting in Paris, Rome and indeed Brussels already.

The biggest threat is that the European Central Bank ceases to fund Greece's banks.

ECB may well feel obliged to turn off the tap, since right now it is only financing those banks

because the country is officially complying with the terms of its IMF and eurozone bailout.

The moment that Greece was deemed not to be in compliance, it is difficult to see

how the ECB could continue to provide emergency liquidity assistance to Greek banks.

Robert Peston, BBC economics editor, 2 February 2015

The game is up. It’s time for Greece to leave the eurozone and move on

The stand-off between Greece and the rest of the eurozone will escalate,

neither side will blink and the country will default

Allister Heath, Telegraph 29 Jan 2015

There is now a clear threat of Grexit.

In 2011-12 Mrs Merkel did not want Germany to be blamed for another European disaster,

and both northern creditors and southern debtors were nervous about the consequences

of a chaotic Greek exit for Europe’s banks and their economies.

The Economist, editorial, Jan 31st 2015

Financial Times, 22 January 2015

Knepet är att trycka nya centralbankspengar som sedan används för att köpa statspapper.

Räntorna pressas, och en viktig effekt är att valutan tappar i värde.

Men åtgärderna är kriminellt senkomna och beslutet tas långt efter både Storbritannien och USA.

OECD understryker att ECB:s sedelpress inte kommer att räcka för att lyfta Europas ekonomier.

DN-ledare 23 januari 2015

Den penningpolitiska stimulansen är nödvändig, men effekten avklingande och för att häva sig ur stagnationsfällan krävs andra medel.

Jag tycker det är skriande uppenbart att räntan världen över är för låg och att en större del av stimulanserna borde ske via finanspolitiken.

Rolf Englund 5 december 2009

QE - Monetary easing will not cure structural difficulties.

But the eurozone did not fall into a slump because supply-side problems suddenly became worse.

It faltered because demand collapsed.

Martin Wolf, FT 22 January 2015

If investors perceived that the central bank of Italy, for example, were taking on unaffordable risks when buying Italian government bonds,

at that point the price of those bonds would fall, the implicit interest rate paid by the Italian government would rise,

and the whole point of QE would be blown up.

Robert Peston, BBC economics editor, 22 January 2015

This means that in theory German taxpayers are sheltered from notional exposure to the stretched finances of the Italian or Spanish governments, for example.

But as I explained the other day...

Athanasios Orphanides, a former member of the ECB’s governing council, said it potentially broke EU rules.

“It is as if it’s accepted that the euro area’s modus operandi is to clear things with Germany,

and for the ECB to constrain its actions to what is best for Germany,” he told the Financial Times.

“This is inconsistent with and violates the [EU] treaty.”

FT 20 January 2015

Speaking in front of Mr Draghi and hundreds of other guests at a finance industry reception on Monday,

Ms Merkel warned against using monetary policy to let governments in vulnerable economies off the hook over reforms.

She said: “One must prevent the dealings of the ECB from easing the pressure for improvements in competitiveness.”

QE and central bank solvency

- what would happen to the Eurosystem’s capital resources if a country defaults?

Would this generate a fiscal transfer between members?

Jérémie Cohen-Setton, Bruegel, 20th January 2015

Draghi would like his trillion euros to go to Italian factories to re-equip themselves, to Greek tourist resorts to smarten themselves up,

and to German consumers to spend more on that Italian-made stuff and those Greek holidays.

But banks won’t want to lend to Italian or Greek companies just because they have a lot more money on their balance sheet.

So if a trillion euros get printed in Frankfurt, a lot of it will wash its way across the English Channel.

Matthew Lynn, Telegaph 19 Jan 2015

Economists will no doubt be debating the effectiveness of QE for a couple of generations at least. Yet one thing we know for sure is that when a major central bank prints money, it floods the rest of the world. When Japan started, it fuelled asset booms in the US and Europe. When the Fed and the Bank of England launched QE, much of the money poured into the emerging markets.

In a world where capital is mobile, and there are no controls on its movement, that is what you would expect.

Ever since his “whatever it takes” speech of mid-2012, ECB president Mario Draghi has been hinting that QE salvation is just around the corner.

That’s allowed cash-strapped eurozone governments to borrow at ultra-low interest rates even while presiding over moribund economies and national balance sheets riddled with debt.

Liam Halligan, Telegraph 10 Jan 2015

For a couple of years, then, eurozone stock and bond markets, and their global counterparts, have been pricing in,

ever more enthusiastically, the idea the ECB will ride to the rescue.

Almost everyone is betting on the Frankfurt-based institution joining its US and UK equivalents in using money-from-nothing to buy up vast swathes of government debt,

so “solving” Europe’s chronic state of indebtedness and ensuring the eurozone remains intact.

Yet, Draghi’s plan is probably illegal under EU Treaties.

Next Wednesday, the European Court of Justice (ECJ) will rule on a challenge brought by a group of German activists and politicians.

The ECJ will no doubt fudge the ruling, leaving the too-hot-to-handle decision in Merkel’s court.

Mr Draghi issued his own cri de coeur in Helsinki six weeks ago, laying out the "minimum requirements for monetary union".

His prescription amounts to an EU superstate, with economic sovereignty to be "exercised jointly".

His plea is Utopian. There is no popular groundswell anywhere for such a vaulting leap forward

The northern creditor states have in any case spent the past four years methodically preventing any durable pooling of risk or any step towards fiscal union.

In airing such thoughts, Mr Draghi is really telling us that he no longer thinks EMU can work.

Ambrose Evans-Pritchard 7 Jan 2015

Peter Praet, the European Central Bank's chief economist:

"There is a risk of a real economic vicious cycle: less investment, which in turn reduces potential growth, the future becomes even grimmer and investment is reduced even further," he told Börsen-Zeitung.

Mr Praet warned that an "underemployment equilibrium" is setting in, invoking the term used by Keynes in the 1930s.

He exhorted "all the authorities", including governments, to step up to their responsibilities and take "urgent action".

This is a man who knows that monetary union is in deep crisis.

Italy's political system is going to blow up soon. Its unemployment rate has just reached a modern-era high of 13.4pc,

with youth unemployment hitting a record 43.9pc.

The Mezzogiorno is sliding from depression towards social collapse.

The Telegraph has argued since Maastricht that a currency union of disparate cultures with no EMU treasury or political authority to guide it would end in paralysis

Mr Draghi issued his own cri de coeur in Helsinki six weeks ago, laying out the "minimum requirements for monetary union".

His prescription amounts to an EU superstate, with economic sovereignty to be "exercised jointly".

His plea is Utopian. There is no popular groundswell anywhere for such a vaulting leap forward, and it would imply a technocrat dictatorship beyond democratic control if ever attempted.

