Related: USD/SEK - Trichet - Tyskland - Frankrike - Stabilitetspakten - ECB Watch - ECB

Euron and ECBThe krona has gained 7.9 percent on a correlation-weighted basis against a basket of nine other developed-world currencies tracked by Bloomberg

J. Bradford DeLong, professor vid universitetet Berkeley i USA

The ECB’s primary inflation mandate, which it interprets as keeping inflation just below 2 percent in the medium term, is enshrined in 1991’s Maastricht accord. Once this is achieved, the rulebook also allows it to “support the general economic policies” aimed at delivering high growth, social protection and economic convergence.

"Sist men inte minst ger euron EU-invånarna en handfast symbol för den europeiska identiteten.

Det är en symbol att vara stolt över, i takt med att euroområdet växer och mångdubblar fördelarna för sina nuvarande och kommande medlemmar". EU-Kommissionen Mer om EUs symboler  Euron mot Kronan 12 månader augusti 2010  ”Vår randvaluta blir en skvalpvaluta”

Carl Bildt, referat på Ja-sidans Europafokus   "Eurons roll som reservvaluta är nu ifrågasatt", konstaterar SEB:s chefekonom Robert Bergqvist i ett marknadsbrev på fredagsmorgonen. E24/TT 14 maj 2010 Exchange offices in the UK have stopped selling 500 euro banknotes En valutaunion ökar handeln. Det kan röra sig om 30–50 procent på lång sikt. "Det finns inget tystare än en ämbetsman klättrande i sin karriärstege". Ökad handel är det starkaste ekonomiska argumentet för att Sverige ska införa euron Britain, Denmark and Sweden Would Gain Little Trade from Joining the Euro In the continuing controversies about Europe's bold experiment in monetary union, there has at least been some agreement about where the costs and benefits lie. The costs are macroeconomic, caused by forgoing the right to set interest rates to suit the specific economic conditions of a member state. The benefits are microeconomic, consisting of potential gains in trade and growth as the costs of changing currencies and exchange-rate uncertainty are removed. Furthermore, the gain does not build up over time but has already occurred. And the three European Union countries that stayed out—Britain, Sweden and Denmark—have gained almost as much as founder members, since the single currency has raised their exports to the euro zone by 7%. The intractable difficulties in working out the trade effect from previous currency unions means that previous estimates are fatally flawed. The euro hit a fresh record high against the yen of Y146.56 The euro is, and will remain, strong.

Kark-Heinz Grasser, Wall Street Journal, June 17, 2005 Mr. Grasser is Austria's finance minister.     Rolf Englund: EU website on economic and financial affairs - EU Observer about Euro - Dollarn The Euro Homepage by Giancarlo Corsetti

Euron spricker

när dollarn faller The eagle (the dollar) is

landing Eurons första kurs mot kronan var 9.39 - den 5 januari 1999 21 maj 2002: 1 Euro 9:16 - 1 Dollar: 9:97

An unsustainable black

hole

"en ny bankliknande monsterstruktur som med hjälp av belåning ska kunna låna ut bortåt 18500 miljarder kronor Men hur löser man då en kris som lett till överbelåning i hushåll, banker, stater, ja till och med i den egna centralbanken? Enkelt. Skapar en ny bank förstås! Det är i alla fall vad Bryssels bästa och brajtaste tycks skissa på, enligt diverse läckor. De cirka 4000 miljarder kronor som pumpas in i den europeiska nödfonden EFSF är tänkta att bli grundplåt i en ny bankliknande monsterstruktur som med hjälp av belåning i sin tur ska kunna låna ut bortåt 18500 miljarder kronor (!) till euroländer och banker som ligger risigt till. Brandvägg är eurokraternas namn på denna konstruktion. Därför det frenetiska arbetet – inte i första hand för att ”rädda Grekland” utan We are now in the stage of the crisis where people get truly desperate. Markets are convinced that Europe is preparing to massively increase the reach of the euro backstop fund known as the EFSF.

ECB has a total exposure of about 444 bn euros to 'struggling eurozone economies' In a report published on Monday entitled A House Built on Sand?, Open Europe has calculated that the ECB has a total exposure of about €444bn to "struggling eurozone economies". "The ECB is ultimately underwritten by taxpayers which means there is a hidden – and potentially huge – cost of the eurozone crisis to taxpayers buried in the ECB's books." "The euro at $1.50 is a disaster for the European economy and industry," The ECB estimated bank writedowns total of $649 billion, ECB marking its 10th anniversary June 1, has failed in each of the last eight years to achieve its aim of bringing inflation below 2 percent. Trichet, 65, recently stepped up defense of his goal, arguing May 8 that a revision would ``unanchor'' inflation expectations. He maintains that investors ``have not lost faith'' in the ECB's ability to deliver price stability and that only temporary ``shocks'' have caused its ceiling to be breached. The European Commission Predicts Weaker Growth, Higher Inflation in 2008 Ségolène Royal, socialist candidate for the presidential elections: France's prime minister Dominique de Villepin: France's prime minister said the euro's current exchange rate was hurting some exporters "The euro has allowed the creation of a stable environment between all the European partners. But its current level hurts some of our exports," Dominique de Villepin said. Mr. de Villepin said there is a need for Europe to make a clear choice in favor of defending its interests, "rather than remaining the only trading power in the world that doesn't have effective rules against the excesses of globalization." Slovenia is now clear to join the 12-member eurozone on 1 January 2007 and EU finance ministers are due to set the exchange rate next month. "Kronans berg-och-dalbana är inte långsiktigt bra för svensk ekonomi" Kronans berg-och-dalbana är inte långsiktigt bra för svensk ekonomi. Den skapar djup osäkerhet för många av de företag som ska skapa de nya jobben; småföretagare ägnar sig i allmänhet inte åt terminssäkring och valutaspekulation. Desto gladare är de globala valutaspekulanterna - inklusive de stora svenska exportföretagens finansavdelningar - som kan leka med en liten fisk i det stora finanshavet och tjäna grova pengar. En majoritet av svenska folket har sagt ja till denna valutapolitik genom att säga nej till EMU. Det är bara att respektera resultatet. Man kan inte få allt här i livet. I förhållande till euron är och förblir kronan en liten och instabil skvalpvaluta. Under vissa perioder är det lugnt, men när det blåser upp visar kronan hur känslig den är. Nejsidans paradargument var att vi i Sverige måste bevara vår "självständighet". Visst, det är bara att läsa dagens kronkurs för att se hur mycket den fiktiva självständigheten är värd. Mer ur Expressen om EU och EMU

Klas Eklund: - Men innan man blir upphetsad över det ska man ska komma ihåg att syftet med räntesänkningen i somras var att få upp aktiviteten i den svenska ekonomin och få upp inflationen, som var för låg. Han är inte det minsta orolig för de senaste månadernas kraftiga kronförsvagning. Konjunkturinstitutets chef Ingemar Hansson: Bara tre gånger under de senaste tio åren har kronan varit svagare mot euron (och dess föregångare ecun) än vad den är i dag. Kronans kurs mot euron var i genomsnitt 5 procent starkare under 1995-2000 än genomsnittet för 2001-2005. Detta trots att bytesbalansöverskottet har varit mer än dubbelt så stort under den senare perioden. De offentliga finanserna har varit i värre skick, tillväxten är något bättre än i det håglösa Euroområdet, inflationen är låg och överskottet i utrikeshandeln är stort. Sweden's current account surplus is equivalent to 3 per cent of GDP. The worst-performing currency in the world this year has been the Swedish krona, dubbed "Europe's yen" by one fund manager. Sweden's economy has flourished outside the eurozone. Growth is currently running at 2.3 per cent, with Göran Persson, the prime minister, predicting last week that this figure will rise as high as 3.5 per cent in 2006. Yet inflation has remained muted, a fact attributed to the entry of low-cost food retailers and cheap Chinese imports, coupled with slow wage growth as workers focus on protecting their jobs. Underlying inflation is running at a tepid 0.8 per cent, with Mr Persson forecasting a rate of zero next year. This muted inflation data allowed the Riksbank to slash its repo rate by half a point to a record low of 1.5 per cent in June, lower even than rates available in the eurozone and encouraging carry trade players to borrow in krona and invest in higher-yielding jurisdictions elsewhere. Few analysts see any scope for the Riksbank to intervene to prop up its currency at present - a previous attempt to do so in 2001 proved spectacularly unsuccessful. carry trade = räntearbitrage