The northern creditor states have in any case spent the past four years methodically preventing any durable pooling of risk or any step towards fiscal union.

In airing such thoughts, Mr Draghi is really telling us that he no longer thinks EMU can work. Nobody can fault him for lack of effort.

....

Draghi outlined the minimum requirements needed to complete monetary union in a way that offers

stability and prosperity for all its members

in a speech to students of the University of Helsinki 27 November 2014

Sovereign debt needs also to act as a safe haven in times of economic stress. It can do so first of all through a strong fiscal governance framework.

Secondly, by having some form of backstop for sovereign debt in place. “Over the longer-term”, the President concluded,

“it would be natural to reflect further on whether we have done enough in the euro area to preserve at all times the ability to use fiscal policy counter-cyclically.

But it is also clear that… this could only take place in the context of a decisive step towards closer Fiscal Union”.

Det makroekonomiska argumentet för /eller snarare emot/ EMU

Nils Lundgren i Helsingfors den 21 september 1994

Europe’s QE Quandary

Shouldn't the ECB Buy Bonds, Too?

Jana Randow, Bloomberg, Dec 3, 2014

It’s the new conventional wisdom: When all else fails to make economies grow, create new money and buy government bonds. That’s the formula dubbed quantitative easing, or QE.

Most economists think it helped keep the U.S. and the other countries that used it — Japan and the U.K. — from tumbling into a catastrophic depression. Shouldn’t Europe try it, too?

It’s difficult for the 18-nation euro area to do the same thing, partly because of European Union rules, and partly on concern about fueling asset bubbles.

But now that the European Central Bank has exhausted most other options, it’s pressing ahead with some asset purchases and other QE-like moves to get more cash into the economy.

Mario Draghi's efforts to save EMU have hit the Berlin Wall

If the ECB tries to press ahead with QE, Germany's central bank chief will resign.

If it does not do so, the eurozone will remain stuck in a lowflation trap and Mario Draghi will resign

Ambrose Evans-Pritchard, 5 November 2014

Mr Draghi is accused of withholding key documents from the ECB's two German members, lest they use them in their guerrilla campaign to head off quantitative easing.

This includes Sabine Lautenschlager, Germany's enforcer on the six-man executive board, and an open foe of QE.

David Marsh, author of a book on the Bundesbank and now chairman of the Official Monetary and Financial Institutions Forum,

says the Bundesbank has been quietly seeking legal advice on whether it can block full-scale QE.

It is looking at Articles 10.3 and 32 of the ECB statutes, arguably relevant given the scale of liabilities.

Deep Divisions Emerge over ECB Quantitative Easing Plans

Some view /ECB/ bond purchases as unavoidable, as the euro zone could otherwise slide into dangerous deflation

Others warn against a violation of the ECB principle, which prohibits funding government debt by printing money.

Der Spiegel, 3 November 2014

Is it important that the ECB adhere to tried-and-true principles in the crisis, as Weidmann argues?

Or can it resort to unusual measures in an emergency situation, as Draghi is demanding?

Bundesbank President Jens Weidmann, is opposed to most of these costly programs.

“whatever it takes” to save the euro, including purchasing “unlimited” amounts of struggling governments’ bonds

According to the German Constitutional Court, the policy violates European Union treaties – a ruling that the European Court of Justice is now reviewing.

The ECJ’s decision will have important implications for the eurozone’s future, for it will define what authority, if any, the ECB has to intervene in a debt crisis.

Gita Gopinath, Project Syndicate 3 November 2014

And yet, in a fundamental way, the current debate about OMT misses the point. Rather than asking whether the ECB’s mandate allows it to intervene in a debt crisis, EU leaders should be asking whether it should.

The Bundesbank’s position on this question is well known; a leaked submission to the Constitutional Court last year declared unequivocally that, “It is not the duty of the ECB to rescue states in crisis.”

But there is a strong case for allowing the ECB to act as lender of last resort.

Gita Gopinath is Professor of Economics at Harvard University. She is a visiting scholar at the Federal Reserve Bank of Boston, a research associate with the National Bureau of Economic Research, and a World Economic Forum Young Global Leader

"extend and pretend/delay and pray"

Bank stress tests an unconvincing fudge

Willem Buiter, FT 30 October 2014

EBA, The European Banking Authority, has a long record of stress tests that grotesquely underestimate the capital holes in EU banks.

Both the AQR and the stress test relied heavily on national regulators and supervisors – the very entities on whose watch the excesses that led to the financial crisis were allowed to fester and compound.

They were in charge of the regulatory leniency that permitted the banks in their jurisdictions to engage in lender forbearance (extend and pretend/delay and pray) and to overstate the fair value of their assets.

The adverse scenario was not particularly stressful – no deflation, for instance.

Will the asset quality review and stress tests conducted by the European Central Bank and the European Banking Authority mark a turning point in the eurozone’s crisis?

Leverage is 20 to 1 in Spain and Italy; 25 to 1 in Germany and France; and 30 Lto 1 in the Netherlands.

It is questionable whether this is enough loss-absorbing capital.

Martin Wolf, FT October 28, 2014

Perhaps the most important possibility omitted by this assessment is that of sovereign default.

America’s eight biggest banks used to have 23 times more loans and investments than loss-absorbing capital

Now they are only 14 times “levered”.

The Economist print September 27th 2014

ECB should abolish its OMT program – which, according to Germany’s Constitutional Court, does not comply with EU treaty law anyway.

The fiscal compact – formally the Treaty on Stability, Coordination, and Governance in the Economic and Monetary Union

French Prime Minister Manuel Valls and his Italian counterpart, Matteo Renzi, have declared – or at least insinuated –

that they will not comply with the fiscal compact to which all of the eurozone’s member countries agreed in 2012

Their stance highlights a fundamental flaw in the structure of the European Monetary Union

– one that Europe’s leaders must recognize and address before it is too late.

Hans-Werner Sinn, Project Syndicate 22 October 2014

Some two or three years ago, the European Central Bank (ECB) would have been seen as revolutionary and courageous,

if it had then set about buying bank debt in the form of bonds, including junk from Greece and Cyprus.

Robert Peston, BBC economics editor 2 October 2014

Today, with the eurozone economy still flatlining five years after its crisis erupted,

the ECB inauguration of a two-year programme to nationalise loans to households and businesses

- to the tune of several hundred billions of euros - looks like a slightly desperate last role of the dice.

Since the onset of the eurozone sovereign debt crisis in 2010,

the standard pattern has been to do the right thing between six and 18 months too late,

the delay generally originating in Frankfurt or Berlin.