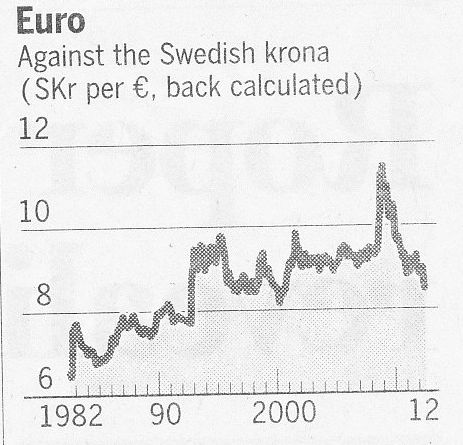

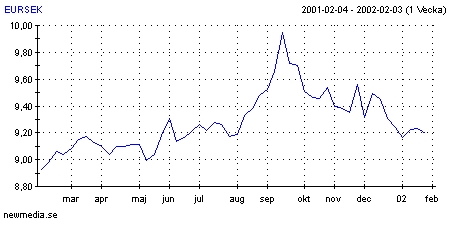

Kommentar av Rolf Englund: När euron infördes som elektronisk valuta den 1 januari 1999 sattes värdet till 9 kronor och 48 öre, om det nu är någon som minns det. Under 1999 föll kursen från 9,48 till 8,80 och 2000 verkar ha varit ett riktigt bottenår för euron som vara nere i 8,25 och vände. Sedan gick det raskt upp för euron och ner för kronan och euron var uppe i nästan 10 kronor 2001.

The European Central Bank is about to raise its interest rate for the first time in two and a half years. Does this move make any sense? Martin Wolf, FT 3/6 2005:

The ECB's monetary stance raises a number of questions: has it over- interpreted its price stability target? Is it chasing an arbitrary goal? Why is it so obsessed with government deficits? Why does it place so little emphasis on its other treaty obligation of supporting the European Union's economic policy? These are questions Europeans have not been, but should be, asking. Top The 12-country eurozone was hit on Tuesday by revelations that the economic situation in two of its weakest members, Italy and Portugal, could be even worse than feared. It is almost impossible to overstate the importance of the French referendum on the European constitution for the future of the European Union. Remember M3? Anybody? M3, a broad money supply measure watched closely by the ECB, grew at an annual rate of 6.4 per cent in February, down from 6.6 per cent in January. But the average rate of 6.5 per cent from December to February was up from 6.3 per cent in the three months to January. Unlike many other central banks, the ECB uses monetary aggregates as an important indicator of likely inflationary trends.

Kommentar av Rolf Englund: Kommentar 2: Kommentar 3: Det är just svårigheten, för att inte säga omöjligheten, att styra ekonomin med en ränta för hela området som gör EMU till en så korkad idé. Men idén med EMU är inte att det är bra för ekonomin, utan för att en gemensam valuta är en sak som en stat har, liksom flagga, domstol, parlament, försvar och konstitution. Jean-Claude Trichet, president of the European Central Bank, warned this month of “unsustainable price increases in property markets” that could result from excess liquidity and strong credit growth. What do the eurozone's national central banks do all day? Unsurprisingly lavish: France and Germany. Together, staffing at the Banque de France and the Bundesbank accounts for more than half the total. Leanest of the world's main central banks is that of China, with barely 2,200 employees. Russia, at the other end of the scale, has 37 times as many. The Bank of England can set interest rates with just 1,900 staff and no help from Frankfurt. Top Hervé Gaymard, France's new finance minister, on Thursday warned of a global "economic catastrophe" if the US, Europe and Asia did not work together to stem the decline of the dollar against the Euro. Trichet should not bemoan the rising euro The writer is a senior fellow at the Hoover Institution at Stanford University In his Frankfurt speech, the Fed chairman warned that at some point in the not too distant future the US dollar would have to decline because of the soaring US current account deficit. This sent the euro racing past the $1.30 mark, and Mr Trichet had egg on his face. Senior members of the ECB are furious with Mr Greenspan for his comments, which they regard as a "provocation". They are right. If anything, central bankers are supposed to moderate volatility in the foreign exchange markets, not increase it. The dollar was going down anyhow, so why grease the skids? In their view, the "double bubble man" was back, pumping up volatility. My advice to Europeans is simple: sit back, relax and enjoy the terms-of-trade gains from your currency's ascent. The soaring euro is not as negative for European growth as many assume because it means the ECB can postpone the higher interest rates it may have had in store. A higher euro, combined with lower interest rates than would otherwise be the case, does, however, affect Europe's pattern of production. It means a decrease in the production of tradeables - cars, for example - and an increase in the production of goods and services destined for domestic consumption. The euro's appreciation also demonstrates confidence in "Making the euro an international currency has to be way down the list of priorities for the ECB," said Robert Solomon, an economist with the Brookings Institution in Washington. "The benefits just aren't that great." The U.S. current-account deficit, of which the huge merchandise trade deficit is a key component, will shoot to over $500 billion this year. This demands capital inflows equal to the deficit, and a lower dollar promotes that, by making dollars cheaper for the rest of the world. Eventually, the lower dollar could also make American exports more competitive and begin to close the deficit. But to sell the dollar, traders need a place to put the proceeds, and that place, for the moment, is the euro. "What's happening to the euro is a reflection of the dollar," Solomon said. "It's not a euro phenomenon." EMU - Ett illa genomtänkt fullskaleexperiment If the dollar is not allowed to fall against the yuan, it will probably continue to fall heavily against something else. On Friday, the American currency fell to its weakest level against the yen since April 2000. It also remained around record lows against the euro. Earlier in the week, Nicolas Sarkozy, France’s finance minister, had declared that “the greenback has become unhinged”. The European Central Bank has not intervened directly on behalf of the euro for four years. It is unlikely to do so again without American backing. Japan’s monetary authorities have no such compunction. The finance ministry happily spent over ¥20 trillion ($170 billion) propping up the dollar last year and over ¥14 trillion in the first three months of this year. For Japan, unlike South Korea, buying dollars is profitable. And if it is also inflationary, so much the better for a country still gripped by deflation. Interest rates on American assets, such as Treasuries, may be low. But they are higher than the zero interest rates on offer in Japan. Moreover, printing yen to buy dollars is one way to inject liquidity into Japan’s moribund financial system. European leaders have openly blamed the US for the sharp rise in the value of the euro. Dollar at record low against euro More about the dollar at IntCom Consumer prices in the eurozone have soared by 2.5 per cent in the year to October The larger-than-expected rise, from an annual rate of 2.1 per cent in September, will add to the unease at the European Central Bank, which holds a rate-setting meeting next week. Although inflation has remained stubbornly higher than the ECB's target of “close to but below” 2 per cent, the eurozone's export-led recovery shows signs of losing momentum. Until 1998, members of the ERM effectively followed the policy set by Germany. While this was never ideal for the Netherlands, the European Central Bank's policy has turned out to be worse. There is a widely held view that the Dutch are unswervingly good Europeans, have a successful economy and are keen on economic reform - and that all this makes them a model for others to follow. The Dutch economy is in trouble. The Dutch public is hostile to economic reform. The Dutch have among the shortest working hours of all industrial nations and one of the lowest rates of productivity growth. Official unemployment is still low but the reality is masked by an extremely high proportion of part-time workers - not all voluntary - and a large number of people on disability allowances. Most ominously, the Dutch economy has become volatile since the introduction of the euro. The Netherlands' economic problems may in fact have had a negative impact on Dutch attitudes to Europe. The Dutch used to be among the most enthusiastic supporters of European integration. But recent opinion polls suggest a rise in euro-scepticism. The outcome of a forthcoming referendum on the European Constitution is not clear. In the 1980s and 1990s, the Dutch guilder was linked to the D-Mark through the European exchange rate mechanism. While the guilder was tied to the D-Mark in nominal terms, it managed to devalue in real terms because of persistently lower rates of inflation. One reason was the so-called Polder model - a celebrated deal between the government, employers and trade unions that guaranteed long periods of wage moderation. As this agreement gradually eroded, the Dutch lost that advantage. The other big factor is monetary policy. Until 1998, members of the ERM effectively followed the policy set by Germany. While this was never ideal for the Netherlands, the European Central Bank's policy has turned out to be worse. The ECB cannot be blamed for this - it sets policy for the eurozone as a whole - but from a purely Dutch perspective, the level of interest rates has been wrong almost all the time. One popular method to determine optimal interest rates is the so-called Taylor rule, which calculates the optimal short-term interest rate as a function of changes in inflation and the output gap - the percentage difference between the levels of actual and potential real gross domestic product. It suggests that the present European short-term interest rates of 2 per cent are right for the eurozone. But for the Netherlands, the correct rate is close to zero per cent. Because of relatively large trade exposure to the US, the Dutch economy has also been hit by the strong fluctuations in the euro's exchange rate against the dollar. Fiscal policy is constrained through the stability pact. With no effective macroeconomic tools left, the Dutch are aiming to improve their economic performance through structural reforms. But this has proved slow and unpopular, as it has elsewhere in Europe. Earlier this month, for example, 200,000 people took to the streets in Amsterdam to protest against some reforms. The story of the Netherlands and its economic downturn offers a convincing argument as to why the eurozone needs a common economic policy. The U.S. trade deficit widened