FT Editorial 2 October 2014

Now is another opportunity to ditch faulty analysis and wrong-headed policy and arrest deflation before it takes hold.

Mr Draghi has shown the right instincts since he took over the ECB presidency.

Only a weak euro can save the ECB now

Lorenzo Bini Smaghi, FT October 2, 2014

Merkel has a duty to stop Draghi’s illegal fiscal meddling

The ECB is overstepping its mandate with anti-deflationary measures

Hans-Werner Sinn, FT September 29, 2014

In the summer of 2012, Mario Draghi, president of the European Central Bank, did something extraordinary.

He said the magic words the “ECB is ready to do whatever it takes to preserve the euro”.

He then waved a wand called “outright monetary transactions”.

Hey presto! The panic in eurozone sovereign debt markets subsided: yields on Italian and Spanish 10-year governments bonds are now below 3 per cent.

Mr Draghi this time seeks to end the threat of deflation. Will he be equally successful?

Experience suggests that only the brave would bet against him.

Yet to succeed twice would be quite a remarkable achievement.

Martin Wolf, Financial Times June 6, 2014

Nominal gross domestic product rose 4 per cent between the first quarter of 2008 and the last quarter of 2013.

Real GDP has stagnated over the three years since the start of 2011.

Further falls in inflation are likely and Japanese-style deflation quite conceivable.

The latter would weaken spending, raise the real burden of debt and make adjustments in competitiveness more difficult.

Indeed even ultra-low inflation greatly raises these risks.

Lagarde och Englund om deflation och inflation

Realräntor - Real Interest Rates

The ECB auction, which will allow banks to borrow up to €400bn in cheap, four-year loans,

comes as markets continue to doubt whether the central bank can return inflation to

its target of below but close to 2 per cent.

FT 16 September 2014

Draghi only had to say "whatever it takes" to end Europe's financial crisis.

But Draghi will actually have to do whatever it takes to end Europe's economic one.

That's what he's trying to do now, but the eurocrats might not let him.

They have their rules, after all.

Matt O'Brien, Washington Post, August 27, 2014

Merkel: Not without Treaty change

Unemployment in the euro area

Speech by Mario Draghi, President of the ECB,

Jackson Hole, 22 August 2014

Draghi’s recent speech at the annual gathering of central bankers in Jackson Hole has excited great interest,

but the implication of his remarks is even more startling than many initially recognized.

If a eurozone breakup is to be avoided, escaping from continued recession will require increased fiscal deficits financed with ECB money.

The only question is how openly that reality will be admitted.

Adair Turner, former Chairman of the United Kingdom’s Financial Services Authority,

member of the UK’s Financial Policy Committee and the House of Lords, Project Syndicate 8 September 2014

Jag tycker det är skriande uppenbart att räntan världen över är för låg och att en större del av stimulanserna borde ske via finanspolitiken.

Rolf Englund blog 5 december 2009

What impressed me was not so much the rate cut, but that Mario Draghi, ECB president,

allowed the decision to be taken on a majority vote. Quite a few central bankers were opposed.

Wolfgang Münchau, FT September 5, 2014

European Banking Authority (EBA) revealed what information would be published about each bank.

The region's 124 most important banks are undergoing an assessment of their risky assets

designed to determine how well they would cope with future market shocks.

CMBC 20 August 2014

Draghi is running out of legal ways to fix the euro

The ECB should starting buying equities and junk bonds. It should subsidise mortgages and consumer credit....

All these measures would be effective. Most would be illegal.

Wolfgang Münchau, FT 17 August 2014

“Not without treaty change.”

It’s hard to believe, but almost six years have passed since the fall of Lehman Brothers

The crisis is by no means over. Recovery is far from complete,

and the wrong policies could still turn economic weakness into a more or less permanent depression.

In fact, that’s what seems to be happening in Europe as we speak.

Paul Krugman, New York Times 14 August 2014

Dragi trollar fram 850 miljarder euro - men vad säger Bundesbank och Författningsdomstolen?

ECB pumps cheap cash into the banks through the targeted long-term loan program,

which kicks in next month and which Draghi says might supply 850 billion euros ($1.1 trillion).

Next, the banks lend that cash to companies.

They then bundle the loans together into asset-backed bonds,

and sell those securities to the ECB.

Mark Gilbert, Bloomberg View 8 August 2014

Formulating monetary policy at the European Central Bank is akin to "herding cats," former Bank of England governor Charles Goodhart said yesterday.

RE: Varifrån får Dragi 850 miljarder euro (cirka 7800 miljarder kr)?

Från sedelpressen, eller, nuförtiden, genom att skriva 850 på datorn och trycka enter.

Se mer om sedelpress här

Asset-backed securities: The key to unlocking Europe's credit markets?

Bruegel 24 July 2014

Draghi insisted that the eurozone’s recovery remains on track

and offered no hint that it had moved closer to embarking on broad-based asset purchases, known as quantitative easing.

He maintained that a weak recovery would continue and longer-term inflation expectations remained anchored to the central bank’s target of below but near 2 per cent.

FT 7 July 2014

“The fundamentals for a weaker exchange rate are much better than they were two or three months ago.”

"stock prices have reached what looks like a permanently high plateau."

ECB’s chief economist Peter Praet:

“Normally, a fall in prices would be able to support purchasing power and, therefore, domestic demand. But ..."

It seems like Praet is not entirely sure about the difference between supply and demand shocks,

but let me just illustrate the dffference in two graphs

The Market Monetarist, Lars Christensen, 15 July 2014

ECBs Outright Monetary Transactions (OMT)

Did the German court do Europe a favour?

ECJ will also not rubber-stamp the OMT – and, if it does, the legal victory will not resolve the fundamental dilemmas

The OMT programme was justified but the fiscal union question remains

Ashoka Mody, Bruegel, 15th July 2014

IMF has issued a blistering attack on Europe’s authorities

“Inflation has been too low for too long.

A persistent failure to meet the inflation target could undermine central bank credibility,” said the IMF

with remarkable bluntness in its annual health report on the currency bloc.

Ambrose Evans-Pritchard 14 July 2014

“A negative external shock could tip the economy into deflation.

The recovery is neither robust nor sufficiently strong.

Financial markets are still fragmented, with contracting credit and high borrowing costs constraining investment in countries with large output gaps,

large debt burdens and high unemployment,” it added.

Gabriel Stein, from Oxford Economics, said the bar for /ECB/ QE remains very high,

whatever EU treaty law says, since it would face huge political opposition in Germany,

where the AfD anti-euro party has recently won its first seats in the European Parliament and

the press views asset purchases as the road to perdition.