to a record $43.1 billion in January Eurostat: Inflation in the 12-nation zone slid to

an annual rate of 1.6 per cent in February While an interest rate

cut may seem the right medicine for Germany's ailing economy to Mr

Schröder in Berlin, the ECB in Frankfurt has to take account of conditions

in the euro area as a whole Although Mr Schröder said Europe and the US shared a common responsibility for the world economy, he knows that it is in the US's interest for the dollar to decline further to help cure the unsustainable US current account payments deficit. Co-ordinated currency intervention among the Group of Seven countries appears to be a non-starter, not least because of US hostility. Although one can sympathise with the German chancellor's hope that the ECB might be looking at the plight of Europe's exporters, he must also know that this would represent a significant shift away from its preoccupation with controlling inflation. While an interest rate cut may seem the right medicine for Germany's ailing economy to Mr Schröder in Berlin, the ECB in Frankfurt has to take account of conditions in the euro area as a whole. A case can be made for saying that the eurozone minus Germany has achieved respectable growth and job creation over the past decade. There are even suggestions that the ECB in its five years of operating monetary policy for the eurozone has been soft on inflation. --- Germany has been the EU's slowest-growing economy,

with an average annual growth rate of only 1.4%—roughly the same as that

achieved by feeble Japan over the same period. Over the past decade GDP per

head in the rest of the EU grew by an average of 2.3%—even faster than

America's 2.1% average growth. And though it is true that European labour

markets are in general less flexible than America's, Europe outside of Germany

has been creating just as many jobs as America. Over the past decade,

employment has risen by an average of only 0.2% a year in Germany, against a

rate of 1.3% a year in the rest of the EU, exactly the same pace of increase as

in America. Gerhard Schröder, warned

on Wednesday that the euro's current strength against the dollar was "not

satisfactory" and said he would raise the issue with President George W. Bush

in Washington this week While Mr Schröder stopped short of calling for any joint intervention to stabilise the euro-dollar exchange rate, he said the European Central Bank must be considering further action to lower interest rates in response to the continuing dollar decline. "The present dollar-euro exchange rate, at least for the Europeans, is not satisfactory," he said. "Only the central banks are in a position to change that, and I do not want to interfere in the policies of the US Federal Reserve. That is a matter for the Americans. "I would just say that I believe the European Central Bank has recognised that this relationship between the euro and the dollar is not helping the export sector, to put it very mildly. I can imagine that as a result, with all due respect for the independence of the ECB, there will be some consideration about whether [euro] interest rates are at the right level." Concerted action to influence exchange rates would contradict stated US policy. The US administration has consistently argued that open markets are the best judge of currency values. Though it agreed during the recent meeting of the Group of Seven rich countries to address European concerns about excess volatility in currency markets, the US thinking coming out of the meeting was that there was no change in the hands-off stance on the dollar. Dollar's threat to eurozone The eurozone economy grew by an insipid

0.4 per cent last year,- difficulties facing the struggling bloc as the euro

continues to strengthen. Official figures showed that the German economy, the eurozone's biggest, grew just 0.2 per cent quarter-on-quarter in the final three months of last year, but shrank by 0.1 per cent for the year as a whole. It was the first time the German economy had contracted since 1993. Meanwhile, the French economy, the eurozone's second largest, grew only 0.2 per cent in 2003, its worst performance in 10 years. The eurozone's expansion looked paltry compared to the 1 per cent growth recorded in the US during the fourth quarter, and Britain's growth rate of 0.9 per cent. The annual comparison looked even worse - the eurozone's 0.4 per cent growth for 2003 as a whole paled next to Britain's 2.1 per cent and an expected 3.1 in the US. Official figures showed that the German economy, the eurozone's biggest, grew just 0.2 per cent quarter-on-quarter in the final three months of last year, but shrank by 0.1 per cent for the year as a whole. It was the first time the German economy had contracted since 1993. Meanwhile, the French economy, the eurozone's second largest, grew only 0.2 per cent in 2003, its worst performance in 10 years. The US current account deficit,

currently at 5 per cent of gross domestic product, is now widely regarded as

unsustainable in the long run. On present evidence, the decline in the dollar's exchange rate so far is not sufficient for this process to continue at a meaningful pace. The question is therefore not so much whether the dollar should fall further, but by how much and against which currencies. While the steep rise in the

euro against the dollar is undeniably bad news for the eurozone, Europe's

fundamental problem is its failure to generate sustained growth in domestic

demand

Although some recent data from the US have disappointed, there can be no doubt that it is currently enjoying a robust recovery. But questions about the sustainability of that recovery persist. The current account deficit, expected to be about 5 per cent of US gross domestic product this year, looks like a potential source of turbulence for currency, equity and bond markets. The fall in the dollar should, in time, help to narrow that deficit. But a weaker currency can at best be only a partial solution. What the world really needs is for other economies to take up the slack in sustaining global demand. Siemens and Volkswagen are among the large manufacturers already warning about the hit to their profits from a rising euro. Michael Rogowski, head of the BDI, the German industry federation, says that the impact will be worse for smaller companies that cannot hedge their currency exposure. "The euro has reached a level where it is dangerous for many companies," he says. Oxford Economic Forecasting, a consultancy, believes that even with the euro averaging about $1.28, the eurozone could still grow by 1.7 per cent this year: hardly spectacular, but still the best performance since 2000. Fred Bergsten of the Institute for International Economics, a Washington-based think-tank, has been a long-standing advocate of a weaker dollar as a way to resolve the imbalance of the global economy. A rising euro against the dollar is not exactly what he wanted - he thinks China and other Asian countries should revalue - but he has little sympathy for European complaints. "I've had a lot of Europeans crying on my shoulder saying that the strong euro is going to ruin their economy, and I said to them: 'Not at all, it depends on what you're doing about domestic demand'," he says. Dollar's threat to eurozone The economic recovery in

continental Europe is "distinctly weak" and could easily be wrecked should the

euro continue to rise, OECD has warned. In contrast, growth in the United States should "remain very strong," said the OECD's chief economist, Jean-Philippe Cotis, at the World Economic Forum in Davos. Mr Cotis said the global economy found itself in a

very unusual situation. High growth in the United States and Asia was

"dangerously imbalanced" with the "distinctly weaker" European growth data.

"Paradoxically it is the weakest economy that sees its currency appreciating,"

Mr Cotis said. Svagare dollar är nyttig

medicin för EU Bara förra året blev euron 22 procent starkare mot den tidigare så hårda amerikanska valutan. Allt fler uttrycker oro för vad det betyder för den europeiska återhämtningen. Inte minst den tyske finansministern Eichel hoppades att Europeiska Centralbanken (ECB) skulle sänka räntan i torsdags, så att euron kunde tappa lite av sitt värde och därmed minska trycket på exportföretagen. Efter striden om stabilitetspakten är nu en konflikt om räntan och växelkursen under uppsegling. Men det var tacknämligt att ECB inte hörsammade önskemålet utan lämnade räntan oförändrad. Visst, möjligen skulle en räntesänkning ha fungerat som en lindring. Men bara i det korta perspektivet. Dessutom är det en typ av politik som vi har erfarenhet från i Sverige. Vi löste våra problem genom att justera värdet på vår krona. Någon sådan enkel utväg får EU-länderna inte erbjudas av centralbanken. De strukturreformer som krävs för att Europa ska kunna prestera bättre verkar behöva draghjälp utifrån. Fast det kan bara verka och fungera om det samtidigt inte ruckas på de institutionella ramverken. Därför vore det glädjande om kommissionen beslöt att domstolspröva euroländernas beslut att frångå stabilitetspakten. ECB har inget mål för valutakursen, utan ska i första hand sikta på prisstabilitet och därefter agera för att stärka tillväxten. Tillsammans med strikta regler för offentliga budgetsaldon kan detta driva fram strukturreformer som på sikt stärker Europas konkurrenskraft. Men åsidosätter finansministrarna restriktionerna och beviljar sig själva tillfällig lindring blir utmaningen svårare. En dyrare euro är kanske en besk medicin för tillfället, men på sikt kan det betyda mycket för Europas möjlighet att friskna till. RE: Full text av denna extremistiska ledare finns

på The euro hit another new high

against the dollar this week, above $1.28. The euro hit another new high against the dollar this week, above $1.28. That is almost 10% more than it bought in June 2003, when the European Central Bank (ECB) last cut interest rates, and over 50% above its low in 2001. A stronger currency will squeeze growth and inflation, just like a tightening of monetary policy—a reason, you might think, to cut interest rates. Yet the ECB held rates unchanged at its meeting this week. One reason is that although the euro has risen sharply against the dollar, in trade-weighted terms—ie, against a basket of the main currencies—its rise has been more modest, only 3% since June and 25% since 2001. That merely reverses its previous decline, taking its trade-weighted rate to the same level as at its launch five years ago. Indeed, it is also currently almost exactly at its average level over the past 20 years, using an index of its predecessor currencies before 1999.

Few have realised the most dangerous feature of Emu: Införandet av euron har

varit till skada för Italiens ekonomi och det hade varit bättre

för landet att stå utanför EU:s valutasamarbete, tycker

premiärminister Silvio Berlusconi. Införandet av euron har varit till skada

för Italiens ekonomi och det hade varit bättre för landet att

stå utanför EU:s valutasamarbete, tycker premiärminister Silvio

Berlusconi. I sin traditionella årsavslutande presskonferens i går

avslöjade han att han inte alls är nöjd med euroinförandet.

Han sade att "det har gått väldigt bra"

för de länder som behållit sina egna valutor - Sverige, Danmark

och Storbritannien. Italienska konsumentföreningar hävdar att valutabytet har kostat landets hushåll i genomsnitt 2 800 euro (25 000 kronor) i prishöjningar sedan januari 2002. TT-AFP There is, for the moment,

little evidence of stress in funding U.S. current account deficits. At the 21st Annual Monetary Conference, Cosponsored by the Cato Institute and The Economist, Washington, D.C. By the end of September 2003, net external claims on U.S. residents had risen to an estimated 25 percent of a year's GDP. To date, the widening to record levels of the U.S. ratio of current account deficit to GDP has been seemingly uneventful. But I have little doubt that, should it continue, at some point in the future adjustments will be set in motion that will eventually slow and presumably reverse the rate of accumulation of net claims on U.S. residents. In July 2001 one euro bought

just under 84 cents; this week it hit a new high of over $1.20. For America, it should be a boon, helping to boost exports, profits and jobs. The usual worry that a falling currency will lift inflation is also lessened, because America still has ample spare capacity and its inflation rate (1.3% on its core measure, excluding energy and food) is, if anything, too low. In Europe a weak dollar is feared and resented. Politicians and businessmen worry that America's gain will be their loss, and that their own firms will become less competitive as a result. And yet a rising euro need not be bad news for Europe. In fact, if the European Central Bank (ECB) responds in the correct way, it could be just the opposite: the kind of good news the euro area badly needs. Unfortunately, that is a big “if”, given the ECB's proven reluctance to reduce interest rates. And yet a stronger euro not only should make it easier for the ECB to cut rates while holding inflation down, it also should make such reductions imperative because the rise in the euro itself is equivalent to a tightening of monetary conditions. Although manufacturers may be hurt in the short term by the euro's rise, the euro area's economy as a whole should benefit. A stronger exchange rate improves any economy's terms of trade, and so boosts consumers' spending power: they can buy more foreign goods in exchange for the same amount of domestic production. Lower interest rates will also, at last, boost Europe's feeble domestic demand, which has long been a big drag on euro-area economies. Finally, a stronger euro should force politicians and firms in Europe to pursue the kind of painful but necessary structural reforms which they have long talked about, but resisted making. Faced with a rising currency and a slowing

global economy, Investors are focused on the US's ever-widening current account deficit: a shortfall that requires $1.5bn a day of foreign capital to finance it. Those investors are unlikely to be attracted by US yields; short-term interest rates are just 1 per cent (and negative in real terms) and the US 10-year Treasury bond yields a few basis points less than its German equivalent. And once a currency slide begins, the incentives to hold it rapidly reduce. For a European investor, this year's 21.5 per cent rise in the US equity market translates into just a 5.6 per cent gain in euro terms, 25 percentage points behind the return from the German market. Fortunately for the US, there are still some willing financiers of its current account deficit: the Asian central banks. They are keen to keep their currencies steady against the dollar so as to give their exporters a competitive boost. US demand keeps their factories busy. So they are happy to act rather like bourgeois merchants supplying the Victorian aristocracy - exchanging their goods for eventual promises to pay. At some stage, after their holdings of Treasury bonds have fallen sharply in value, the deal may start to pall but that stage may be years away. The Asian reluctance to let currencies appreciate against the dollar puts more of the adjustment burden on the eurozone and on peripheral currencies such as sterling and the Australian dollar. In theory, that should allow the European Central Bank to cut interest rates. Such a move would head off the deflationary impact of a rising euro and play its part in rebalancing the global economy, reducing dependence on US domestic demand. In practice, however, the ECB may be unwilling to play this role. It is already aggrieved at the failure of France and Germany to stick to the deficit terms of the stability and growth pact. And it seems to feel that the US current account deficit, being the result of US profligacy, is not Europe's problem to deal with. But it is not difficult to see where this delicate balancing act could go wrong. The Chinese economy could overheat, slowing the growth in global trade. Private investor reluctance to own US assets could push up Treasury bond yields, thereby applying the brakes to the US recovery. Faced with a rising currency and a slowing global economy, Europe could be caught in a very nasty squeeze. Can the EMU persist and

prosper without political union? If political union is unrealistic, what is the

future of the euro? Den svenska kronan stärktes ytterligare

på torsdagsmorgonen.En euro kostar nu runt 9 kronor, den lägsta

nivån hittills i år. Den kronförsvagning alla räknat med

efter Sveriges nej till EMU har i stället förvandlats till en

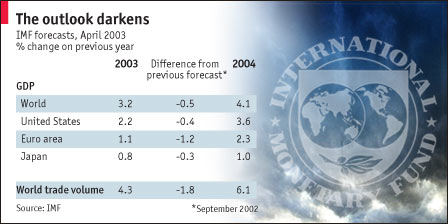

kronförstärkning. IMF growth projections for 2003 Big Lies about Central

Banking Joseph E. Stiglitz, a Nobel laureate in economics, is Professor of Economics at Columbia University and was Chairman of the Council of Economic Advisers to President Clinton and Chief Economist and Senior Vice President at the World Bank. An independent central bank focused exclusively on price stability has become a central part of the mantra of "economic reform." Like so many other policy maxims, it has been repeated often enough that it has come to be believed. But bold assertions, even from central bankers, are no substitute for research and analysis. Research suggests that if central banks focus on inflation, they do a better job at controlling inflation. But controlling inflation is not an end in itself: it is merely a means of achieving faster, more stable growth, with lower unemployment. Some argue that in the long run there are no tradeoffs. But, as Keynes said, in the long run, we are all dead. Even if it were impossible to lower unemployment below some critical level without fuelling inflation, there is uncertainty about what that critical level is. Accordingly, risk is unavoidable: monetary policy that is too loose risks inflation; if it is too tight, it can cause unnecessary unemployment, with all the suffering that follows. But that is not the point: the point is that no one could be sure. A calculated risk is always unavoidable. Who bears it varies with different policies, and that is a decision that cannot--or at least should not--be left to central bank technocrats. While there is a legitimate debate about the degree of independence accorded to central banks and other decision-making bodies, within a democracy, the perspectives of those whose well-being is affected by the decisions taken should be represented in the process. A focus on inflation may make sense for countries with long histories of inflation, but not for others, like Japan. America's central bank, the Federal Reserve, is mandated not only to ensure price stability, but also to promote growth and full employment. There is broad consensus in the US against a narrow mandate, such as that of the European Central Bank. Today, Europe's growth languishes, because the ECB is constrained by its single-minded focus on inflation from promoting economic recovery. Technocrats and financial market players who benefit from this institutional arrangement have done an impressive job of convincing many countries of its virtues, and of the need to treat monetary policy as a technical matter that should be put above politics. The euro has hit four-month lows against

the dollar, as dismal European economic data contrasts with optimism in the

United States. The European single currency traded below $1.11 for the first time since April, as traders swapped their money into dollars in response to a buoyant US stock market. The euro has lost 7% of its value against the dollar since June, partially reversing a sustained 33% increase since early last year. Den svenska kronan kommer att bli starkare