The German constitutional court has already ruled that the ECB’s back-stop debt plan for Italy and Spain (OMT) is illegal and probably ultra vires. “The ECB is desperately trying to avoid doing QE. They are hoping that recovery will come along and save them in time.” he said.

Public policy needs to prop up domestic demand until the threat of lowflation has subsided and banks are ready to lend again

IMF Report

TLTRO

The European Central Bank’s decision to cut rates below zero was the headline-grabber but ECB-watchers view

the central bank’s offer of up to €400bn in cheap, fixed-rate loans – known officially as a targeted longer-term refinancing operation (TLTRO) –

as the package’s centrepiece.

Financial Times 6 June 2014

Outright Monetary Transactions OMT

The European Central Bank's outright monetary transactions (OMT) or bond-buying programme was announced by Mario Draghi, president of the European Central Bank, in September 2012.

Under the outright monetary transactions programme the ECB would offer to purchase eurozone countries’ short-term bonds in the secondary market,

to bring down the market interest rates faced by countries subject to speculation that they might leave the euro.

lexicon.ft.com

Schäuble explained that, as far as decisions over OMT bond purchases are concerned, the ECB ”cannot make these decisions because it has bound them to conditions that are beyond its control.”

Schäuble said that these conditions are decided by the European Stability Mechanism, the European governments’ bail-out program.

“ESM decisions are subject to a unanimous vote and we will not approve of such a program as announced by the ECB,” Schäuble explained

— buttressing a belief that, after a two-year interregnum, euro-area jitters may be about to restart.

David Marsh, MarketWatch, June 4, 2014

Otmar Issing, the former chief economist of the European Central Bank and the German Bundesbank,

is a genial number-cruncher who believes in the overall benefits of European integration

has turned virulently pessimistic over the European single currency.

In a marked change from his relative sanguinity during his eight years at the ECB,

he terms member countries’ unreliability on economic policies “a basic design flaw of monetary union.”

David Marsh, Market Watch, Jan. 10, 2011

The ECB saved the euro by providing a backstop to the member states of the single currency in 2012.

That at least is the current received wisdom. I wonder, however, whether that will still be the judgment in two years’ time.

Mr Draghi speech in Amsterdam, he went through a number of “what if” type scenarios with admirable clarity.

One of those was the one we are now in: a worsening of the medium-term outlook for inflation /too low inflation/.

Wolfgang Münchau, Financial Times, May 18, 2014

Otmar Issing, the former chief economist of the European Central Bank and the German Bundesbank,

is a genial number-cruncher who believes in the overall benefits of European integration

has turned virulently pessimistic over the European single currency.

In a marked change from his relative sanguinity during his eight years at the ECB,

he terms member countries’ unreliability on economic policies “a basic design flaw of monetary union.”

David Marsh, Market Watch, Jan. 10, 2011

Complacent policy makers and investors imagine the crisis is over.

Avoiding catastrophe is still not guaranteed. That is anyway a grossly insufficient goal.

Martin Wolf, FT, May 13, 2014

Mario Draghi, president of the European Central Bank, saved the day in July 2012 when he announced that “within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And, believe me, it will be enough.”

He needs to promise to do whatever it takes yet again, to eliminate excess capacity and raise inflation to 2 per cent.

If he does not, crisis might yet return.

I had doubted whether the ECB’s programme for Outright Monetary Transactions would work.

But in the end, this conditional promise by the central bank to purchase government bonds in the secondary markets proved so effective at stopping the panic that it never had to be carried out.

Ireland, Spain and Italy at the end of last year these economies were between 6 per cent and 9 per cent smaller than before the crisis.

Unemployment is very high, especially in Spain. Greece is in still worse shape.

A move to negative interest rates is part of the answer.

So is an asset-purchase programme that would expand the ECB’s balance sheet by buying collateralised private sector assets and government debt

Avoiding catastrophe is still not guaranteed. That is anyway a grossly insufficient goal.

The aim must be to secure a healthy recovery.

‘If the euro falls, Europe falls’ - How the euro was saved - the third part

Angela Merkel was handed the piece of paper Barack Obama had just passed around.

“What is this?” the German chancellor asked. “I haven’t seen this before.”

A full-scale endorsement of a plan for the European Central Bank to protect eurozone countries when they came under attack from financial markets by automatically buying their bonds.

In retrospect, it marked the beginning of the final turning point in the crisis.

Peter Spiegel, Financial Times, 15 May 2014

Three months after the testy exchange, Ms Merkel would give her tacit endorsement to an equally ambitious bond-buying scheme designed by another Italian technocrat, ECB president Mario Draghi.

This would end the existential crisis that had faced the euro for more than three years.

That plan – unveiled after ECB staff spent a furious summer constructing the system following Mr Draghi’s declaration he would do “whatever it takes” to ensure the euro’s survival – has long been hailed as the coup de grâce of the eurozone crisis.

Yet Mr Draghi’s programme was unlikely to have quelled markets without Ms Merkel’s acquiescence, which was given despite the public objections of the powerful German Bundesbank.

Under article 123 of the Treaty of Lisbon, the ECB is prevented from buying the government bonds of member states,

but it has nonetheless already promised to do so even though the threat was never carried out.

The ECB does not appear to find this rule wise and its members are not threatened with jail it it is broken.

Andrew Smithers FT 16 May 2014, click

Article 123 of the Treaty of Lisbon

How the euro was saved

In the French seaside resort of Cannes

To the astonishment of almost everyone in the room, Angela Merkel began to cry.

the man sitting next to her, French President Nicolas Sarkozy, and the other across the table, US President Barack Obama

Peter Spiegel, Financial Times 11 May 2014

https://twitter.com/TeresaKuchler

Europeiska centralbankens (ECB) högste chef Mario Draghi

Nu har det snart gått två år sedan italienaren uttalade de numera välkända orden

”Inom ramen för vårt mandat, är ECB redo att göra allt som krävs för att rädda euron. Lita på mig, det kommer att räcka”.

Louise Andrén Meiton, SvD Näringsliv, 6 mars 2014

Inom teaterns värld finns begreppet peripeti, en avgörande vändpunkt i ett antikt drama. Som när kung Oidipus inser sitt öde. Det finns ett tydligt före och ett efter. I den ekonomiska världen har Mario Draghis uttalande fått samma tyngd.

Få talar numera om eurons kollaps. Men desto fler talar om ECB:s möjliga åtgärder.

Vad kan då ECB göra? En möjlig åtgärd är att sänka räntorna.

Men med en styrränta på 0,25 procent och en inlåningsränta på 0 procent är handlingsutrymmet begränsat.

Ett ord är viktigt, mandatet. Centralbanken har lovat att köpa oändliga belopp av ett krisdrabbat lands obligationer, om landet genomför reformer och besparingar.

Men nyligen förklarade den tyska författningsdomstolen att de ser problem med ECB:s plan och att de anser att centralbanken har överskridit sina befogenheter.

Den tyska Författningsdomstolen

Low inflation has, as is to be expected, coincided with weak demand.

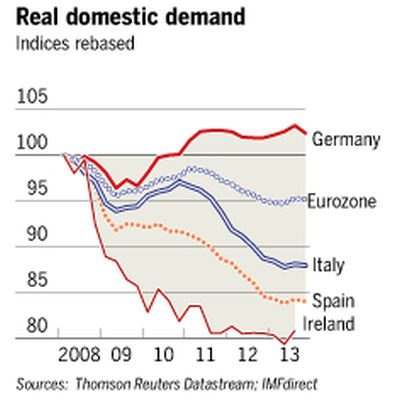

In the fourth quarter of last year, eurozone real demand was 5 per cent below levels in the first quarter of 2008.

In Spain, real demand fell 16 per cent. In Italy, it fell 12 per cent.

Even in Germany, real demand stagnated from the second quarter of 2011: this is no locomotive.

Martin Wolf, FT 11 March 2014

Nice chart

These concerns have led the Bank of Italy to conduct its own intensive examinations across the nation, such as the one at Banca Alberobello, ahead of the ECB tests. From Banca di Sicilia in the deep south to Banco di Trento e Bolzano, in the German-speaking northeast, the Bank of Italy is staging its toughest examination of the nation’s banks in history.

Financial Times, 4 March 2014

Draghi's Monetary Nightmare

European Private Lending Remains Stuck At Record Low Levels

Tyler Durden,2/27/2014

Can the European Central Bank legally act as lender of last resort to ensure the survival of the euro?

This question is of fundamental importance for the sustainability of the monetary union.

Recently, the German Constitutional Court ruled that it cannot.

In the court’s view the ECB has the power to conduct monetary policy,

but not to support member states in financial distress even if necessary to ensure the survival of the common currency.

Katharina Pistor, Vox, 26 February 2014

RE: Det förefaller som om det var Fed och inte ECB som ställde upp som Lender of Last Resort för de europeiska bankerna

som professor Pelotard har viskat i mitt öra.

The Fed's $600 Billion Stealth Bailout Of Foreign /European/ Banks Continues

At The Expense Of The Domestic Economy, Or Explaining Where All The QE2 Money Went

Many speculated that the US central bank would primarily focus its "rescue" efforts on US banks,

not US-based (or local branches) of foreign (read European) banks:

after all that's what the ECB is for.

Tyler Durden, zerohedge, 6 December 2011

Europe or Democracy?

What German Court Ruling Means for the Euro

Either the European Court of Justice has to stop bond purchases or German justices will.

SPIEGEL Staff, February 10, 2014

When Europe’s leaders set out in June 2012 to break the “vicious circle” between banks and sovereigns,

they left rules for treating government bonds untouched, an oversight that may subvert their drive to prevent a recurrence of the debt crisis.

Under EU rules, banks can rate all debt issued by the bloc’s 28 national governments as risk-free,

avoiding any increase in their capital requirements.

Bloomberg, 10 February 2012

This encourages so-called carry trades, whereby lenders borrow at low cost from the European Central Bank and plow the money into state debt that offers higher returns.

EMU:s chef för banktillsynsmyndigheten SSM, Danièle Nouy:

"En av de största lärdomarna av den nuvarande krisen är att det inte finns någon riskfri tillgång, så statspapper är inga riskfria tillgångar.

Det har visat sig, så nu måste vi reagera"

Rolf Englund blog med länkar 10 februari 2014

Germany's constitutional court

The European Court of Justice will now decide the legality of the so-called debt "backstop", introduced in 2012.

Although the ECB has not used the emergency power, its existence calmed turmoil in European financial markets.

When he announced the Outright Monetary Transactions (OMT) programme, ECB President Mario Draghi said he would do "whatever it takes" to save the single currency.

BBC 7 February 2014

"There are important reasons to assume that it exceeds the European Central Bank's monetary policy mandate and thus infringes the powers of the member states."

The /German Constitutional/ court concludes that OMT violates the German constitution.

It accuses the ECB of making a power grab by extending its own mandate.

It says the scheme endangers the underpinnings of the eurozone rescue programmes.

Worse, it says OMT undermined deep principles of democracy.

Wolfgang Münchau, FT 9 February 2014

Germany’s top court has issued a blistering attack on the European Central Bank,

arguing that its rescue plan for the euro violates EU treaty law and exceeds the bank’s policy mandate.

The tough language leaves it doubtful whether the ECB’s back-stop scheme for Spanish and Italian bonds can be implemented if Europe’s debt crisis blows up again,

and greatly complicates any future recourse to quantitative easing if needed to head off Japanese-style deflation.

Ambrose Evans-Pitchard, 7 Feb 2014

I’m the German Constitutional Court, get me out of here!

Court sees ECB bond buying as illegal but refers questions to ECJ

Open Europe Flash Analysis, 7 Feb 2014

The Fed's $600 Billion Stealth Bailout Of Foreign /European/ Banks Continues

At The Expense Of The Domestic Economy, Or Explaining Where All The QE2 Money Went

Many speculated that the US central bank would primarily focus its "rescue" efforts on US banks,

not US-based (or local branches) of foreign (read European) banks:

after all that's what the ECB is for.

Tyler Durden, zerohedge, 6 December 2011

Janet Yellen announced February 19th that America’s central bank is moving to

cut off the massive financial lifeline that has been subsidizing the European banking system since the beginning of the global financial crisis in March of 2008.

By delaying foreign bank compliance with the stringent capital and borrowing requirements of section 165 of the Dodd–Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) imposed on American banks,

the Fed was engaging in the moral hazard of allowing Europe to borrow at virtually zero interest from the Fed to fund its bloated social welfare states.

Chair Yellen’s actions mean the Fed is cutting off Europe and providing greater support for U.S. borrowing.

Breitbart, 24 February 2014

Whatever happened to the eurozone crisis?

To many people the eurozone crisis has disappeared. It is off the front pages.

It has certainly left the TV screens. I have heard prime ministers and presidents declare the crisis "over".

It needs to be said at the outset that Europe is still enjoying the "Draghi effect":

the reassurance given by the President of the European Central Bank (ECB) that he would do "whatever it takes" to defend the euro

- and no-one seems willing to bet against the ECB.

Gavin Hewitt, BBC 28 January 2014

Longer-Term Refinancing Operations

When the eurozone debt crisis was at its most intense in late 2011, Mario Draghi, the new ECB president,

decided to flood banks with a “wall of money”.