om Sverige röstar nej till EMU Den svenska kronan kommer att bli starkare om Sverige röstar nej till EMU den 14 september. Det säger Steve Barrow, valutaanalytiker på investmentbanken Bear Stearns i London. Andra analytiker är inte lika optimistiska, men de tror inte på någon drastisk försvagning av kronan i händelse av ett nej. Däremot råder en del osäkerhet om de politiska konsekvenserna. På Bear Stearns är man övertygad om att den svenska kronan skulle bli starkare utanför EMU. "Det bästa som kunde hända er valuta vore om ni röstade nej till euron", säger Steve Barrow. "Det kanske inte låter självklart, men det är logiskt med tanke på att eurozonen börjar likna en katastrofzon, samtidigt som länderna utanför gör bättre ifrån sig ekonomiskt." "Det finns goda argument för att kronan ska stärkas, men det blir ingen reflexrörelse på valutamarknaden vid ett nej. På lite längre sikt räknar vi däremot med att euron skulle sjunka ned mot 8,28-8,50 kronor." De senaste dagarna har euron pendlat kring 9,20 kronor. Går Sverige med i valutaunionen väntas valutabytet ske till en kurs på 9,00 kronor per euro. Den amerikanska investmentbanken Merrill Lynch råder sina kunder att köpa svensk valuta redan nu. "Svenska kronor är en ganska säker placering just nu", säger bankens valutastrateg Alex Patelis. Enligt Danske Bank är världens finansmarknader redan inställda på ett nej. Sannolikheten att svenskarna röstar ja är så låg som 3 procent, enligt bankens analys av prissättningen på valuta- och räntederivat. "O ja, marknaden tror på ett nej", säger Klas Eklund, chefsekonom på SEB. I händelse av ett nederlag för regeringen Persson i folkomröstningen väntas effekterna på räntor och valutakurser bli begränsade. Däremot finns det en del osäkerhet om de politiska konsekvenserna. En viss politisk riskpremie i form av högre ränta på svenska statspapper kan vara motiverad, enligt SEB:s chefsekonom. OECD: Sveriges

förutsättningar bättre än euroländernas Sverige har bättre förutsättningar för tillväxt än euroländerna. Det gäller allt från byråkratiska hinder för nyföretagande till antalet patent i utlandet. Den årliga tillväxten per invånare blir 2,25 procent i Sverige och 2,0 procent i euroområdet 2003-2008. Med hänsyn till vad som är långsiktigt hållbart är dock Sveriges tillväxt 0,5 procentenheter högre än euroländernas, eftersom valutaunionens ekonomi är tillfälligt uppblåst under perioden. Den bedömningen gör västländernas samarbetsorganisation OECD i en färsk rapport. OECD skriver att euroländerna lider av stora stelheter i sina ekonomier, vilket försämrar möjligheterna till långsiktig tillväxt. Inte minst ses den höga strukturella arbetslösheten (som är oberoende av konjunkturen) på cirka 8 procent som ett problem för euroområdet. För att komma till rätta med den krävs enligt OECD en mer flexibel arbetsmarknad. I Sverige är anställningstryggheten något lägre än den är inom EMU. Å andra sidan är ersättningen till arbetslösa samt skatten på arbete högre i Sverige än inom EMU. Enligt Padoa-Schioppa, som

är ledamot i Europeiska centralbankens direktion, är det inte

märkvärdigare att ECB sätter samma ränta för hela

euroområdet än att tyska Bundesbank tidigare gjorde det för

hela Tyskland, med deras stora regionala skillnader. Svenskar, liksom andra européer, är präglade av sin egen historia. I Sveriges dystra erfarenheter från 1990-talets början ligger en finanskris som krävde extraordinära åtgärder från statens och Riksbankens sida. Hur skulle ECB hantera en sådan situation? - Något liknande den svenska bankkrisen, som omfattade hela branschen, är helt osannolikt i euroområdet. Under normala förhållanden ska de nationella myndigheterna sköta övervakningen av bankerna och vid behov kunna ingripa. De flesta kriser gäller enstaka banker, som övertas av andra eller läggs ned. Det måste dock finnas en beredskap även för svårare situationer, där hela det finansiella systemet hamnar i gungning, medger Tommaso Padoa-Schioppa. I första hand är det en uppgift för de nationella centralbankerna, men vid större insatser skulle även ECB-systemet med alla euroländernas centralbanker dras in. Exakt vilket ansvar som ECB skulle ta i en sådan situation klargörs inte av Tommaso Padoa-Schioppa, som förklarar att det knappast är möjligt att ha en helt förberedd lösning på hittills obekanta problem. Riksbankens officiella

valutakorg, TCW-index är missvisande Den svenska kronan slog bottenrekord i september 2001, när världens finansmarknader fortfarande skakade efter terrordåden i New York och Washington. Sedan dess har den svenska valutan sakta återhämtat sig. Kronan har till exempel stärkts med nästan 40 procent mot USA-dollarn. Mot Riksbankens officiella valutakorg, TCW-index, har kronan stärkts med 15 procent sedan bottennoteringen. I TCW-korgen (Total Competitiveness Weights) ingår tio olika valutor. De har viktats efter hur mycket de påverkar svensk utrikeshandel och konkurrenskraft. Men detta index är ändå missvisande eftersom flera av Sveriges viktigaste handelspartner inte finns med. Korgen innehåller till exempel inga asiatiska valutor (utöver den japanska yenen) trots att Sverige har en mycket omfattande handel med de asiatiska länderna: den svenska exporten till Kina är tolv gånger större än exporten till Nya Zeeland, vars valuta finns med i TCW-index. Dollarn har större betydelse för svensk industri än vad som framgår av TCW-index eftersom flera andra länder i Asien och Latinamerika har valutor som nära följer dollarkursen. För att få ett mer rättvisande mått på kronans utveckling, har vi i stället använt en alternativ valutakorg, MERM-index (Multilateral Exchange Rate Model, som tar hänsyn även till andra varor än industrivaror). Den består till mer än en fjärdedel av dollar. Mot denna korg har kronan stärkts med över 20 procent sedan bottennoteringen. Kursen är därmed tillbaka på samma nivå som vårvintern 2000, då Stockholmsbörsen stod som högst och högkonjunkturen var som hetast. Europe's single currency, the euro, has surged against the US

dollar and The euro has gained sharply against the US dollar,

reaching a new four-year high of $1.1067 The Economist 6/2

2003 Cocooned in its Frankfurt tower block, the ECB’s governing council remains reluctant to accept that the bank has a role to play in fostering growth in the sluggish euro area. The bank’s inflation target—2% or lower—is, claim its policymakers, the sole determinant of interest-rate policy. In practice, the ECB has more than once trimmed borrowing costs when inflation was above target, but it has provided often-convoluted explanations which seek to demonstrate the theological consistency of its behaviour. Ja-sidan: Kronan nådde på

tisdagen 7/1 sin starkaste nivå sedan början av 2001.

Stefan Fölster:

Svenskt Näringsliv förordar ingen Om Sverige röstar ja till EMU, betyder det att kronan kommer att knytas till euron vid en svagare nivå än vad marknaden hittills räknat med. När euron så småningom ersätter kronan sker konverteringen till kursen 9 kronor för en euro. Det spår Svenskt Näringsliv i sin senaste konjunkturprognos. Svenska exportföretag får fler kronor för varje euro de tjänar ju svagare knytkursen är, men Stefan Fölster betonar att det handlar om en prognos och inte om en partsinlaga. "Svenskt Näringsliv förordar ingen särskild knytkurs för kronan", säger han. "Vi tror mest på en marknadsbestämd kurs. Det är bättre än att ha någon politiskt eller administrativt frampressad kurs." "Rätt kronkurs 8,90 kr" Finansoro bakom kronans

styrka För egen del kommer jag att rösta ja

utan övertro på att enbart euron löser några av Sveriges

grundläggande problem. Utom det som illustreras av diagrammet: den svenska

kronans stadiga fall i värde över decennierna.