Eurozone banks were urged to take advantage of cheap three-year ECB loans, or “longer-term refinancing operations”,

The sweetener helped ensure the LTROs were successful in averting disaster:

banks borrowed more than €1tn and the eurozone crisis eased, at least temporarily.

FT 23 January 2014

Marknaderna skiter i hur det går för Spanien, Grekland, Italien och andra krisländer

Det enda marknaderna bryr sig om är om dessa länders obligationer kommer att inlösas på förfallodagen, eller ej.

Rolf Englund blog, 10 januari 2014

Att dessa länders räntor nu har sjunkit är således inte något tecken på att marknaderna tror att dessa länders ekonomier är på rätt väg.

Det som gjort att räntorna gått ner är att marknaderna nu tror att ECB kommer att förse dessa länder med nya lån om det skulle behövas så att de kan lösa in sina obligationer på förfallodagen.

Skuldländerna har således fått om inte en egen sedelpress så i alla fall tillgång till ECBs sedelpress.

It is two years since Mario Draghi launched his first big policy initiative as ECB president,

with the longer-term refinancing operation gratefully taken up by about 1,000 banks across the eurozone

The €1tn flood of cheap money extended under the scheme has served three vital purposes.

atrick Jenkins, FT, November 27, 2013

First, it ensured governments had ready buyers for the debt they needed to keep issuing. Even as banks have derisked since the crisis, cutting loans to companies and individuals, they have amplified their investment in sovereign bonds

Second, the LTRO’s low interest rate, now just 0.25 per cent, inflated banks’ profit margins, allowing weaker institutions to build up capital reserves.

Third, it levelled the playing field for banks across the region, albeit artificially. For the first time in an age Portuguese banks were borrowing money at the same price as their German counterparts

Given the benefits, it has been unsurprisingly popular.

Though more than a third of the money has been repaid early as banks have sought to prove their newfound strength, €630bn is outstanding

and Mr Draghi has been lobbied to extend the programme when it expires in a year.

Mike Amey from the bond fund Pimco said the eurozone is “sleepwalking into a decades-long deflation trap” like the Japanese in the 1990s when they mistook near zero rates for easy money. The region has no margin for error as its ageing crisis takes hold.

While gentle deflation can be benign in low-debt economies, it plays havoc with the debt dynamics of leveraged economies,

an effect described by US economist Irving Fisher in his 1933 classic “Debt-deflation Theory of Great Depressions”.

Ambrose Evans-Pritchard, 7 Jan 2014

The Brussels think-tank Bruegel said deflation risks pushing Italy and Spain into a “runaway debt trajectory” as the debt stock rises on a shrinking or static nominal base.

Day by day it is becoming more and more clear that the euro zone is heading for deflation and

despite of this the ECB so far has failed to act and it is blatantly obvious that

the ECB is in breach of its own mandate to secure "price stability" defined as 2% inflation.

The Market Monetarist, 7 January 2014

The failure to act is also a clear demonstration that the ECB in fact has an asymmetrical monetary policy rule (what I have called the Weidmann rule). The ECB will tighten monetary policy when inflation increases, but will not ease when inflation drops.

Depressing...

Why Draghi was wrong to cut interest rates

Deflation in parts of a currency union is not the same as deflation of a union as a whole

Hans-Werner Sinn, Financial Times, November 13, 2013

Deflation in parts of a currency union is not the same as deflation of a union as a whole, because its internal effects on competitiveness cannot be compensated for by exchange rate adjustments.

In fact, Greece, Spain and Portugal need to devalue in real terms by about 30 per cent relative to the eurozone average in order to correct the distortions that were brought about before the crisis by the inflationary credit bubble created by the single currency and thus restore their competitiveness.

The ECB should not act against moderate deflation in these countries, but rather aim to offset such deflation by inflating the northern eurozone – Germany, in particular.

With its Outright Monetary Transactions programme, through which its offers to purchase government bonds of troubled countries at the taxpayers’ risk, the ECB is escorting private German savings again to southern Europe, where they are reluctant to go voluntarily.

The ECB has also been relocating its (electronic) printing presses from the northern to the southern central banks through its policy of allowing junk assets to be used as collateral for its lending to needy commercial banks.

These schemes have exported more public capital from north to south than the official rescues.

Growth rates have remained stubbornly low and unemployment rates unacceptably high,

partly because the increase in money supply following QE has not led to credit creation to finance private consumption or investment.

Nouriel Roubini, Project Syndicate, 31 October 2013

Instead, banks have hoarded the increase in the monetary base in the form of idle excess reserves. There is a credit crunch, as banks with insufficient capital do not want to lend to risky borrowers, while slow growth and high levels of household debt have also depressed credit demand.

As a result, all of this excess liquidity is flowing to the financial sector rather than the real economy.

Since the end of the credit boom in 2008, cross-border claims of banks based in the eurozone core (essentially Germany and its smaller neighbors)

toward the eurozone periphery have plummeted from about € 1.6 trillion to less than half that amount.

Part of the difference has ended up on the ECB balance sheet, but this cannot be a permanent solution.

Daniel Gros, Director of the Brussels-based Center for European Policy Studies, Project Syndicate, Nov. 6, 2013

Lånen och stödköpen har inte i första hand gynnat grekerna.

Istället har pengarna gått till de främst tyska och franska banker som hade tagit stora positioner i Greklands och de andra krisländernas statsobligationer.

Genom att sälja sina obligationer till EU-fonderna, ECB och IMF har bankerna sluppit undan hotande förluster.

Mats Persson, Axess Nr 8, 2013

IMF har uppskattat att banker i Spanien, Italien och Portugal hotas av förluster på 250 miljarder euro, 2 200 miljarder kronor, bara på sina lån till företag.

Siffran motsvarar en tredjedel av bankernas totala kapital.

Wolfgang Münchau, kolumnist i Financial Times, har uppskattat de totala förlusterna i euroländernas banker till 2 600 miljarder euro, 23 000 miljarder kronor (!).

Andreas Cervenka, SvD Näringsliv 2 november 2013

det behövs pengar utifrån, mer specifikt från den gemensamma europeiska räddningsfonden ESM. Problem 1: Tyskland vill inte utan kräver istället att alla bankernas långivare betalar mer innan skattepengar ens kommer ifråga. Tyskland och andra länder är också emot en gemensam insättningsgaranti för eurozonens banker, en förutsättning för att undvika massuttag och seriekonkurser vid en ny kris.

The German banking system appears healthy at first sight.

It certainly fulfils its function of providing the private sector with credit at low interest rates.

But I still find it hard to believe that the German banking system as a whole is solvent.