Den svenska kronan ligger åtta på listan med en förstärkning på 18 procent, efter en kontinuerlig uppgång under hösten. En drivande faktor har varit spekulationer om att Sverige kommer att gå in i valutaunionen EMU. Vid ett svenskt medlemskap kommer kronan sannolikt att knytas till euron till en kurs runt 8,60-8,70. Valutahandlarna har därför inte velat köpa kronor till en kurs alltför långt ifrån den väntade anslutningskursen. Robert Bergqvist, ränte- och valutaexpert på SE-banken

oroar sig inte för vad partiledarna kommer fram till, eller inte kommer

fram till. Ett stopp i EMU-processen skulle inte ge

någon anledning till The price of a falling dollar European Union leaders have confidently declared

the region's economic slowdown is over. Eurozone underlying inflation

rises in May ECB may raise rates after

inflation revised up “Haveri för Europeiska

centralbanken (ECB)” Ett stopp i EMU-processen skulle

inte ge någon anledning till Sett till prissättningen så är det nästan ingen på marknaden som tror att vi är med i EMU den 1 januari 2005. Konvergenspositionerna är inte av en omfattning att de, vid en avveckling, skulle flytta kronan till avsevärt högre nivåer. Därför skulle ett stopp i EMU-processen inte ge någon anledning till oro för hur det skulle slå mot kronan och på finansmarknaderna. Samtidigt är svenska fundamenta starka i ett internationellt perspektiv, med stora överskott i handels- och bytesbalanserna. Statsfinanserna är också relativt starka jämfört med omvärlden. En viss återhämtning i ekonomin framöver borde också kunna stärka riskaptiten och därigenom ge draghjälp år kronan. The price of a falling dollar What makes the negative impact more plausible is the extent of the recent dependence on external demand. In the year to the first quarter of 2002, the eurozone economy expanded by only 0.1 per cent. The contribution of domestic demand was minus 0.7 percentage points, offset by a positive contribution from net trade of 0.8 percentage points. It is astonishing that so large an economic area should have been

this dependent on external demand. A strong appreciation would combine with low productivity growth to generate a squeeze on profitability in the internationally exposed sectors of the economy. That is likely to undermine investment. In addition, low productivity growth is a partial explanation for the persistently weak growth of private consumption in the eurozone, particularly in Germany. This is a clash of the pygmies: a huge capital requirement and weak asset prices in the US against a miserable productivity record and sluggish domestic demand in the eurozone. The worry must be that US adjustment is reinforced, not offset, by the eurozone's response. The proponents of the euro wanted their currency and their zone to play a bigger role. They have their wish. We shall soon know whether they know what to do with it. Few have realised the

most dangerous feature of Emu: Euron spricker

när dollarn faller Eurozone underlying

inflation rises in May This brings the rate within the ECB's 0 to 2 per cent target range for the first time this year. But excluding energy, food, alcohol and tobacco, whose prices are highly volatile and often give little indication of longer-term inflationary trends, inflation rose from 2.4 to 2.6 per cent. Inflation was highest in Ireland, at 5 per cent, and also far above the overall eurozone target ceiling in Spain, Portugal, Greece and the Netherlands. By the same measure - the so-called "harmonised index of consumer prices" - figures published on Tuesday showed inflation in the UK at only 0.8 per cent. The ECB faces a painful dilemma: whether to raise interest rates soon to prevent a further build-up in inflationary pressure, or whether to keep rates low while it waits for economic recovery to become more entrenched. ECB

may raise rates after inflation revised up The official estimate of eurozone inflation has been revised up, underlining the significant deterioration in the bloc's economic outlook and prompting speculation the European Central Bank could raise interest rates as soon as next month. The upward revision of the eurozone's April inflation numbers comes on the heels of a slew of disappointing data this week, which were at odds with previous rosy predictions that inflation was set to head steadily downwards. Eurostat, the EU statistical agency, said on Thursday that eurozone consumer prices rose by 2.4 per cent in the year to April - significantly more than its earlier estimate of a 2.2 per cent increase. Inflation was highest in Ireland, at 5 per cent, and lowest in Germany and Austria, at 1.6 per cent. The refusal of inflation to fall below the ECB's 2 per cent target ceiling presents a dilemma for the central bank. Inflationstakten ökade oväntat

Under de närmaste månaderna väntas en

förbättrad konjunktur, flöden, stigande börskurser och

ökad riskaptit medverka till att gynna kronan, som på tre

månaders sikt väntas ha stärkts till 8:85 mot euron. Europes economy - March

14, 2002

At last year's EU summit in Stockholm, France's prime minister, Lionel Jospin, confidently predicted that GDP growth in the EU would be a healthy 3% in 2001, the same as in 2000. Since then, though, Europe's economies have stumbled. In the Netherlands, where electors go to the polls in May, GDP was flat in the last two quarters of last year. In France, growth slipped to 2% in 2001 after averaging over 3% in the three previous years (see chart 1). The French economy actually contracted in the fourth quarter, for the first time in five years. Europe's sickliest economy, though, is its biggest, Germany. In the first half of 2000, the country seemed to have at last shaken off years of torpor. Yet in the middle of that year it stalled, and it has struggled ever since, shrinking in the third and fourth quarters of 2001. Last year, German GDP grew by a measly 0.6%, the lowest rate in the EU. Between them, France and Germany account for more than half the output of the 12-member euro area (the EU countries that have adopted a common currency). Add Italy (whose GDP also fell at the end of 2001, but where no election is due this year), and the proportion rises to 70%. Not surprisingly, the whole region's GDP slid by 0.2% in the last quarter of 2001, the first drop for almost nine years. Happy Days are here again, at least for

now Whatever the Treasury may say in the report on “economic convergence” due to be issued just before a referendum, the British and euroland economies will be about as convergent in the year ahead as an Aston Martin and a Daimler-Benz truck. Indeed, it is hard to think of any time since the ill-fated ERM experiment, when the economic cycles of Britain and the Continent have been more out of sync. While today’s euro interest rate, at 3.25 per cent, may not seem very far from the British level, there is a strong possibility that the European Central Bank will ease at least one more time, to below 3 per cent. After all, there is something strange about a monetary policy that keeps interest rates much higher in the present slump than it did in the boom of 1999, when European interest rates were set at 2.5 per cent. Thus the gap between British and euro interest rates is almost certain to widen in the year ahead, but this gap vastly understates the true monetary divergence between Britain and the eurozone. Most British businessmen — and all those who favour the euro — believe that the pound is substantially “overvalued” and that Britain would be mad to join the euro unless we could first devalue by at least 10 per cent. If a referendum campaign were launched, currency markets would immediately start to anticipate this decline. There would be wild speculation, reminiscent of the ill-fated period before ERM entry in 1990. The most likely result would be a sharp fall in sterling and a dramatic increase in British inflation — even before the referendum was held. The economic forecasters’ rule of thumb is that a 10 per cent fall in the exchange rate is roughly equivalent in its inflationary impact to a change in interest rates of between 2 and 3 percentage points. Thus if sterling were to join the euro at an exchange rate 10 per cent below today’s level — implying an entry rate very close to the old ERM central parity of DM2.95 to the pound — British interest rates would have to rise to between 6 per cent and 7 per cent. And that would merely maintain the present level of monetary rigour in the British economy. Once we allow for the additional inflationary pressures building up in the year ahead, as the world economy recovers, British interest rates would have to rise as high as 8 per cent or 9 per cent. One obvious alternative to such a savage monetary tightening — which would probably trigger an ERM- style negative equity disaster in the housing market — would be either to raise taxes or to slash public spending. To offset the inflationary impact of a 10 per cent sterling devaluation, the scale of the fiscal tightening would have to be much bigger than the £11 billion in public spending cuts suggested by the European Commission as the price that Britain ought to pay for joining the eurozone. It seems unlikely that Mr Blair would propose a 5p increase in the standard rate of tax or a 20 per cent reduction in health and education spending in his euro-referendum package. Soros: "impossible" for Britain to reject adoption of the euro