The country has been running large current account surpluses for a decade, currently at about 6 per cent of gross domestic product.

This means German banks must have been building up huge stocks of foreign securities – a large yet unknown proportion of which are likely to default,

especially if the main crisis resolution tool turns out to be a bail-in of investors.

Wolfgang Münchau, FT, June 23, 2013

Deutsche Bank has one of the lowest leverage ratios of large banks globally

Financial Times, July 21, 2013

Svaret på galaxens alla frågor är inte 42.

För ekonomi och banker är svaret 20.

Rolf Engluns blog 23 augusti 2013

Outright Monetary Transactions

Tuesday was not an easy day for Asmussen, a member of the ECB's executive board, who was called

to testify before Germany's highest court in defense of an ECB program which,

while having proven to be economically successful, might be in violation of the law.

Der Spiegel, June 12, 2013

“probably the most successful monetary policy measure undertaken in recent times”.

Mr Draghi's robust defence of OMT, which was opposed by Germany’s Bundesbank and stirred controversy in Germany,

comes ahead of court hearings at the constitutional court in Karlsruhe

which is considering the legality of the scheme under Germany’s Basic Law.

Financial Times 6 June 2013

ECB sänker räntan med 0,25 procent

"Central bankers say they are flying blind", "Uncharted territory", "No one fully understands"...

IntCom 2 Maj 2013

Mario Draghi has revealed that some eurozone policymakers wanted to slash interest rates more aggressively this month,

said it was ready to enter uncharted territory and introduce a negative deposit rate.

No one fully understands why rates have fallen so far so fast,

and therefore no one can be sure for how long their current low level will be sustained.

Economists simply have little idea how long it will be until rates begin to rise.

Kenneth Rogoff and Carmen Reinhart, Financial Times May 1, 2013

Central bankers say they are flying blind, FT

Growing concern at the IMF over the long-term side-effects of interest rates close to zero came

as some of the leading figures in central banking conceded they were flying blind when steering their economies.

Lorenzo Bini Smaghi, the former member of the European Central Bank’s executive board,

captured the mood at the IMF’s spring meeting, saying: “We don’t fully understand what is happening in advanced economies.”

Financial Times, April 17, 2013

1992

Det erinrar om dagens situation där i USA centralbankschefen Greenspan försöker uppnå en "soft landing" på ekonomins hangarfartyg.

Han känner att han inte kommer fram, drar gasen - räntan - i botten, men motorn, penningmängden, svarar inte. Farten sjunker ändå.

Grant drar också en mycket tänkvärd parallell mellan England och USA på 1920-talet och Japan och USA på 1980- och 90-talen.

England hade 1925 under finansminister Churchill återgått till guldmyntfonten på en då orealistisk växelkurs (den som rådde före första världskriget).

Bank of England förmådde USA att sänka räntan mot slutet av 1920-talet. Detta ledde till att aktiespekulanterna fick ny kraft inför 1929.

I mitten på 1980-talet var det USA som på hotellet Plaza (ägt av Donald Trump) fick japanerna att sänka sin ränta, vilket ledde till den japanska bubbla som nu spricker och hotar hela världsekonomin.

Rolf Englund på DN Debatt 26/8 1992

Mr Wolf’s implicit point that this ECB de facto guarantee of eurozone sovereign debt has reduced the need for austerity is largely correct.

While austerity was not optional for most of the 2010-13 sovereign debt and banking crisis, it is mostly optional now.

Roger Altman, FT 13 May 2013

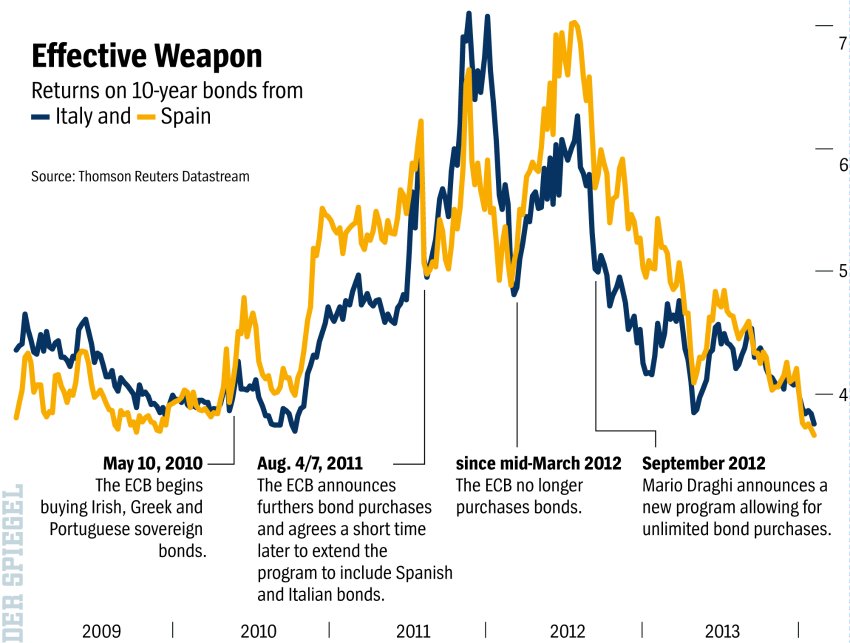

The decline in yields on Spanish debt, shown so clearly in the chart, dates almost precisely to 26th July 2012,

the date on which Mario Draghi, president of the ECB, told an audience in London that

“Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.”

This statement, in turn, led to the announcement by the ECB on August 2nd 2012 of “outright monetary transactions” which would be aimed “at safeguarding an appropriate monetary policy transmission and the singleness of the monetary policy”.

Rightly or wrongly, markets concluded that the risk of an outright default on Spanish bonds had largely disappeared.

Martin Wolf, Financial Times, 10 May 2013

Mario Draghi has again made clear in recent speeches that fixing the structural economic problems of Spain and the rest cannot be the job of the ECB.

But he has also said the ECB will continue to fight the balkanisation of European finance.

Stephanie Flanders, BBC Economics editor, 1 May 2013

These charts (page 6 of presentation attached) from a recent speech by ECB Vice President Vitor Constancio show that, although borrowing costs have fallen in much of the periphery when it comes to households and companies there's still a wide gap between German interest rates and rates at the periphery.

In the jargon, the "transmission mechanism" for the ECB's monetary policy is still impaired,

and credit is still crunched in the countries that need it most.

All of which may help to explain why market expectations surrounding this ECB meeting have been so high

- and expectations among economists are so low.

Fragmentation and rebalancing in the euro area (slides from the presentation)

Presentation by Vítor Constâncio, Vice-President of the ECB,

Joint EC-ECB Conference on Financial Integration, Brussels, 25 April 2013

ECB is under no illusion that a rate cut will do much good

It knows monetary policy is already too loose for Germany

(let’s hope flush German bankers don’t do anything reckless).