Billionaire investment guru George Soros has said that it is "impossible" for Britain to reject adoption of the euro. Mr Soros, whose currency investments have earned him a formidable reputation, warned that there were still concerns over Europe's single currency. Harmonisation of taxes among EU states was needed to support a euro which was still "a work in progress", Mr Soros told GMTV's The Sunday Programme. "It's a quandary because it's dangerous to move in and particularly at what exchange rate and so on, on the other hand it's impossible to stay out," he said. MARKNADEN: KRONAN KNYTS TILL 8,75 MOT EURON Kronan kommer att stärkas med 30 öre gentemot euron de närmaste två åren. Det är marknadens genomsnittliga bedömning, enligt Prosperas senaste undersökning. Detta innebär att kronan knyts till en kurs på runt 8,75 i växelkurssamarbetet ERM2 inför ett svenskt EMU-medlemskap. Bakom marknadens optimism ligger kronans uppsving och ökade utsikter för ett svenskt EMU-inträde. Statsminister Göran Perssons teoretiska tidtabell för ett svenskt EMU-medlemskap innebär att en folkomröstning om euron hålls våren 2001, inträdet i ERM sker senast februari 2004 och Sverige ansluts till EMU 1 januari 2005. Lås kronan mot

euron Replik: Låt

kronan flyta vidare RE: För andra åsikter, se t ex Kaletysky och Sorors Styrelseordförande i Svenska Handelskammaren i Tyskland är Lars Törnquist, styrelseledamot i SEB Tyskland SEB ingår som bekant i Wallenbergssfären och har Klas Eklund som chefekonom. Handelskammaren samarbetar även med Exportrådet, som har en VD som heter Ulf Dinkelspiel, och med Direktör Anders Narvinger ABB Financial Services AB i ledningen för styrelsen. RE: För en annan artikel på samma tema,

se Inga genvägar till

euron I dag bestäms kronans värde av marknaden. Går Sverige med i EMU blir det ett politiskt beslut att fastställa växelkursen till euron. Att Svenskt Näringsliv redan nu ropar efter en svag krona i stället för lägre skatter och reformer av den svenska ekonomin, tyder på att organisationen inte vet vem eller vad man finns till för. Långt kvar till stärkt "Europapeng" Nyåret 1998-99 startade EMU. Då kostade en euro 9 kronor och 56 öre. Vid årsskiftet tre år senare - när euron blev praktisk verklighet i form av sedlar och mynt för Eurolands 310 miljoner medborgare - hade kursen fallit till 9:23 kronor. Och kräftgången fortsatt sedan dess. På torsdagen pendlade eurokursen runt 9:07 kronor. Introduktionen av "Europapengen" har alltså inte blivit någon knuff i ryggen för den nya valutan. Den har fortsatt att tappa mark även mot dollarn: Från 1:18 dollar per euro vid årsskiftet 1998-99 till 0:86 dollar/euro i dag. Det motsvarar en "devalvering" på drygt 25 procent. Bo Lundgren Vi moderater vill föra en politik med målsättningen att svensk ekonomi i sig är så stark att vår köpkraft och vår valuta (så länge vi står utanför euron) stärks. Mer än några

kronor Handelsbankens ekonomer om svenskt

EMU-medlemskap "Rätt

kronkurs 8,90 kr" SEB räknar med att kronan stärks till 9,00 mot euron och till 10,60 mot dollarn på tre månaders sikt. DI 2001-11-23 Hamburgerkursen visar kronans verkliga värde Nästa år ska vi troligen folkomrösta om att avskaffa den svenska kronan och ersätta den med euron. Då uppstår genast frågan till vilken kurs växlingen ska göras. Helst ska det ske på en "lagom" nivå. Kronan får varken vara för svag eller för stark, varken undervärderad eller övervärderad. Men vad som är lagom råder det delade meningar om. Experterna på Riksbanken säger en sak, experterna i näringslivet en annan. De senaste veckorna har kursen pendlat mellan 9,00 och 9,50 kronor per euro. De flesta bedömare är överens om att kronan måste knytas till en starkare kurs än så. Men den kan knappast bli lika stark som den var för tio år sedan, då Sverige upprätthöll en fast växelkurs på 7,40 kronor mot eurons föregångare, ecun. Medelgissningen är att knytkursen hamnar någonstans mellan 8 och 9 kronor per euro. För att bedöma vad som kan tänkas vara en lämplig nivå, har ekonomerna ansträngt sig för att räkna ut kronans långsiktiga "jämviktsväxelkurs" mot euron. Pionjärarbetet gjordes av riksbanksekonomerna Annika Alexius och Hans Lindberg 1996. De utgick från att en "real jämviktsväxelkurs" för kronan är en som är förenlig med intern och extern balans i ekonomin. Vid intern balans råder full sysselsättning och stabila priser. Extern balans förutsätter att utlandsskulden inte växer under okontrollerade former. Dessvärre ser det ut att behövas olika växelkurser vid olika tidpunkter för att ekonomin ska hålla balansen. kurs här Annika Alexius och Hans Lindberg kom fram till att kronans jämviktsväxelkurs för 1996 borde ligga kring 114. Detta mätt mot Riksbankens valutaindex TCW, där de viktigaste konkurrentländernas valutor ingår. Vid dåvarande växelkurs skulle det motsvara 8,40 kronor per euro. Förra året gjorde ekonomerna på Svenskt

Näringsliv (SN) en beräkning med samma metod. De kom fram till att

jämviktskursen för 2001 låg vid 9,10 kronor per euro.

Det intressanta är att kronans faktiska växelkurs - som bestäms helt av marknadskrafterna - verkar ha anpassats rätt väl till den teoretiska jämviktskursen. Det tyder på att valutamarknaden är ganska bra på att hålla svensk ekonomi i intern och extern balans. En alternativ metod att räkna ut kronans rätta värde är att använda tidningen The Economists berömda Big Mac-index. Vid jämvikt ska en hamburgare kosta lika mycket här som i Hamburg. I Economists senaste mätning kostade en svensk Big Mac 2,63 euro. Om det är dyrt eller billigt i europeisk jämförelse är dessvärre svårt att avgöra, eftersom priserna skiljer sig åt i olika delar av eurozonen. Enligt det senaste Big Mac-indexet får man punga ut med 2,82 euro för en fransk burgare medan det räcker med 2,21 för en italiensk. Asymmetriska chocker - ett hinder för

svenskt medlemskap i EMU? http://tuth.ne.su.se/ed/pdf/24-3-jh.pdf EU-kommissionen:

Snart vänder det The eurozone economy may have shrunk during the last three months of 2001, but it is due for a rapid rebound, the European Commission has calculated. Growth in gross domestic product (GDP) across the 12-member eurozone over the October to December period is likely to have fallen within the range of minus 0.3% to plus 0.1%, the commission's new economic forecasting model has estimated. Weaker yen, stronger euro The writer is head of strategy and economic research at Societe Generale Asset Management in Paris The yen fell nearly 10 per cent during the last two months of 2001 and is now back down in the 130s against the US dollar for the first time since 1998. Japanese and US authorities appear to have jointly encouraged this slide. Tokyo says it reflects economic fundamentals; Washington hints that it favours broader monetary expansion through purchases of US Treasuries. Regrettably, the role that the euro could play in a more co-ordinated currency adjustment has been neglected. The weaker yen policy is doomed to fail if its impact on the currencies of its main trade partners, the US and the rest of Asia, is not offset by a stronger euro.

Handelsbankens ekonomer om svenskt

EMU-medlemskap Om Sverige går med i EMU kommer vi att få högre inflation i stället för starkare krona. Det spår Handelsbankens ekonomiska sekretariat i en ny studie. Själv räknar banken med att väljarna röstar ja till valutaunionen nästa år. Därefter väntas kronan knytas till euron vid en kurs på 8,50 kronor/euro. Men att kronan försvinner betyder inte att inflationen gör det. Tvärtom, Handelsbanken räknar med att Sverige får högre inflation med euron. Orsaken är att Sveriges ekonomi väntas växa snabbare än EU-genomsnittet de kommande åren. Detta leder till “real appreciering”, det vill säga att svenska priser och löner stiger relativt övriga EU-länders. Om vi står utanför EMU kommer denna appreciering att ske genom att kronan stärks på eurons bekostnad. Går vi med kommer den i stället att ske genom att inflationen blir högre här än i eurozonen. “Sverige har bättre tillväxtförutsättningar än EU-genomsnittet, vilket talar för att Sverige får en högre inflation än EU-genomsnittet”, säger Jan Häggström, chefsekonom på Handelsbanken. Att Sverige skulle behöva särskilda så kallade buffertfonder av finsk modell för att utjämna svängningar i konjunkturen tror inte ekonomerna på Handelsbanken. Inte heller är det nödvändigt att skapa en buffert med hjälp av extra strama budgetmål. Istället borde de förbättrade statsfinanserna användas för att sänka skatterna, menar Handelsbanken. Mer än några

kronor Ökat stöd

för EMU EMU gör dollarn billigare Hade Sverige gått med i EMU från början skulle dollarn aldrig ha stigit över 11 kronor. Men vi hade inte kunnat hindra den från att stiga över 10,50. Det visar en beräkning som Dagens Industri har gjort. Beräkningarna visar att kronans kurs mot dollarn, yenen och andra icke-europeiska valutor inte hade sett särskilt mycket annorlunda ut om Sverige hade deltagit i valutaunionen från starten 1999. Euro-dollar reaches three-month

The euro scraped briefly above $0.90 in London trading on Monday, in its first foray above the important psychological barrier since early May. At the end of London trading it remained tantalisingly near, trading almost half a cent above Friday's closing price at $0.899 as traders continued to digest the sobering news in Friday's US Fed Beige Book. Svenska Dagbladet 2001-07-26 om Gunnar Hökmarks

odödliga tankar: Om det inte vore för att många tecken tyder på att konjunkturnedgången har kommit för att stanna ytterligare en tid. - Tiderna är dåliga, det är alla överens om. En oförskämt stark dollar nämns i många kommentarer och analyser som en av orsakerna till problemen. Men det verkliga problemet är snarare att kronan är för svag - eller rättare sagt att den svenska regeringens politik är för svag, vilket avspeglar sig i ett lågt förtroende för kronan. Mer av Svenska Dagbladet om EMU Finanstidningen 2001-07-26 - Det är ett

elände med den svenska kronan. Att den förlorat stort i

förhållande till dollarn är en sak. Sverige behöver EMU!