For much of southern Europe, however, its “transmission mechanism”

– the way lower policy rates are conveyed to the real economy – is broken.

Financial Times, 30 April 2013

Small businesses in Italy are paying interest rates German rivals were paying before Lehman Brothers’ collapse in late 2008 led to central banks slashing interest rates globally

– a fact that encapsulates all the weaknesses of banks across the eurozone’s southern periphery.

French and German banks reduced their exposures to these markets by some 30-40 percent

ECB has taken extraordinary action to protect monetary union with the LTRO and conditional OMT.

Unfortunately, fragmentation continues and remains debilitating.

A common safety net is another essential element.

This would involve common deposit insurance and common backstop.

The other union Europe needs to contemplate is fiscal union.

David Lipton, First Deputy Managing Director IMF, April 25, 2013

Bundesbank takes aim at Mario Draghi’s ECB rescue plan in an opinion written for the German constitutional court.

ECB’s main justification for the programme

– that its interest rates were not being transmitted to the real economy in stressed countries because of speculation about a euro break-up

– relied on “strongly subjective elements” in assessing the effectiveness of this so-called transmission mechanism.

Financial Times, April 26, 2013

Revealed in an opinion written by the Bundesbank for the German constitutional court are a series of detailed objections to the plan.

The opinion, dated December 21, was not public but the German newspaper Handelsblatt said it obtained the document, which it also published on its website.

The Bundesbank said the ECB’s main justification for the programme – that its interest rates were not being transmitted to the real economy in stressed countries because of speculation about a euro break-up – relied on “strongly subjective elements” in assessing the effectiveness of this so-called transmission mechanism.

The bank also argued that it is not the role of a central bank to guarantee the irreversibility of the currency, a pledge Mr Draghi has made several times.

The legal opinion is a submission in a case to be heard in June by the constitutional court against the establishment of the eurozone’s permanent rescue fund, the European Stability Mechanism.

Bundesbank president Jens Weidmann has been public from the outset in his institution’s opposition to the Outright Monetary Transactions programme launched in September by Mario Draghi, ECB president, after pledging to do “whatever it takes” to save the euro.

Spaniens statliga pensionsfond nu har 97 procent av sina tillgångar i spanska statspapper.

Moody’s rapport om de spanska bankerna. Andelen dåliga lån är uppe i 10,8 procent eller motsvarande 160 miljarder euro.

Många av bankerna är beroende av nödlån från ECB för att klara sig.

En annan stor risk enligt Moody’s: bankernas stora exponering mot spanska statspapper.

Bankerna har, vid sidan om pensionsfonder, nämligen stödköpt det egna landets skuldebrev i enorm omfattning.

Andreas Cervenka, SvD 5 april 2013

ECB to Push Cyprus Over the Brink

Will they really cut off all forms of support? That would give Cyprus no choice but to leave the Eurozone and could easily cause a chain reaction all across the periphery.

If they didn’t withdraw support they would be admitting that their threats were empty and would be encouraging every periphery country to openly defy them.

Naked Capitalism 21 March 2013

Now some believe that the ECB might extend the timetable. But I can think this will happen only if Cyprus has capitulated and there are merely some formalities to be tidied up. Eurozone officials were making threatening noises all during the day Wednesday about how Cyprus could not keep its banking system shut much longer.

So all eyes will be on the Cyprus parliament. Will it defy the Eurocrats or surrender to their will? As our accompanying Cyprus post describes, the island nation has no good choices. The one that is most destructive to all parties, that of a Eurozone exit, looks more likely than it should under any sane calculation.

Full textECB PRESS RELEASE 21 March 2013

Governing Council decision on Emergency Liquidity Assistance requested by the Central Bank of Cyprus

The Governing Council of the European Central Bank decided to maintain the current level of Emergency Liquidity Assistance (ELA) until Monday, 25 March 2013.

Thereafter, Emergency Liquidity Assistance (ELA) could only be considered if an EU/IMF programme is in place that would ensure the solvency of the concerned banks.

Click

Cyprus - The disaster scenario

If it fails to convince the eurozone that it has a viable alternative to bailing in depositors,

then the ECB could decide that Cypriot banks are no longer eligible for the eurosystem’s emergency loans,

known as Emergency Liquidity Assistance (ELA), which is now the only thing keeping the island’s banks afloat.

That is the gun pointing at Mr Anastasiades’ head, something made clear to him by ECB officials at the late-night negotiations

Financial Times, 20 March 2013

Without eurozone liquidity, Cyprus has no central bank to prop up its banks like a non-eurozone country does.

So either Cyprus becomes an economy with no money and reverts to the barter system,

or Nicosia would have to start printing its own currency to keep its banking system running.

When Cypriots next go into their bank branches they may be withdrawing Cypriot pounds.

The ECB’s next governing council meeting, when any decision to withdraw ELA could be taken, is on March 28.

Jens Weidmann, president of the Bundesbank

and a member of the ECB's governing council,

Only politics, not the ECB, can solve the euro zone crisis

"We should quickly revert to our core business, which is monetary policy,"

CNBC 12 Mar 2013

"We face a structural crisis in Europe. We face a crisis of confidence, and this can only be overcome if politicians really tackle the root causes," Weidmann told CNBC in an interview.

"Monetary policy can only buy time at best. ... In that sense, I am a bit concerned about some of the expectations around the power and potential of monetary policy actions."

Weidmann said central bank actions had blurred the line between monetary and fiscal policy during the crisis.

"We should quickly revert to our core business, which is monetary policy," he said.

Former Central Bank Head Karl Otto Pöhl:

Bailout Plan Is All About 'Rescuing Banks and Rich Greeks'

Der Spiegel May 18, 2010

The 750 billion euro package the European Union passed last week to prop up the common currency has been heavily criticized in Germany. Former Bundesbank head Karl Otto Pöhl told SPIEGEL that Greece may ultimately have to opt out, and that the foundation of the euro has been fundamentally weakened.

Eurozone sovereigns will emphatically not be bailed out by their fellow governments following solemn announcements.

Instead, they’ll be bailed out by “exceptional liquidity assistance” (ELA),

which means the sovereigns’ own banks will write cheques to their local banks against the security of national bonds.

Totally different, you see.

Instead of money created by the ECB, this is money created by the ESCB, or European system of central banks.

John Dizard, Financial Times March 8, 2013

By now it has become ever more clear that euro area policy is to make sure absolutely nothing happens

until after the German elections in September 2013.

John Dizard, Financial Times 16 December 2012