Europe Must Reverse The Euro's Slide

"Perssons fel att kronan

försvagas" Regeringen bär ansvaret för att kronan försvagas. Det hävdar moderaterna i en ny rapport, där partiet anklagar regeringen Persson för att bedriva flytande devalveringspolitik. "Begreppet Perssonpengar håller på att få en ny innebörd", sa Gunnar Hökmark, moderaternas representant i riksdagens finansutskott, vid en pressträff på torsdagen. Moderaterna uppmanar regeringen att vidta snabba åtgärder för att stärka kronan, till exempel att slopa förmögenhetsskatten liksom dubbelbeskattningen på aktieutdelningar. "Det lättaste vore att ge besked i eurofrågan och tala om när vi ska folkomrösta, det skulle ge stadga åt kronan", säger Gunnar Hökmark och uppmanar Göran Persson att följa sin brittiske kollega Tony Blair, som lovat en folkomröstning om EMU inom två år efter torsdagens parlamentsval. Vilka hoppas du vinner det brittiska valet egentligen? "Jag tycker inte att de konservativa gjort sig förtjänta av en valseger", svarar Gunnar Hökmark. Han vill inte svara på vad som kan vara en lämplig konverteringskurs när det är dags att byta kronan mot euron. "Prognoserna måste rimligtvis revideras ned med hänsyn till kronans försvagning det senaste året", säger han. "Men det vore bra om vi kunde förhandla utan att fixera oss vid ett antal rimlighetsvärden." Kronfallet är

ingen valutakris Den stabila euron IMF: One World -

one Currency? Most popular explanations for the euro’s decline do not

stack up Most popular explanations for the euro’s decline do not stack up. Some argue that the euro’s weakness reflects the American economy’s faster growth rate. That gap may now have almost closed, which could explain why the euro has recovered slightly over the past couple of weeks. But the “growth-gap” explanation does not fully explain exchange-rate movements. The Australian dollar, for instance, has plunged by almost as much as the euro against the greenback, and yet Australia’s growth rate has roughly matched America’s in recent years. A lot of the American dollar’s strength has nothing to do with relative growth rates. A second favoured explanation for the euro’s weakness is that labour- and product-market rigidities in Europe discourage investment. Europe’s overtaxed and overly regulated economies are certainly more arthritic than America’s. But that was also true two years ago when the euro was more than 30% above its current value. Europe’s economic rigidities have not got worse relative to America’s over the past two years: on the contrary, European economies have become more flexible far faster than most observers had expected. This should have favoured rather than hurt the euro. In fact, the euro, by creating a single, more liquid capital market, has spurred corporate restructuring across Europe, as managers have been forced to pay more attention to shareholder value. Labour markets are also becoming more flexible, as a loosening of the rules has made it easier for firms to hire workers on part-time or fixed-term contracts, with less job protection and lower social-security taxes. Across the euro area, tax rates are being trimmed and wage bargaining is becoming more decentralised. None of this is to deny that more reforms are needed - but investors and the markets have been wrong to assume that Europe can never change. The third culprit often identified by the markets is the ECB itself, for lacking clarity in its policy goals and lacking transparency in its decision-making. Really? The ECB has been poor at communicating with the outside world, and its president, Wim Duisenberg, seems decidedly gaffe-prone; but charges of a lack of transparency and clarity apply more to the Fed than to the ECB. Unlike the ECB, for instance, the Fed lacks a clearly defined inflation goal, and at times Alan Greenspan is far from transparent, being a master of obfuscatory language. He gets away with it, because the markets think he can do no wrong. What is curious about much commentary on the relative merits of the euro and the dollar is that all of America’s economic strengths are pitted against all of the euro area’s weaknesses. Somehow, America’s economic imbalances are ignored. A Martian investor might at least wonder why an economy with the biggest current-account deficit the world has ever seen, a negative personal savings rate, record borrowing by firms and households, not to mention a dangerously overvalued stockmarket, had such a strong currency. Financial markets believe that these imbalances can be unwound gradually, allowing the economy to land softly. But even hard landings look soft when they start. Why the time has come to suspend the

euro The key factor is the outflow of capital from the euro zone to America and Britain. In today's globalised foreign exchange markets, it is capital movements rather than trade deficits or growth rates that count. The euro zone is bleeding capital at the rate of $50-60 billion per month. This is partly due to the takeover of US companies by German ones, and the reason for that is that profit opportunities are better outside the euro zone The Maastricht Treaty has left the responsibility for the exchange rate of the euro with the Council of Ministers, not the ECB. Article 109 (2) says that the council may "formulate general orientations" for exchange rate policy. A resolution at the Luxembourg Summit in 1997 strengthened this by resolving that "the council may, in exceptional circumstances, for example in the case of a misalignment, formulate general orientations for exchange rate policy in relation to non-EU countries".

This is such a time. It should be the first duty of the French presidency of the EU to show some leadership on this question. Trading in the euro should be suspended, and the ERM reintroduced with broad bands. The euro should be relaunched when it has proved to be stable for at least six months.

This would be a drastic step and cause some loss of face to the ECB. But the euro is a new currency. There is still time before it comes into circulation as a currency. It is thought everywhere to be a failing one. This may be unfair, but then that is the perception of the market. As Mr Volcker said to the Lords committee: "I stress the perceptions, as they are

From boom

to trust Strong domestic demand /in the US/ has sucked in floods of imports that have suppressed inflation but have expanded the current account deficit from $82bn in 1983 to probably more than $400bn this year. Forecasts range up to $500bn for 2001. This alarming deterioration might have been expected to trigger a dollar crisis that would have ended the boom, but instead foreign capital has poured in, much of it coming from continental Europe to the great embarrassment of the sponsors of the euro. The correct way to support the euro In fact, the eurosystem could have intervened massively if it had wanted to because it is sitting on more than E260bn ($221bn) in foreign exchange reserves, plus E100bn worth of gold - much more than the US. One of the reasons why the eurosystem did not intervene with substantial amounts has to do with its structure. Most of the foreign exchange reserves potentially backing up the euro are owned by the 11 national central banks. The ECB itself has only about E50bn of reserves directly at its disposal. The remainder, worth more than E210bn, plus most of the gold, belongs to the national central banks. These reserves were accumulated during the pre-euro period when there were still 11 national currencies that needed some foreign exchange reserve backing. With the launch of the euro, however, there is no longer any reason for national central banks of the euro-zone to continue to keep more than E210bn of reserves. As these reserves consist mostly of dollars, which are currently over- valued in a long-term perspective, there is a strong argument for disposing of them to realise the profit. But this is not a job for the ECB. The simplest way to dispose of the excess reserves at the national central banks would thus be to ask them to keep E50bn and transfer the remainder of about E160bn to national treasuries. Keeping reserves of E50bn in the national central banks of the eurosystem is more than enough for a potential call-up by the ECB because this would allow the ECB to count on about E100bn in an emergency, about twice the sum available to US authorities. National treasuries in the euro-zone countries would then find themselves with E160bn worth of dollars. If they believe what their political representatives repeatedly assert, that the euro is massively undervalued, they should sell these dollars quickly and use the proceeds to pay off public debt. Carried out over a period of two years, this would amount to selling about $8bn a month - more than the ECB's intervention in September and enough to finance the outflow of foreign direct investment from the euro-zone. Should the euro return to what is commonly thought to be its long-term equilibrium level of about $1.10 - about 30 per cent above the current rate - the net gain would be E45bn, or almost 1 per cent of the euro-zone's gross domestic product.

Konsumentprisnivåer i Sverige jämfört med övriga medlemsstater i EU Samuel Brittan: Watch the

dollar, not the euro, Financial Times, October 12 Dark clouds on the euro horizon , BBC United States riding to the rescue of a currency hailed by